Basel III and other regulatory developments are causing a sea change in bank-corporate relationships. It is up to corporate treasurers to lead that process.

Table Of Contents

Bank-corporate relationships are beginning to experience big changes as a result of new regulations, such as Basel III. This is likely to accelerate in the coming months, and it behooves companies to build a clearer picture of how they divide business between banking partners in order to steer that process of change, rather than simply being swept up by it.

“The changes are beginning to be pretty dramatic in the way in which banks and corporates work together,” notes Guenther Peer, Austrian-based vice president, treasury services business operations, with Reval. For instance, some banks may stop offering notional pooling to certain smaller companies, Peer says. “It will become too expensive for them to do so as a result of regulations imposed by Basel III,” he adds. Basel III is a set of reform measures, developed by the Basel Committee on Banking Supervision, aimed at boosting the banking sector’s ability to absorb shocks arising from financial and economic stress.

To be sure, the changes are just beginning. “It [Basel III’s impact] has been mentioned in some meetings with our bankers, but I can’t say that it has been the cause for any changes as of yet,” says Craig Creaturo, chief financial officer and vice president, administration, with Chromalox, a US-based developer of advanced thermal technologies for industrial heating applications.

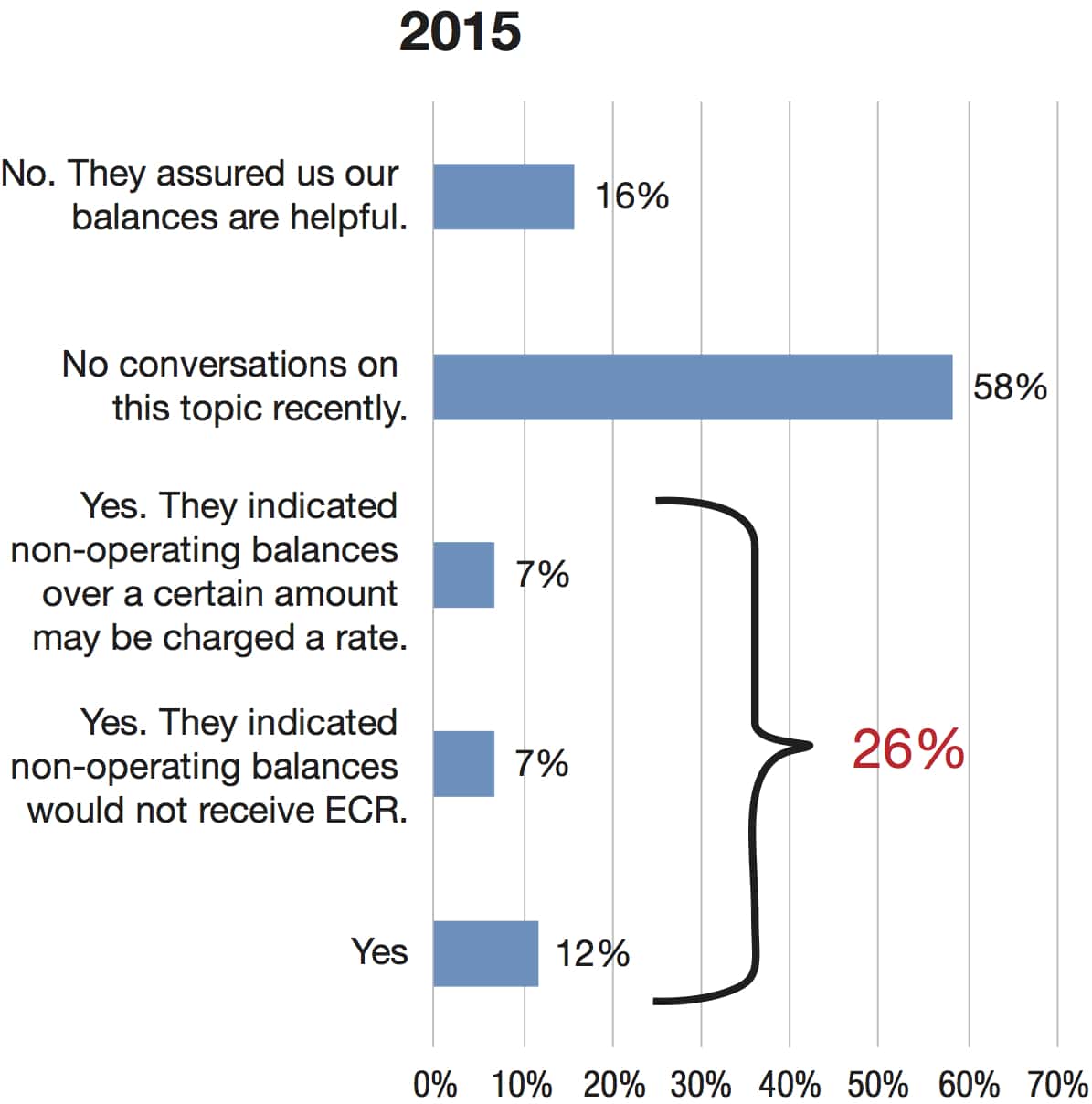

Still, slightly more than one-fourth of treasurers and other financial professionals responding to the 2015 Liquidity Risk Survey indicated their banks had talked with them about reducing balances (see chart, p 38). Among these, 7% learned their banks may levy charges on non-operating balances; another 7% were told non-operating balances would not qualify for an earnings credit rate (ECR)—interest paid on excess account balances that reduce bank service charges. Consultancy Strategic Treasurer and investment adviser Capital Advisors Group published the survey.

One of the biggest impacts for corporates likely will come from the liquidity coverage ratio (LCR), which is leading to changes in pricing, as well as in the products and services banks offer, Peer notes. The LCR measures banks’ level of “unencumbered high-quality liquid assets that can be converted easily and immediately in private markets into cash to meet their liquidity needs for a 30-calendar-day liquidity stress scenario.” Between January 2015 and January 2019, the minimum LCR required of banks under Basel III will rise from 60% to 100%, although some countries have accelerated this time line.

As a result of Basel III, “the whole world has split into two groups: operating and non-operating deposits,” says Paul LaRock, principal with Treasury Strategies. Operating deposits now are seen as a source of liquidity from many banks’ perspective, as they’re more difficult to move—few companies would want to quickly transfer the bank accounts through which their payroll or accounts receivable flow, given the administrative hassles. “They’re ‘stickier,’” LaRock adds.

