SCF is no longer a luxury that only the largest suppliers can afford.

Last year was a memorable year for supply chain finance (SCF) for many reasons. At the start of the pandemic in 2020, buyers began extending membership in their SCF programs to small and midsize enterprises (SMEs), a trend that continued well into 2021.

However, last year’s collapse of Greensill Capital brought some unwanted attention to the little-known and opaque world of SCF.

Lex Greensill, former head of SCF at Morgan Stanley, founded his firm in 2011. The company lasted until March 8, 2021, when it filed for insolvency due to one of its primary insurers pulling the plug on credit insurance for the firm’s debt portfolio.

Most SCF is done on a confirmed basis. But in the case of Greensill, authorities alleged that the firm was providing financing against future receivables that might or might not have ever materialized, which many have described as a form of unsecured lending.

In the wake of Greensill’s collapse, the industry expected unwanted regulatory attention to rear its head; however, a UK parliamentary report, Lessons from Greensill Capital, recognized no need to “bring supply chain finance within the regulatory perimeter for financial services.”

Nonetheless, Greensill’s example highlights the need for greater transparency in SCF. Much information regarding SCF deals and programs is not readily available. As SCF grows and looks to attract a wider pool of investors, and as it supports more-complex financing structures, the need also grows for greater transparency to bring more clarity and certainty. This is particularly so for those companies that rely on SCF to ship and supply goods and services without a 60-, 90- or 120-day wait for payment.

Transparency is even more critical as SCF becomes a haven for nonbanks and fintechs looking to disrupt the field by leveraging the latest technologies, such as artificial intelligence, blockchain and tokenization—or serving a niche, such as SMEs, that large global trade banks typically overlook.

Certainly, Global Finance’s annual SCF awards reflect the changing mix of providers now entering the SCF market. It is tempting to be dazzled by shiny new pieces of technology and ways of doing business that many new tech-savvy entrants to the field claim they deliver. But it remains critical to keep in mind the need to balance the technology hype against other factors, such as a provider’s safety and security, reputation and market standing.

It is equally important not to dismiss the innovation and work some of these newer entrants bring. They may not have the track record or experience of firms that have offered SCF for decades. Still, they have identified a niche that is not currently well served by the usual SCF providers and can be better addressed with newer technologies and business models.

Although long-standing SCF providers continue to invest in their offerings and want to help clients to digitalize more aspects of their supply chains, there is no question that much of this innovation and investment wouldn’t be happening at its current scale or pace without the competitive threat posed by those newer, tech-savvy entrants.

This year’s award winners are a mix of the old and the new and a celebration of those that bring not only financing and a pool of investors, or even technology’s newest bells and whistles, but also a willingness and ability to adapt their services to suit the needs of companies seeking faster and more-affordable forms of financing.

As the SCF market matures, many now realize that one size does not fit all and that a wide range of solutions and approaches are needed to address the differing and varied needs of suppliers at every stage or tier of the supply chain.

Among the winners of this year’s Global Finance Best Supply Chain Finance Providers, there is a growing recognition that SCF needs to benefit all parts of the supply chain. It’s no longer a special solution for only the largest suppliers in key markets, according to Orbian, but also provides early liquidity to suppliers in more-vulnerable countries.

Add into the mix a global pandemic that caused significant demand and supply shocks in global supply chains and cash shortfalls for companies that have had to endure months of disruption and lockdowns, and we have the kind of perfect storm that allows SCF to flourish and potentially realize its full potential. Despite these recent developments, there still exists the trillion-dollar trade financing gap. But a meaningful shift, reflected in the achievements of this year’s winners, is underway as new solutions enable all tiers of the supply chain to benefit from early payment for goods or services provided.

Methodology: Behind the Rankings

Global Finance editors select the winners for both the Trade Finance Awards and the Supply Chain Finance Awards with input from industry analysts, corporate executives and technology experts. The editors also consider entries submitted by financial services providers, as well as independent research, taking into account a set of objective and subjective factors. This year’s ratings, which cover 102 countries and eight regions, were based on performance during the period from the fourth quarter of 2020 through the third quarter of 2021.

It is not necessary to enter in order to win, but experience shows that the additional information supplied in an entry can increase the chance of success. In many cases, entrants are able to present details and insights that may not be readily available to the editors of Global Finance.

