Corporate Financing Focus

Active Currency Management Can Turn Risk Exposure Into Source of Potential Returns

Multinational industrial companies trading goods in global markets or building new plants overseas routinely take on exposure to foreign currency fluctuations as part of doing business, and they often consider hedging all or part of their exposure.

When a corporation hedges its overseas revenue, it is effectively buying insurance against unfavorable currency moves, which is a defensive posture, says Scott Arnott, vice president, global fixed income and currencies, at Goldman Sachs Asset Management in London.

More often than not, the currency exposure is seen as a necessary evil, and the price, or rate of exchange, is simply accepted as is, Arnott says.

Instead of ignoring currency risk or deciding how much of it to hedge, companies operating in global markets should realize that techniques for actively managing currency positions could be a good source of potential returns, according to Arnott.

Currency markets are both highly liquid, with average global daily turnover of $1.9 trillion, and inefficient, he says. There are few other markets where such a large number of participants are so accepting of price and unconcerned with profit.

When central banks intervene to influence exchange rates, for example, they are not looking to make a profit, but rather to attain an economic or political objective.

Tourists who are spending money abroad and investors buying foreign stocks and bonds are all involved in the currency markets, but with different objectives in mind. This creates inefficiencies in the market that active currency managers can exploit, Arnott says.

Trends in the currency markets are not only recognizable, but once they become established, they are usually long lasting, he says.

This makes it possible for a chief financial officer to select an active currency manager who can create positive returns or limit losses from currency exposures.

When employing a currency manager, the company should not limit its potential opportunities for gains by restricting the managers ability to trade, such as in a limited number of currencies, Arnott says. The company should ask the manager for his best ideas.

Following a period of low interest rates and lackluster equity-market returns, investors are looking for alternatives, such as currency markets, the Goldman Sachs executive says.

|

|

|

Glenn Stevens, managing director of GAIN Capital, a provider of foreign exchange services, including online trading and asset management, says the trend toward active currency management began with hedge funds and has been adopted by a growing number of portfolio managers, who realize they can add 300-400 basis points to annual returns by actively managing their currency exposures.

Major corporations are now joining this move toward active management of currency positions, and a cottage industry has sprung up to serve their needs, he says.

GAIN Capital, based in Warren, New Jersey, is a leading non-bank foreign exchange dealer and market maker, with an average transaction volume of more than $60 billion a month. While many of GAIN Capitals clients use its online currency trading facilities to speculate

in the foreign exchange market, a growing proportion of users are hedgers who have existing exposure, such as fixed-income portfolios in another country, Stevens says.

As investors diversify their portfolios internationally, the need for active currency management will continue to grow, he says.

When a corporate CFO or treasurer has a strong view on the likely direction of a currency, it makes sense to take action on this conviction, Stevens says.

|

|

|

Greenspan Hopeful

Federal Reserve chairman Alan Greenspan, in London for the Group of 7 meeting last month, said market forces and budgetary discipline in the US should allow global economic imbalances to be reduced over time.

Market forces appear poised to stabilize and, over the longer run, possibly to decrease the US current account deficit and its attendant financing requirements, he said.

According to Greenspan, European companies may decide to protect their profit margins, rather than seeking to cut prices to preserve market share if the dollar weakens further. He also suggested that US exports may begin to rise as a result of the dollars depreciation since 2002.

In contrast to Greenspans upbeat remarks, former US treasury secretary Robert Rubin, who is now a senior Citigroup executive, says he fears the US fiscal and current account deficits may have a tendency to get worse rather than better.

The US imbalances could have serious bond market effects and also raise very complex questions about our currency, Rubin told a conference on enterprise and productivity hosted by UK chancellor of the exchequer Gordon Brown on the sidelines of the February Group of 7 meeting.

The conventional view is that there is probably a fairly good chance that the dollar could decline over some period of time, Rubin said.

|

|

|

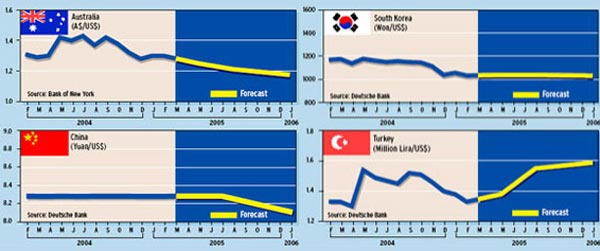

China Pressured

Meanwhile, G-7 officials are keeping the pressure on China to allow its currency to strengthen to help narrow the US current account deficit.

Despite mounting pressure from Europe and the US to revalue the yuan, China isnt likely to succumb to these demands and compromise its economic engine for the sake of prematurely liberalizing its financial markets, says Ashraf Laidi, chief currency analyst at MG Financial Group, an online currency trading firm based in New York.

The Bank of Japan could begin to lighten its holdings of US treasury securities in anticipation of an eventual move by China to revalue its currency, most likely in the first half of 2006, Laidi says.

Japan leads the world in holdings of US treasury debt, with about $715 billion.

A gradual Japanese retreat from US-dollar securities into non-dollar assets is inevitable in order to avoid massive losses on the central banks dollar portfolios, Laidi says.

Several central banks already have started shifting their reserves into euros and away from dollars, and Japan has no choice but to follow suit, Laidi says.

The ongoing lack of intervention by the Bank of Japan in the foreign exchange market, combined with improving prospects of a Chinese yuan revaluation, have created a bullish opportunity for the yen, he says.

According to Laidi, market participants expect Japans inflation to regain positive territory in 2005, following seven years of deflation.

|

|

|

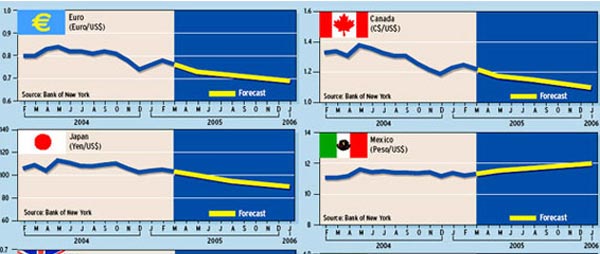

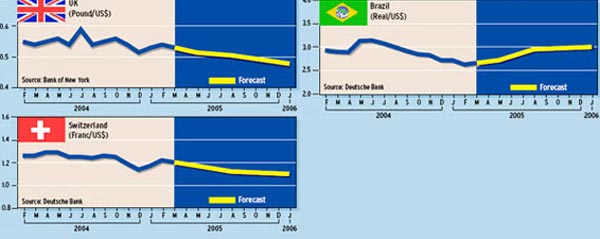

Currency Forecasts

Gordon Platt