Capital market reform bodes well for depositary receipt issuers and foreign investors.

Plunging oil prices, an economic slowdown in China and volatile emerging markets made 2015 a challenging year for issuers and investors in global financial markets. Although 2016 hasn’t started out any better, it could be a breakthrough year for depositary receipts, as more and more local regulators around the world come to recognize the economic benefits of DRs and seek to open their markets wider to foreign investors.

“There will be challenges again this year, but challenges open up opportunities,” says Nancy Lissemore, managing director and global head of depositary receipt services at Citi. “In such an environment, capital market reforms could go forward,” she says.

Regulatory changes in India, Taiwan and China, which Citi has been following closely in the past few years, are continuing to progress, Lissemore says, although “further development is required if issuers and investors are to reap the full benefits.”

India needs to finalize regulations in this area, but when it does, “this will be very positive for DR access,” Lissemore says.

China took a major step in February toward giving foreign investors free access to its bond market, the third-largest in the world. China wants to attract foreign capital at a time when capital flight is depressing the renminbi and has forced the country’s central bank to spend hundreds of billions of dollars of reserves to support the currency.

“International investors are continuing to demand access to equities and debt instruments,” Lissemore says. She points to the success of unsponsored American depositary receipts (ADRs) and global depositary note (GDN) programs. GDNs, debt security versions of the traditional DR structure, have existed for about five years and have grown quickly in the past few years. Citi offers the product in 17 markets, mostly for sovereign debt. The GDNs replicate the characteristics of local bonds while trading in dollar terms.

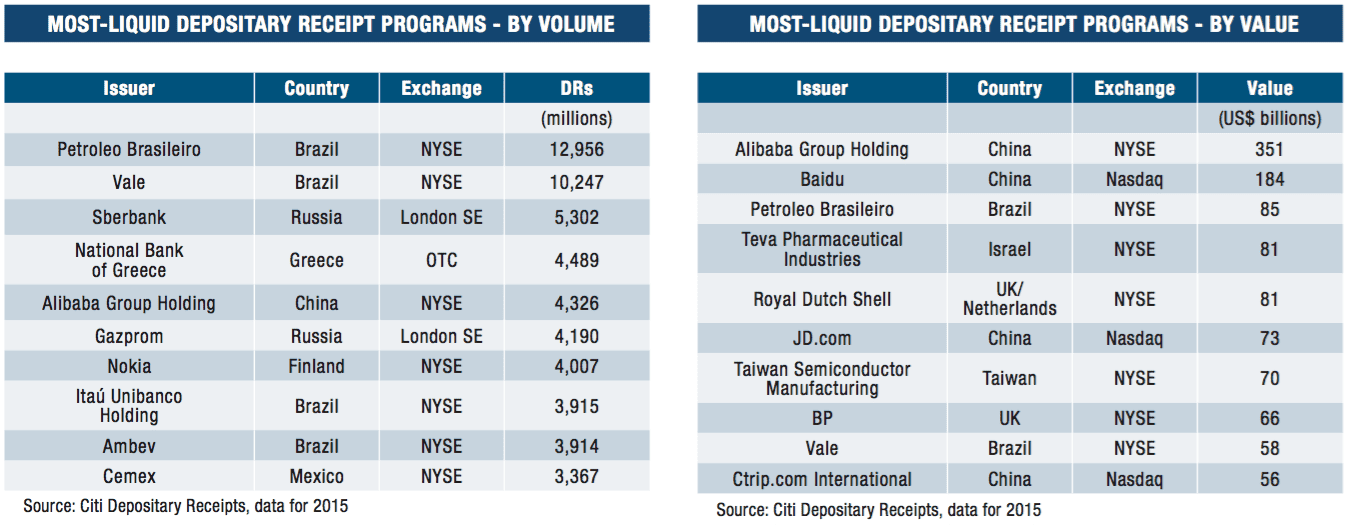

Most foreign stocks trade in the US markets as ADRs. Unsponsored ADRs, which trade in the US over-the-counter market, are established by depository banks without the direct involvement of the issuer of the underlying ordinary shares. These programs have grown tremendously since October 2008, when the US Securities and Exchange Commission exempted them from US registration, provided the issuer of the shares publishes regular financial statements in English.