The winners are those banks and providers that best serve the specialized needs of corporations as they engage in cross-border trade. The winners are not always the biggest institutions, but rather the best: those with qualities that companies should consider most carefully when choosing a provider. Global Finance uses a proprietary algorithm with criteria—such as knowledge of local conditions and customer needs, financial strength and safety, strategic relationships and governance, competitive pricing, capital investment and innovation in products and services—weighted for relative importance. Each entity is rated on each separate criterion. The algorithm incorporates those ratings into a single numeric score, with 100 equivalent to perfection. In cases where more than one institution earns the same score, we favor local providers over global institutions and privately-owned over government-owned institutions.

|

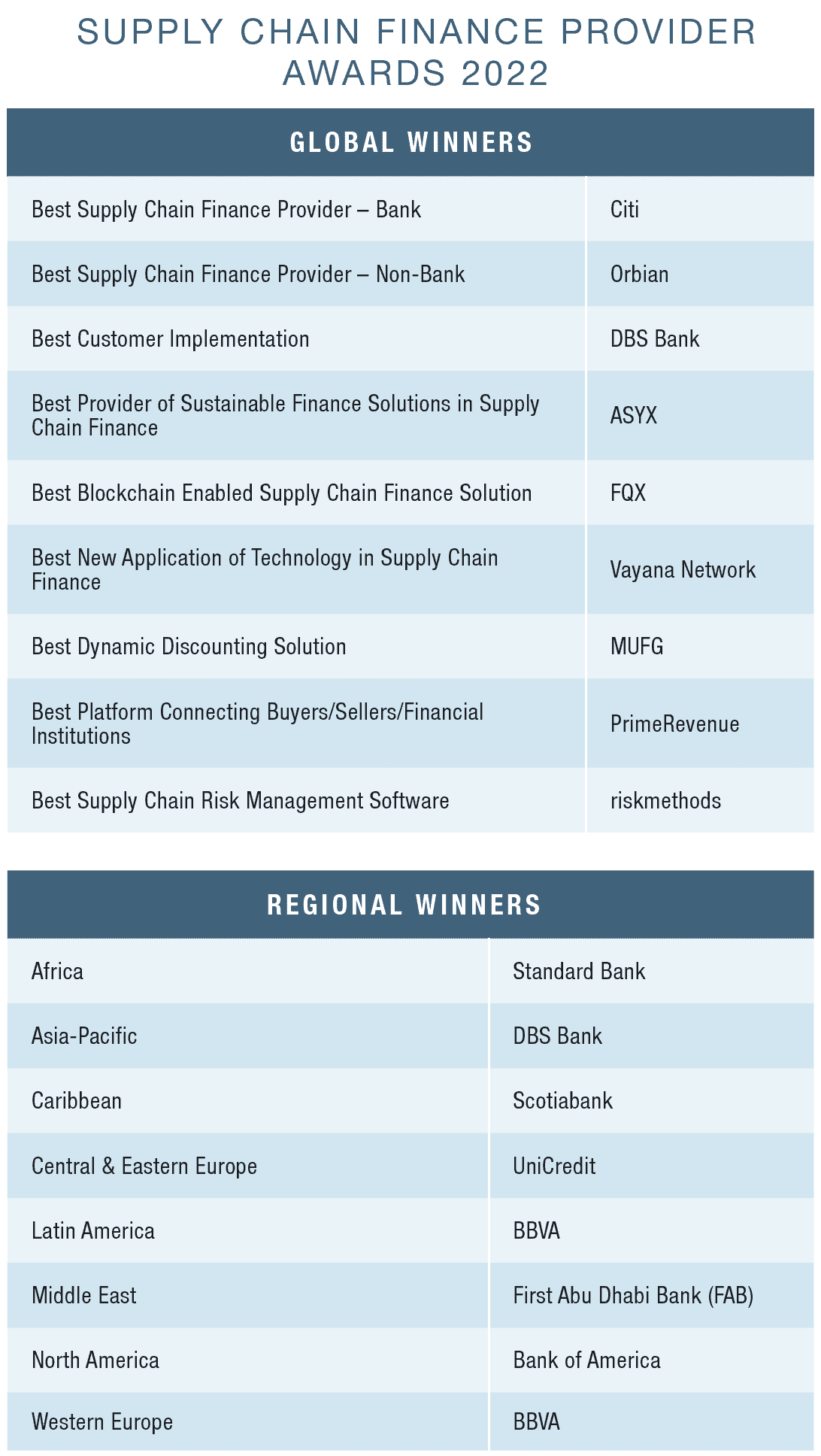

GLOBAL WINNERS |

|---|

BEST SUPPLY CHAIN FINANCE PROVIDER — BANK

Citi

Winning the global award for Best Supply Chain Finance Provider–Bank is not just about the number of markets served or the number of supply chain finance programs a provider supports. With one of the largest transaction banking networks, Citi boasts encouraging metrics on both counts. But more important, especially during a pandemic, is its ability to scale and implement its services quickly as supply chains adjust to the new business norms.

