CORPORATE FINANCING NEWS / FOREIGN EXCHANGE

by Gordon Platt

The euro tumbled against the dollar, the yen and the Swiss franc in mid-June, as European finance ministers reached an impasse on a second Greek aid package and demonstrators clashed with police in Athens. Greeces prime minister George Papandreou tried to push a five-year austerity plan through parliament that would raise taxes, cut spending and put state assets up for sale to avoid default.

The risk of a disorderly Greek default escalated after euro area finance ministers failed to decide how to handle the crisis at an emergency meeting on June 14. A deadlock developed on how to encourage or force the private sector to bear some of the cost of a debt extension, re-profiling or restructuring.

Meanwhile, Moodys Investors Service placed the stand-alone financial strength ratings of three major French banks on review for a possible downgrade, citing their holdings of Greek public and private debt and the potential impact of a possible default.

The Day after Default

Recent market action suggests that investors have largely prepared for the eventual certainty of a Greek credit event, but the markets remain vulnerable to a broader contagion from a eurozone government default across sovereigns, financial-sector and risk assets, says Lena Komileva, London-based global head of G10 strategy at Brown Brothers Harriman. Ultimately, the risk is no longer Greek default but [what happens] the day after Greece defaults.

The markets are reacting to the political risk of the EUs management of the crisis, rather than the probability of a Greek credit event per se, according to Komileva. The difference is between a managed and unmanaged default scenario for Greece, she says. This is what will ultimately mark the difference between a governments solvency crisis and a euro crisis.

Analyses of the direct effects of a Greek default may far underestimate the indirect effects, such as the potential for a chain of disorderly market and bank-asset downgrades similar to what happened after the downfall of Lehman Brothers in 2008, she says. If the culmination of Greek default risk comes at the expense of disorderly developments in sovereign and bank credit markets, then European financial integration and the euro in its current form will be at risk, she says.

Biggest Exposure

Data from the Bank for International Settlements show that French and then German banks have by far the biggest exposure to Greek debt, which should not be a surprise to the market, says Sara Yates, foreign exchange strategist at Barclays Capital, based in London. What is more important for the euro is how and when Greece restructures, she says. Our economics team does not expect Greece to restructure in 2011.

Restructuring Greek debt before the country makes progress in moving toward fiscal balance and putting the country on a more sustainable footing would be putting the cart before the horse, according to Yates. Whats more, an early restructuring would increase the likelihood of contagion to the rest of the periphery, she says.

An early and disorderly restructuring of Greeces debt may occur if Greece fails to enact its five-year austerity plan, but this is only a risk and is not the most likely scenario, Yates says. Our central scenario remains for the euro area and the euro to muddle through, particularly as Spain has taken some important steps forward, helping it to remain decoupled from the periphery, she says. We expect the euro to continue to shrug off concerns [related to the debt crisis] and to grind higher versus the dollar, supported by the European Central Banks tightening bias, much as it has done over the past 12 months.

Least Ugly Contest

The euro versus the dollar looks to remain a least ugly contest for the time being, until uncertainty over the US and European debt problems begins to subside, says Michael Woolfolk, a managing director and senior currency strategist in the global markets business of BNY Mellon. Although the outlook for US fiscal and monetary policy is unclear, the outlook for US growth and inflation is for both to move higher, he says. US core consumer inflation rose more than expected in May to post its largest increase in nearly three years, due to increases in apparel and vehicle costs. At an annual rate, the increase was 1.5%, up from 1.3% in April, but still quite low.

The US economic recovery appears to have hit a soft patch, but recent data indicate that the slowdown is less severe than is widely believed, Woolfolk says. The soft patch may not be the double-dip scenario many had feared, he says.

While clearly handicapped by high levels of unemployment and debt service, consumer demand remained brisk throughout the severe winter weather and has been stable this spring, apart from auto sales, Woolfolk says. A rebound in consumer spending this summer should keep growth in GDP near 3% for the second half of the year.

Fed Program Ends

It remains to be seen how the end of QE II, the Federal Reserves second round of quantitative easing, will affect the dollar and the financial markets. The $600 billion treasury-bond-buying program through which the Fed flooded the markets with liquidity was scheduled to end by June 30. Some economists have warned that by monetizing the debt, the Fed was debasing the greenback. If this is true, then an end to QE II could give the dollar a boost.

The Treasury International Capital reporting system that collects data on US cross-border portfolio capital positions has shown a marked increase in foreign demand for short-dated treasuries over longer-term treasuries this year, Woolfolk says. This preference may be related to concerns over raising the US debt ceiling, as well as the lack of progress on US budget reform, he says.

Amid the rally in risky assets earlier this year, US investors have been increasingly moving money overseas in search of higher yields, Woolfolk says. At the same time, growing concern over the US fiscal deficit appears to be causing foreign investors to sell long-dated US treasuries in favor of shorter-dated securities and deposits.