Conversely, Basel III assumes non-operating deposits can be moved quickly. That makes them riskier, as banks would have to cover the outflows. “There was a time when non-operating accounts were the prettiest girl at the dance,” says Kevin Ruiz, principal, also with Treasury Strategies. “Now, it’s different.”

Basel III may also alter banks’ views of selected services they offer—and how they offer them. More banks will try to serve multinational companies through correspondent networks and banking clubs, says John Grout, policy and technical director with the Association of Corporate Treasurers, London. “Multinational companies dealing with banks in many countries will have to pay more attention to local banks.”

As banks reassess their operations in light of Basel III, corporate finance professionals will want to determine, as best they can, their value to their banking partners. “You want to be as important to your banks as they’re important to you,” says Craig Jeffery, managing partner with Strategic Treasurer. While it’s typically not necessary to be among the top 10% of their clients, it’s also not helpful to lag in the bottom quartile, he adds. “Your bankers need to make some money off you.”

Many banks use Raroc, or Risk-Adjusted Return on Capital, to measure the profitability of their major corporate clients, taking into account the entire portfolio of investment banking, cash management and other services they’re using, Jeffery says. Corporates should try to estimate the Raroc they’re providing their banking partners, at least for their top banks, he adds. “It should be done with some level of formality.”

Companies should know the “share of wallet” they’re providing each bank, Peer says. That is, of all the banking services the company uses, what percentage is obtained from each banking partner? This understanding will give them a clearer picture of their exposure to each of their banking partners, will allow them to make strategic decisions about how much business they want to give to each partner and give them a sound quantitative foundation from which to negotiate with their banks on fees.

The demand by key banking partners for a bigger piece of the pie may prompt some companies to consolidate banking partners, Peer notes. In 2013, Chassis Brakes International issued a banking RFP for its European operations. Among the goals: reducing the number of banking partners, then at 12, as well as banking fees. The result? “We have only three banks across Europe, with better bank conditions,” says Hélène Brunou, corporate treasury director with the Drancy, Francebased manufacturer of automotive foundation brakes and foundation brake components.

And for both banks and their corporate clients the full impact of new regulations are yet to be seen. “This will provide entertainment for treasurers for some years,” Grout says.