Liquidity remains a significant portion of any SCF program, and Citi’s global reach permits it to source liquidity from its balance sheet or a pool of investors. A noteworthy addition to the bank’s SCF toolbox is its Dynamic Discounting offering, which it launched in Europe and the US. The service enables buyers to make cash more readily available to mid- to long-tail suppliers, where demand for financing is typically the greatest.

BEST SUPPLY CHAIN FINANCE PROVIDER — NON-BANK

Orbian

Fintechs in SCF come and go, but Orbian, founded in 1999 by Citi and enterprise-software provider SAP, continues its mainstay status. The company focuses on supporting buyer-led SCF programs via innovations, such as Express SCF, that are designed to make SCF accessible to all suppliers regardless of their size or location.

Alongside its traditional SCF programs, which Orbian offers in more than 50 countries, Express SCF facilitates early payment in more than 100 countries. The fintech also recently launched a fixed rate offering—an alternative to pricing programs based on Libor or other floating-rate mechanisms—that lets suppliers lock in a rate on any discounts for up to five years. It is 20 years’ worth of collected data, permitting better risk modeling, that makes such a service possible, according to Orbian.

BEST CUSTOMER IMPLEMENTATION

DBS Bank

Leveraging its digital-first strategy and application programming interface (API) suite, Singapore-headquartered DBS Bank helped renewable-materials provider Stora Enso monetize its growing accounts receivable portfolio and remove costly, inefficient and paper-based processes for managing its incoming receivables. As the company’s days sales outstanding (DSO) had doubled from 60 to 120 days with growing cross-border transactions, its finance team were spending more time physically matching invoices and custom and tax declaration forms with their corresponding payments. This gave them little visibility on the status of incoming payments.

Using a combination of DBS Bank’s Supplier Payment Services, providing automatic and selective payments for suppliers; its digital supplier onboarding tools; and its DigiDocs offering, the bank made the customer journey entirely paperless for Stora Enso. The vendor’s financial team used DBS’ digital corporate banking platform and Swift gpi for cross-border payments to trace incoming payments from buyers in real time.

The bank also set up a digital accounts receivable purchase program to ease the impact that Stora Enso’s widening DSO had on its working capital and to increase its cash conversion cycle so that the company could be paid quicker.

“Teams on both sides worked very well and effectively together to guarantee a smooth process and quick implementation and ramp-up all around,” says Wei Li-Tuomela, vice president and head of Treasury at Stora Enso.

BEST PROVIDER OF SUSTAINABLE FINANCE SOLUTIONS IN SUPPLY CHAIN FINANCE

ASYX

Sustainability may be a current buzzword in finance, but it does not always easily translate into action for small and midsize enterprises (SMEs). For one thing, many systems that track sustainability as goods and services move through global supply chains are often geared for larger companies. The mission of Southeast Asian supply chain integration firm ASYX is to facilitate faster business expansion for SMEs using various forms of supply chain financing and to help them better understand and integrate sustainability into their systems.

With a strong focus on agroindustry and forestry value chains, ASYX is well positioned to support sustainable financing initiatives that lead to real change. In Indonesia, it supports environmental efforts to preserve rural peatlands and mangroves. In the apparel sector, it is helping SMEs that produce natural yarns and fibers in rural areas to scale up their business and become more agile.

BEST BLOCKCHAIN-ENABLED SUPPLY CHAIN FINANCING SOLUTION

FQX

Describing itself as “the first market-ready solution for eNotes,” which are unconditional promises to pay specific sums to other parties on a selected date, FQX combines an old concept with new technology in the form of its Swiss Trust Chain. This is a private blockchain from Swisscom and Swiss Post that incorporates a patent-pending authentication mechanism, which FQX says is based on regulated and qualified electronic signatures provided by Swisscom.

FQX’s eNote infrastructure can be integrated into the financing platforms of banks and fintechs, “[allowing] for the standardized and globally scalable transfer of unconditional promises to pay, radically facilitating supply chain and corporate finance,” the vendor adds. For example, companies can use eNotes to generate free cash flow, improve working-capital metrics and ultimately replace inefficient and costly paper-based trade and supply chain finance processes.

