Thailand's economy is being battered by the pandemic and political uncertainty.

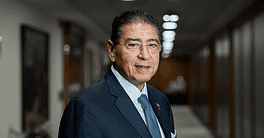

In January, Thailand’s finance ministry estimated that the economy would grow 2.8% this year; in June, the projection was revised downward to a -8.5% contraction, the greatest drop among major South Asian nations. To help maneuver the country through the pandemic-driven recession, 61-year-old veteran banking executive Predee Daochai was picked in a cabinet reshuffle as the new finance minister in early August. However, he resigned on September 1 after just 26 days on the job. A former co-president of giant Kasikornbank and chairman of the Thai Bankers’ Association, Predee cited health reasons as the cause for stepping down. Disputes within the cabinet—reported by a variety of sources—were most likely the driving force behind Predee’s resignation.

“Taking the helm of the finance ministry amidst the pandemic was not going to be a walk in the park for anybody,” says Pavida Pananond, professor of international business at Bangkok’s Thammasat University. “Despite his extensive experience in the banking sector, Preede was challenged with steering Thailand out of its worst economic contraction since 1997, a task made even more daunting by the fact that he was a first-time politician.”

In late March, the kingdom closed its borders and implemented business lockdowns in a largely successful attempt to contain the epidemic. Although many restrictions have since been lifted, Thailand has yet to reopen for international tourism. Meanwhile, as a result of the global economic downturn, exports have plunged more than 20%.

The next finance minister will have to pick up where his predecessor abruptly left off. While his immediate order of business will be to revive and reinvigorate the Thai economy, Pavida says, the new appointee will also need to focus on the broader picture. “In order to enable the country to stay competitive in the post-Covid era, longer term challenges will include improving Thailand’s economic fundamentals,” she says, “from labor skills and productivity to outdated bureaucratic red tape.”

The strategy, in all probability, will mirror the one already detailed by the outgoing minister, a mix of policies aimed at boosting employment and public spending, supporting small and midsize enterprises and improving tax collection. But matters might be made more complicated by the recent antigovernment protests calling for the dissolution of Parliament and reforms of the monarchy. The huge rallies, Pavida says, reflect widespread dissatisfaction with the country’s fundamental institutions. “The rising political temperature can only contribute to making any attempt to restore foreign and domestic investor confidence much harder,” she warns.