Corporate bond issuance reached $2.1 trillion in 2019, pushing the outstanding stock to a record $13.5 trillion.

The return to expansionary monetary policies in early 2019 prompted a $2.1 trillion rebound in the global issuance of corporate bonds according to the Organization for Economic Co-operation and Development (OECD). The outstanding corporate debt market more than doubled to a record $13.5 trillion from the previous year. However, bond quality suffered.

Experts have warned against the sugar rush in corporate debt issuance as investors sought higher returns from risky assets in a low interest rate environment.

Last year, the overall share of non-investment grade corporate bonds increased to 25% of total issuance from 20% in every year since 2010, the OECD said in the 54-page report, “Corporate Bond Market Trends, Emerging Risks and Monetary Policy.”

“This is the longest period since 1980 that the portion of non-investment grade issuance has remained so high, indicating that default rates in a future downturn are likely to be higher than in previous credit cycles,” the organization noted.

The portion of bonds rated BBB, the lowest investment-grade level, accounted last year for the majority (51%) of global investment grade corporate debt, according to the OECD. This was up from 39% in 2000–2007. Last year, only 30% of bonds had a rating of A or higher and all were advanced economies.

“Large issuance of BBB rated bonds, non-investment grade bonds and bonds from emerging market corporations since 2008 has resulted in a situation where lower credit quality bonds have come to dominate the global outstanding stock,” the OECD said.

China’s Pivotal Role

The study analyzed more than 92,000 unique corporate bond issues by non-financial companies from 114 countries between 2000 and 2019.

Companies in advanced economies accounted for 78% ($10.5 trillion) of outstanding corporate debt compared to 22% ($3.0 trillion) in emerging markets.

China played “a pivotal role” in market growth over the last decade.

Bonds issued from Chinese companies have increased from a negligible level before the 2008 crisis to an average $285 billion between 2008 to 2019. In 2016, Chinese companies became the second largest issuers of corporate bonds, peaking at $691 billion. Issuance by companies in other emerging markets has remained relatively low at between $110 billion and $190 billion over the 10-year period.

Concerns over the quality of Chinese issuance might explain why foreign participation accounts for only 1.6% of total outstanding corporate debt. Confidence may improve after rating agency S&P Global last year was authorized to operate in China, the OECD said. Fitch Ratings and Moody’s have also applied for licenses.

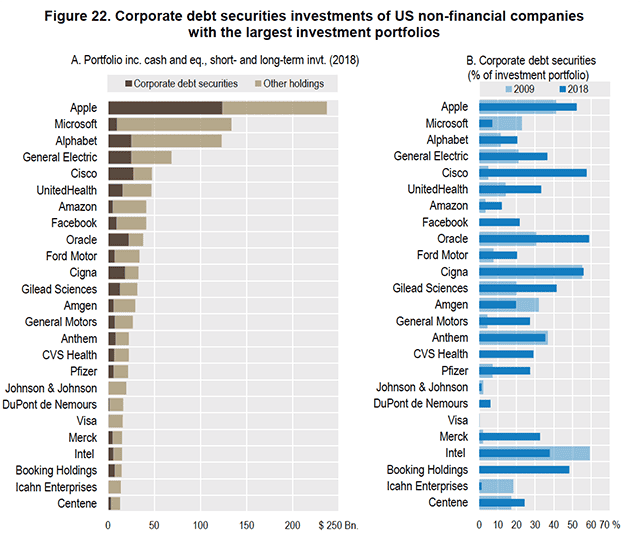

Apple Takes the Lead

While financial institutions have traditionally been the largest owners of corporate debt (86% in the US and Japan; 93% in the euro area; 98% in the UK), non-financial US corporations have increased their holdings since the 2008 financial crisis.

The total value of corporate bonds owned by 25 large US corporations ranked by the OECD tripled to $356 billion in 2018 from $119 billion in 2009. Their overall investment portfolio is worth $1.12 trillion.

iPhone maker Apple has the largest investment portfolio in the ranking, $237.1 billion, 52% of which is in corporate bonds (the top borrower on the list).

Apple’s corporate debt ($124 billion) equals the combined holdings of the world’s six largest corporate bonds exchange-traded funds, according to the OECD.

The top 10 companies by size of their investment portfolio are Apple, Microsoft, Alphabet, General Electric, Cisco, United Health, Amazon, Facebook, Oracle and Ford.

While 15 corporations including Microsoft, Amgen, Intel and Icahn borrowed more in 2019, other companies reduced their holdings. Among them, Apple decreased the share of corporate bonds in their portfolio from 52% to 41%, General Motors from 27% to 4%, Pfizer from 27% to 7%, Gilead from 41% to 20%, and Booking Holdings from 48% to 0%.

Other concerning trends identified by the OECD include longer maturities (13 years in 2019 from 9.4 in early 2000s), a decline in the quality of covenants for non-investment grade bonds, lower minimum credit rating requirements for some companies, and record repayments of $1.3 trillion within one year.