BEST NEW APPLICATION OF TECHNOLOGY IN SUPPLY CHAIN FINANCE

Vayana Network

With a focus on SMEs, India’s Vayana Network leverages plug-and-play APIs, data analytics and digital technologies to make it easier for companies of any size to participate in SCF programs.

For one fast-moving consumer-goods vendor, assessing, researching and servicing an extensive network of distributors proved to be time-consuming and expensive. However, using real-time upstream data to identify creditworthy distributors, Vayana provided financing offerings that ensured that just as much of the distribution chain would be covered.

Vayana’s platform offered the consumer-goods company a range of financing possibilities beyond standard reverse factoring, including receivables securitization and a “specially structured last-mile retailer program.” In addition to its data analytics capabilities, being the largest goods and services tax (GST) Suvidha Provider for API-based connections to India’s GST network for tax filing and e-invoicing also has its advantages, says Vayana, as it allows it to analyze data, assess risk, onboard partners and disburse and collect money quickly.

BEST DYNAMIC DISCOUNTING SOLUTION

MUFG

Dynamic discounting, which enables buyers to use their balance sheets instead of banks, provides suppliers with early payment in return for a sizeable discount on their invoices. It is typically dominated by fintechs. Nonetheless, Japanese banking giant MUFG, which entered US SCF following its 2019 acquisition of GE Capital’s Trade Payables Services platform, is one of the few banking providers whose proprietary SCF platform supports standard SCF and dynamic discounting.

For one large US-based customer looking to improve its working-capital metrics across different business units in various countries, MUFG proposed a solution that combined a receivables purchase program for its largest suppliers and dynamic discounting for its remaining suppliers. According to the bank, the dynamic discounting service delivered a yield of 12% APR and $50 million to $60 million in “realized supplier discounts” or reductions in the cost of goods sold year-on-year. In total, the combined program realized more than $1 billion in cash flow benefits, according to MUFG.

BEST PLATFORM CONNECTING BUYERS/SELLERS/FINANCIAL INSTITUTIONS

PrimeRevenue

The Atlanta-based software-as-a-service SCF platform provider PrimeRevenue connects more than 30,000 customers in more than 80 countries. Its global funding network includes more than 100 partners and supports more than 30 currencies. The platform’s ability to tap into multiple funding providers has led customers to expand their SCF programs to reap the benefits of better financing availability.

A newly added function, SurePay, speeds up payments to suppliers by letting buyers consolidate their entire supplier base onto a single payment platform and eliminating the need to manage multiple enterprise resource planning (ERP) and payment systems.

BEST SUPPLY CHAIN RISK MANAGEMENT SOFTWARE

riskmethods

Getting ahead of supplier risk issues that can crop up at any time in complex global supply chains is the holy grail for many companies. But in a business primarily based on a complex web of international relationships, building in a certain level of predictability to warn companies how their suppliers could be affected by geopolitical, economic or other risks is challenging at the best of times.

However, Munich-based riskmethods’ Risk Intelligence engine eliminates much of the guesswork. The engine analyzes millions of data points from media and other sources to identify relevant supply chain threats in real time. Its offering processes more than 2.5 million potentially relevant risk indicators and conducts between 400,000 and 500,000 risk assessments per month.

How can companies distinguish between what is just noise and what is relevant? The platform’s Noise Cancellation feature alerts users to only the most critical information, so that users are not bombarded with false alarms.

|

REGIONAL WINNERS |

|---|

AFRICA

Standard Bank

Few banks understand the intricacies of trading in local African markets as well as Standard Bank does. With a heritage of 160 years in the region and a robust sub-Saharan network, the bank possesses an in-depth knowledge of local market regulations and customs. Leveraging the strong trading ties between Africa and China, Standard Bank was also one of the first African banks to forge a relationship with a Chinese bank, namely the Industrial and Commercial Bank of China, which acquired a controlling interest in the bank in 2015. Their partnership lets customers in the Africa-China trade corridor benefit from the bank’s structuring and technology expertise. Standard Bank works closely with companies in the oil and gas sector, structuring solutions that improve working capital and liquidity metrics while assuming the credit and market risk from receivables purchasing programs. The bank even supports holistic solutions, integrating SCF with logistics management.

ASIA-PACIFIC

DBS BANK

Much of DBS’ success in growing its SCF business in the Asia-Pacific region can be attributed to its efforts to be a digital-first bank. This not just about how many markets it is in throughout the region—although that’s important—but also the bank’s expansive API suite. At last count, the suite had more than 200 corporate and institutional banking APIs, with almost a third of them being trade related. Through APIs, the bank can help customers transition to paperless trade more seamlessly by making it easier for the client’s ERP and trade systems to interact with bank systems in real time. Companies can submit documents and financing requests digitally with little or no manual effort, resulting in faster processing times and greater visibility across a transaction’s lifecycle.