The pool of unsponsored ADR programs has expanded to more than 1,620, and Citi alone offers 860 such programs, Lissemore says. Citi plans to open 100 to 150 new, unsponsored ADR programs this year, in response to growing investor demand, she says. Trading in unsponsored ADRs increased by 81% last year, compared with a year earlier.

Lissemore says she expects volatility in global markets this year, which should further boost DR trading activity. Despite the 71% drop in DR capital raising in 2015, DR trading volume rose by 6.2 billion, to 163.7 billion shares.

Citi expects a relatively active DR market in 2016. Emerging companies in the pharmaceutical sector, and other foreign issuers are continuing to take advantage of the reduced reporting requirements of going public under the JOBS Act of 2012 to access US capital markets, Lissemore says. “We are working with a lot of companies that are making plans to raise capital, and are watching the market,” she says.

Christopher Kearns, CEO of depositary receipts at BNY Mellon, says: “A growing number of investors, including DR investors, are targeting money from an environmental, social and governance (ESG) perspective. During 2015, BNY Mellon became the first depository to provide detailed data and insights to help clients understand ESG factors that are reshaping global investment strategies.”

As the leading depository, with a 58% market share of all sponsored programs, BNY Mellon is committed to helping its DR clients understand and respond to social, environmental and regulatory change, Kearns says. “More companies are reporting on ESG, and they need to know what is material to long-term investors in this area,” he says.

BNY Mellon Depositary Receipts is collaborating with the Newton Centre for Endowment Asset Management at the University of Cambridge to study the evolving view in the financial markets of the materiality of nonfinancial information to issuers, investors and asset managers.

PILING ON

BNY Mellon has also teamed up with Sustainalytics, an independent ESG research and analysis firm based in Amsterdam. BNY Mellon’s DR business will offer its clients access to the Dutch firm’s research and ratings, as well as customized benchmark reports on how issuers are viewed by investors.

The offering will allow the bank “to help clients better understand the needs of investors and develop strategies around enhanced corporate disclosure,” Kearns says. “We want to keep firms at the forefront of these trends.”

A study on institutional investment in DRs that BNY Mellon commissioned from New York analytics firm Ipreo shows that the number of institutions investing in DRs grew from 3,261 in the second quarter of 2010 to 4,533 in the second quarter of 2015. Global DR equity assets under management increased from $573.9 billion in the second quarter of 2010 to more than $764.2 billion in the second quarter of last year, representing a 5.9% annual growth rate.

BNY Mellon is a major participant in the unsponsored DR market, where it has a facility established for 95% of the entire unsponsored universe. “Unsponsored DRs are good for investors who seek the broadest opportunity to invest,” Kearns says. “Sponsored programs don’t cover the whole universe.”

In 2015 there were 58 new sponsored programs established, compared with 77 in 2014. Of the 59 over-the-counter, unsponsored programs established last year, BNY Mellon was the sole depository for 54% of these programs. There are now a total of 3,602 DR programs in existence.

In the face of demanding global market conditions, activity in the DR market remained solid during 2015, and DR trading—in terms of both volume and value—is likely to rise incrementally as cross-border capital flows keep increasing, Deutsche Bank says in its DR annual report, released in February. “The use of ADRs as an acquisition tool is still a topic of discussion with many companies, potentially resulting in more deals of this nature,” the bank says.

At a time when emerging capital markets flows remain under pressure, the need to attract foreign capital has increased. Political momentum is building behind market-opening initiatives and the further development of domestic capital markets. DR bankers say this bodes well for the future of their business.