With interest rates bottoming and the market jittery, treasurers are seeking more unconventional and versatile means for managing stockpiled war chests of liquidity.

Treasurers face myriad challenges when it comes to managing their organizations’ liquidity. Even though markets are now awash with cheap liquidity as the economic crisis of 2007–2008 recedes, economic uncertainty still lingers across many corners of the globe. And as companies conduct more business cross-border, they are increasingly vulnerable to market instability.

One example is the slowing of economic growth in China. Although the country’s GDP grew by a more than respectable 7.3% in 2014, that was down from 10.6% in 2010, according to World Bank figures.

Or consider the Middle East. Although the flood of refugees into Europe from Syria is foremost a humanitarian crisis, it is also likely to have an economic impact, says Craig Martin, executive director of the Corporate Treasurers Council with the Association for Financial Professionals (AFP). “A lot of resources will have to come to bear on this problem,” he says, adding, “it will have an impact we’re not forecasting.”

Low interest rates—as of early October the European Central Bank’s deposit rate was -0.20%— makes earning a decent return on excess cash next to impossible. Increasing regulations add complexity to an already complicated function. For instance, regulations in Europe make it difficult to manage liquidity across the continent, as many banks are withdrawing the scope of both their product and geographic reach, says Magnus Lind, chair and founder of Treasury Peer, a global organization for corporate treasurers. One of the most notable examples was the decision by RBS early in 2015 to cut its geographic footprint outside the British Isles.