A digital-first mindset and a comprehensive suite of APIs mean DBS can also partner with fintechs looking to disrupt the trade and supply chain finance industry more readily. Among the fintechs with which the bank has worked are AntChain, a blockchain-based trade platform; and CredAble, an Indian fintech that provides working-capital finance for SMEs.

CARIBBEAN

Scotiabank

Although Scotiabank has scaled back its presence in the Caribbean and Central America, it still operates in 25 countries across the region, with strong historical ties to key markets—such as Jamaica, where it has supported trade since 1889. The bank has the aspiration to help its customers expand their business, wherever they do business, “across Canada, into the United States, the Caribbean and Central and South America,” the bank writes in its 2021 annual report. “Our long history across the Americas has given us a deep understanding of how these countries operate, the strengths of their economies, and the aspirations of the people who live and work there.”

CENTRAL & EASTERN EUROPE

UniCredit

Instead of a one size fits all approach to SCF, UniCredit uses in-house innovation and collaborates with fintechs to develop fully customized working capital offerings to meet the financing needs of its customers in Central and Eastern Europe. In Russia, for example, the bank devised a digital agent factoring service for accounts payable management to support the entire supply chain for a local manufacturing client. In Slovenia, the bank structured a program that benefited buyers and suppliers—the buyers extended their payables while the suppliers received their payments sooner—despite the challenging time frames and an entirely new structure for the bank’s local branch. In addition, UniCredit banking teams in different countries—the Czech Republic, Germany and Romania—worked together, with the help of a fintech, to deliver a bespoke SCF offering for an international customer.

LATIN AMERICA

BBVA

The Spanish bank has provided local banking services in Latin America for more than 40 years, and its SCF programs encompass core markets, such as Mexico, Peru and Colombia. In 2020, the region accounted for more than half of the bank’s overall profits. Moreover, the region is of even greater value to the bank following the recent divestment of its US retail banking operations, according to analysts. The bank has based the bulk of its SCF programs in Mexico and Peru, where BBVA boasts a more than 20% market share. In 2020, BBVA launched its new cloud-based global SCF platform, which provides a single point of access and full traceability of all invoices and payments. The platform supports payments in local currency in Mexico, Peru and Colombia. In addition, BBVA plans to roll out support for the Argentinian market later this year.

MIDDLE EAST

First Abu Dhabi Bank (FAB)

As the largest banking group by assets in the UAE, First Abu Dhabi Bank is one of the first banks in the Middle East to develop a fully automated SCF offering, which is in production with several international customers and programs. Throughout 2021, the bank implemented various SCF programs collaborating with government agencies to support SMEs. It partnered with the Department of Finance in Abu Dhabi and health insurer Daman to provide a 6 billion dirham ($1.6 billion) SCF program to ensure rapid payment of receivables for SMEs in the health care sector. Other noteworthy deals include an Islamic SCF program that supports suppliers in the UAE, and acting as co-lead arranger on a program supporting SME suppliers and corporates for one of the major members of the Gulf Cooperation Council.

NORTH AMERICA

Bank of America

With solid growth in its SCF portfolio in 2020, Bank of America witnessed continued growth throughout 2021. The North American corporate banking giant, which invests billions in technology annually, looks to compete with innovative fintechs in SCF by investing in APIs and data analytics to deliver greater operational efficiencies and insights to its clients and their suppliers. For example, the bank now provides real-time payment status information directly to buyers’ ERP systems via APIs. Its Supplier Enablement Portal, which the bank rolled out to North American customers in 2020, uses data analytics to analyze buyers’ spending with suppliers, aiding supplier segmentation and prioritization of strategic suppliers for onboarding to buyer-led financing programs.

WESTERN EUROPE

BBVA

BBVA’s global SCF platform, which it launched in 2020, enables customers to pay suppliers in up to 20 currencies. The new cloud-based platform is designed to make it easier for the bank to onboard the entire supplier base of creditworthy buyers without imposing any limits on the number of invoices or amount of financing. Buyers can also more easily track invoices and payments to suppliers. Given that its biggest markets are based in its European stronghold—where the bank is headquartered—and in South America, the bank is geographically diversified enough to meet its European customers’ local or global SCF needs.