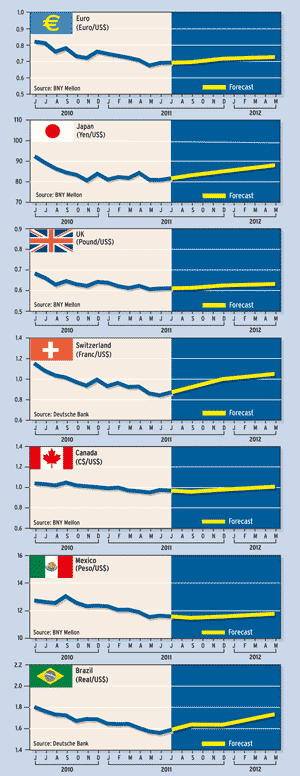

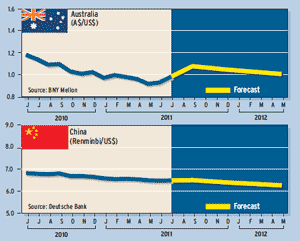

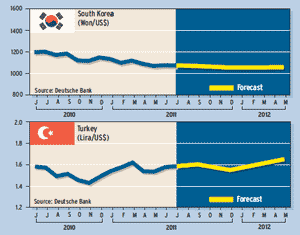

Currency Forecasts

|

CORPORATE FINANCING NEWS / FOREIGN EXCHANGE

CONTAGION RISK WEIGHS ON EURO AS GREECE TEETERS

The euro tumbled against the dollar, the yen and the Swiss franc in mid-June, as European finance ministers reached an impasse on a second Greek aid package and demonstrators clashed with police in Athens. Greeces prime minister George Papandreou tried to push a five-year austerity plan through parliament that would raise taxes, cut spending and put state assets up for sale to avoid default.

The risk of a disorderly Greek default escalated after euro area finance ministers failed to decide how to handle the crisis at an emergency meeting on June 14. A deadlock developed on how to encourage or force the private sector to bear some of the cost of a debt extension, re-profiling or restructuring.

Meanwhile, Moodys Investors Service placed the stand-alone financial strength ratings of three major French banks on review for a possible downgrade, citing their holdings of Greek public and private debt and the potential impact of a possible default.

The Day after Default

Recent market action suggests that investors have largely prepared for the eventual certainty of a Greek credit event, but the markets remain vulnerable to a broader contagion from a eurozone government default across sovereigns, financial-sector and risk assets, says Lena Komileva, London-based global head of G10 strategy at Brown Brothers Harriman. Ultimately, the risk is no longer Greek default but [what happens] the day after Greece defaults.

The markets are reacting to the political risk of the EUs management of the crisis, rather than the probability of a Greek credit event per se, according to Komileva. The difference is between a managed and unmanaged default scenario for Greece, she says. This is what will ultimately mark the difference between a governments solvency crisis and a euro crisis.

Analyses of the direct effects of a Greek default may far underestimate the indirect effects, such as the potential for a chain of disorderly market and bank-asset downgrades similar to what happened after the downfall of Lehman Brothers in 2008, she says. If the culmination of Greek default risk comes at the expense of disorderly developments in sovereign and bank credit markets, then European financial integration and the euro in its current form will be at risk, she says.

Biggest Exposure

Data from the Bank for International Settlements show that French and then German banks have by far the biggest exposure to Greek debt, which should not be a surprise to the market, says Sara Yates, foreign exchange strategist at Barclays Capital, based in London. What is more important for the euro is how and when Greece restructures, she says. Our economics team does not expect Greece to restructure in 2011.

Restructuring Greek debt before the country makes progress in moving toward fiscal balance and putting the country on a more sustainable footing would be putting the cart before the horse, according to Yates. Whats more, an early restructuring would increase the likelihood of contagion to the rest of the periphery, she says.

An early and disorderly restructuring of Greeces debt may occur if Greece fails to enact its five-year austerity plan, but this is only a risk and is not the most likely scenario, Yates says.

Our central scenario remains for the euro area and the euro to muddle through, particularly as Spain has taken some important steps forward, helping it to remain decoupled from the periphery, she says. We expect the euro to continue to shrug off concerns [related to the debt crisis] and to grind higher versus the dollar, supported by the European Central Banks tightening bias, much as it has done over the past 12 months.

Least Ugly Contest

The euro versus the dollar looks to remain a

least ugly contest for the time being, until uncertainty over the US and European debt problems begins to subside, says Michael Woolfolk, a managing director and senior currency strategist in the global markets business of BNY Mellon. Although the outlook for US fiscal and monetary policy is unclear, the outlook for US growth and inflation is for both to move higher, he says. US core consumer inflation rose more than expected in May to post its largest increase in nearly three years, due to increases in apparel and vehicle costs. At an annual rate, the increase was 1.5%, up from 1.3% in April, but still quite low.

The US economic recovery appears to have hit a soft patch, but recent data indicate that the slowdown is less severe than is widely believed, Woolfolk says. The soft patch may not be the double-dip scenario many had feared, he says.

While clearly handicapped by high levels of unemployment and debt service, consumer demand remained brisk throughout the severe winter weather and has been stable this spring, apart from auto sales, Woolfolk says. A rebound in consumer spending this summer should keep growth in GDP near 3% for the second half of the year.

Fed Program Ends

It remains to be seen how the end of QE II, the Federal Reserves second round of quantitative easing, will affect the dollar and the financial markets. The $600 billion treasury-bond-buying program through which the Fed flooded the markets with liquidity was scheduled to end by June 30. Some economists have warned that by monetizing the debt, the Fed was debasing the greenback. If this is true, then an end to QE II could give the dollar a boost.

The Treasury International Capital reporting system that collects data on US cross-border portfolio capital positions has shown a marked increase in foreign demand for short-dated treasuries over longer-term treasuries this year, Woolfolk says. This preference may be related to concerns over raising the US debt ceiling, as well as the lack of progress on US budget reform, he says.

Amid the rally in risky assets earlier this year, US investors have been increasingly moving money overseas in search of higher yields, Woolfolk says. At the same time, growing concern over the US fiscal deficit appears to be causing foreign investors to sell long-dated US treasuries in favor of shorter-dated securities and deposits.

Gordon Platt