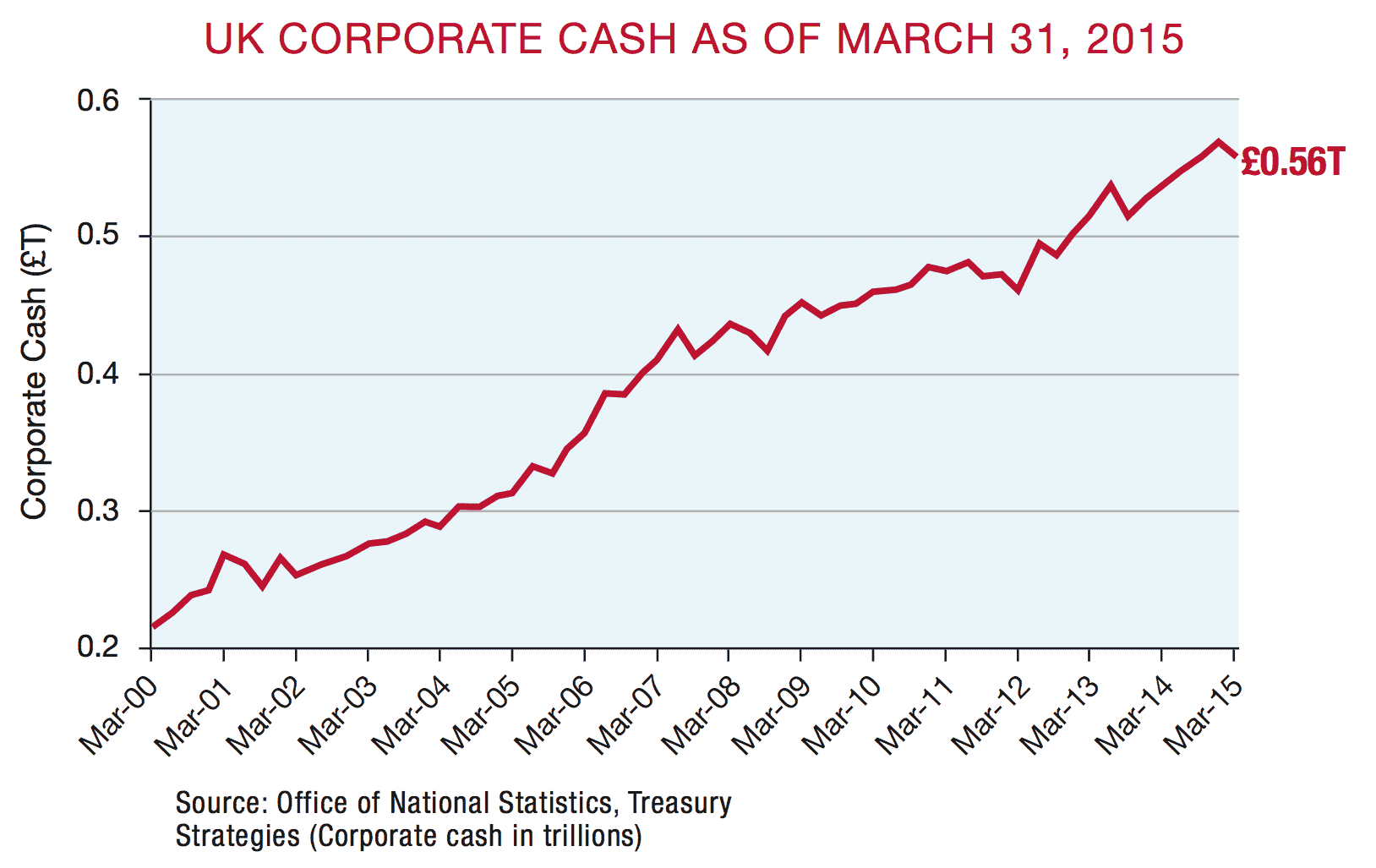

PRESERVING CASH BALANCES

Treasurers are taking action to address these challenges. First, they continue to stockpile cash. Between 2000 and 2015, corporate cash levels in the UK have risen by approximately 170%, according to Treasury Strategies. “As these hits have been coming in the last seven or eight years, we’ve seen corporate cash levels remain high,” says Kevin Ruiz, principal with the consultancy Treasury Strategies.

Treasurers continue to focus on safety and liquidity. “We’re not investing in anything except highly liquid money market investments,” says Mark Eisele, vice president, CFO and treasurer with Applied Industrial Technologies, a US-based distributor of industrial products. The emphasis on liquidity along with safety is key, given Applied Industrial’s acquisition activity. The company made at least four acquisitions in fiscal 2015, and considers acquisitions an integral part of its growth strategy, according to its 2015 annual report. As the company builds cash, it can use it for acquisitions, Eisele says.

Moreover, although interest rates remain low, attempting to capture a few extra basis points by taking on riskier investments generally isn’t worth it, Eisele says. “The level of risk you add dwarfs what you can get in return.”

Eisele isn’t alone in his thinking. “The trend remains for certainty over yield,” says Stephen Baseby, associate policy and technical director with the London-based Association of Corporate Treasurers. Indeed, principal safety remains the top objective when treasurers invest corporate cash, according to the 2015 AFP Liquidity Survey.

GETTING A HANDLE ON RISK

Technology and automation are playing a key role in helping treasurers better manage their liquidity. Though efficiency remains a priority of treasurers’ efforts to automate accounts payable and receivable and other financial operations, the focus has expanded to include control and visibility, Ruiz says. “Treasurers want to understand where their positions are each day.” Automated systems can provide this to a greater degree than manual processes.

Even better, says Martin, is the rise of Cloud-based systems that have put many of these tools within the reach of smaller companies for the first time. “These solutions,” he adds, “have become more robust.”

One example is a technology that allows companies to offer or use dynamic discounting—a sliding scale of discounts that suppliers can offer buyers for accounts receivable. Ad van der Poel, senior vice president of financing services with Basware, says dynamic discounting isn’t new, but the execution is new, based on new technology. According to the company’s research, between 60% and 80% of suppliers are willing to offer discounts if they can receive payment early. The return to customers is significantly higher than what most can get through bank deposits, van der Poel notes. For companies that are cash-rich, “this helps them get value from their liquidity.” At the same time, suppliers can accelerate their cash flows.

Although many organizations try to work with a small group of banking partners, regulation can make that difficult. For instance, regulations in place in Europe make it hard to find continentwide solutions from one bank, so many companies work with multiple banks, Lind says. However, that creates challenges when it comes to managing cash payments and receipts. “The more systems, the more banks, the more people and the more cash management centers, the bigger the risk. You can automate, but it’s a hassle to do that. It becomes more complicated.”

On a global basis, the impact of Basel III remains to be seen, as each country’s regulator will need to interpret the liquidity-coverage-ratio regulation within the context of the country’s regulatory scheme, says Martin of the AFP. The general consensus seems to be that cross-border pooling of excess cash balances will continue to be permitted, albeit at a higher cost.

Basel III also is expected to boost the cost of borrowing, says Tom Hunt, AFP’s director of treasury services. Treasurers are being encouraged to extend credit facilities now, even if they don’t mature for several more years.

Treasurers are taking several steps to better understand and forecast cash inflow and outflows, which has become both more important and more challenging, given many organizations’ increasingly global footprint. A growing number of treasurers are also working more closely with their colleagues in other business units. “The smart ones are doing this,” says Joseph Bizzarro, CEO of Vizant, a treasury advisory firm. “You can’t understand the flow of funds when you don’t understand the business.”

Indeed, treasury needs to take a lead role as many organizations venture further from their home base, Martin says. “We’re financial market analysts and risk managers. So it falls to treasury to understand the global risks.”