Shariaprinciples are no barrier to stable long-term growth.

Sharia principles have stood the test of time, and while Standard & Poor’s considers Islamic institutions somewhat more vulnerable than conventional banks due to comparatively higher real estate exposure—a side effect of the asset-backed principle inherent to Islamic finance—they went into the Covid-19 months solidly capitalized. S&P projects that growth in the GCC will contract 5.6% in 2020 before expanding 2.4% in 2021, and that the region’s banking sector will see a decline in loan growth to 6.6% this year.

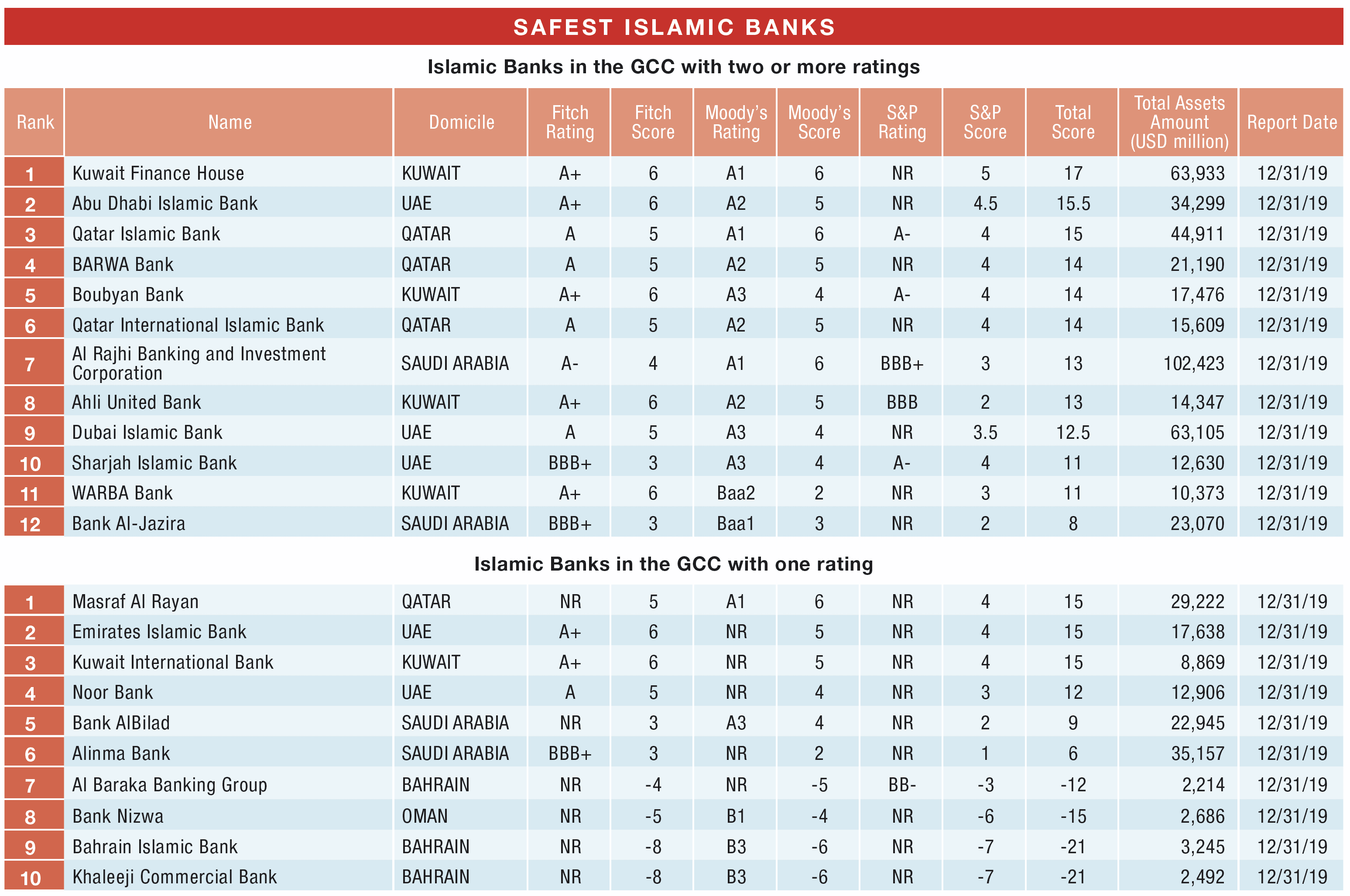

Hence, this year’s ranking shows little change, the most notable being Barwa Bank’s rise to No. 4 following its merger with International Bank of Qatar, which made it the country’s third-largest Islamic banking franchise. Dubai Islamic Bank’s merger with Noor Bank last year likewise created one of the largest Islamic banks in the world. As GCC banks look to enhance their offerings, mergers are likely to accelerate.

Already surpassing $2 trillion, Islamic banks will reach $3.8 trillion by 2023, and the sector is standardizing rules and procedures, according to a 2018 report by Thomson Reuters. The Central Bank of Kuwait in October approved the establishment of a committee of sharia supervision to establish international best practices. Also in October, the International Islamic Financial Market published its Sukuk Al Ijarah Standard Document Templates, which streamline many elements for sukuk issuers and increase transparency for investors.

Global Finance’s 2020 Safest Islamic Banks encompass 12 institutions based in Saudi Arabia, the United Arab Emirates, Kuwait and Qatar that are among the world’s largest 500 banks, are not state owned and carry a minimum of two agency ratings. A further 10 institutions carry only one agency rating, but in our judgment are poised to take advantage of the expansion in Islamic banking.