Banks enlist in recovery effort.

Chinese banks, including many of the institutions making up Global Finance’s ranking of the Safest Banks in China, are at the forefront of the government’s response to the economic damage caused by the coronavirus pandemic.

The world’s second largest economy faces a dramatic decline in GDP, forecast at 1.9% in 2020, down from 6.1% in 2019, according to the International Monetary Fund. Regulators are pressing the banking sector to reduce financing costs for borrowers, particularly small and medium-sized enterprises, by lowering lending rates below the benchmark Loan Prime Rate (LPR). The LPR, which has been in effect for over a year, must be applied to new floating-rate loans beginning in 2021. The change will benefit borrowers as lower rates are expected to persist, further pressuring banks’ net interest margins and profitability.

Regulators have also imposed a moratorium on payment of principal and interest on loans until March 2021, shifting the impact of loan portfolio deterioration forward. The moratorium affects 4% of non-performing loans (NPLs), ¥7 trillion (US$1 trillion).

Systemwide, NPLs are running at 1.96%, up slightly from 1.86% as of year-end 2019; Fitch Ratings expects NPLs to rise to 3.5% of loans by year-end. Accordingly, loan loss reserves are up 41% as banks accelerate recognition of loan losses by charging them off. The China Banking and Insurance Regulatory Commission (CBIRC) expects a 48% jump in loan charge-offs in 2020 over 2019 to ¥3.4 trillion (US$490 billion). With only one-third charged off as of the end of the second quarter, further earnings pressure is expected to be felt for the remainder of this year and beyond.

The pandemic’s impact on the sector is estimated to represent a profit reduction of ¥1.5 trillion (US$200 billion) in 2020; profits were down 9.4% in the second quarter year-over year, to ¥1 trillion (US$146 billion).

While Chinese banks are well capitalized at 14.2% above the 10.5% regulatory capital adequacy ratio, hits to profitability during the crisis have caused the capital ratio for the sector to drop 50 basis points. The People’s Bank of China has provided some relief by lowering the required reserve ratio and initiating lending facilities to provide credit to the economy.

But the decline in international trade poses risks to the Chinese economy as well as the banking sector. The World Trade Organization (WTO) sees global trade contracting by 9.2% in 2020, but forecasts an improvement, reflecting China’s ability to enact recovery measures. On September 15, 2020 the WTO indicated the U.S. had violated international trade rules by imposing tariffs on billions of dollars’ worth of Chinese goods in 2018. It was just the latest skirmish in a long-running battle, but the dispute is likely to linger as the Trump administration has blocked the appointment of judges to the WTO’s Dispute Settlement Body (DSB) who would be required for the resolution of international trade disputes. The U.S. notified the DSB last month of its decision to appeal the case, knowing the WTO does not have an adequately staffed appellate body to address the appeal.

The Rating’s the Thing

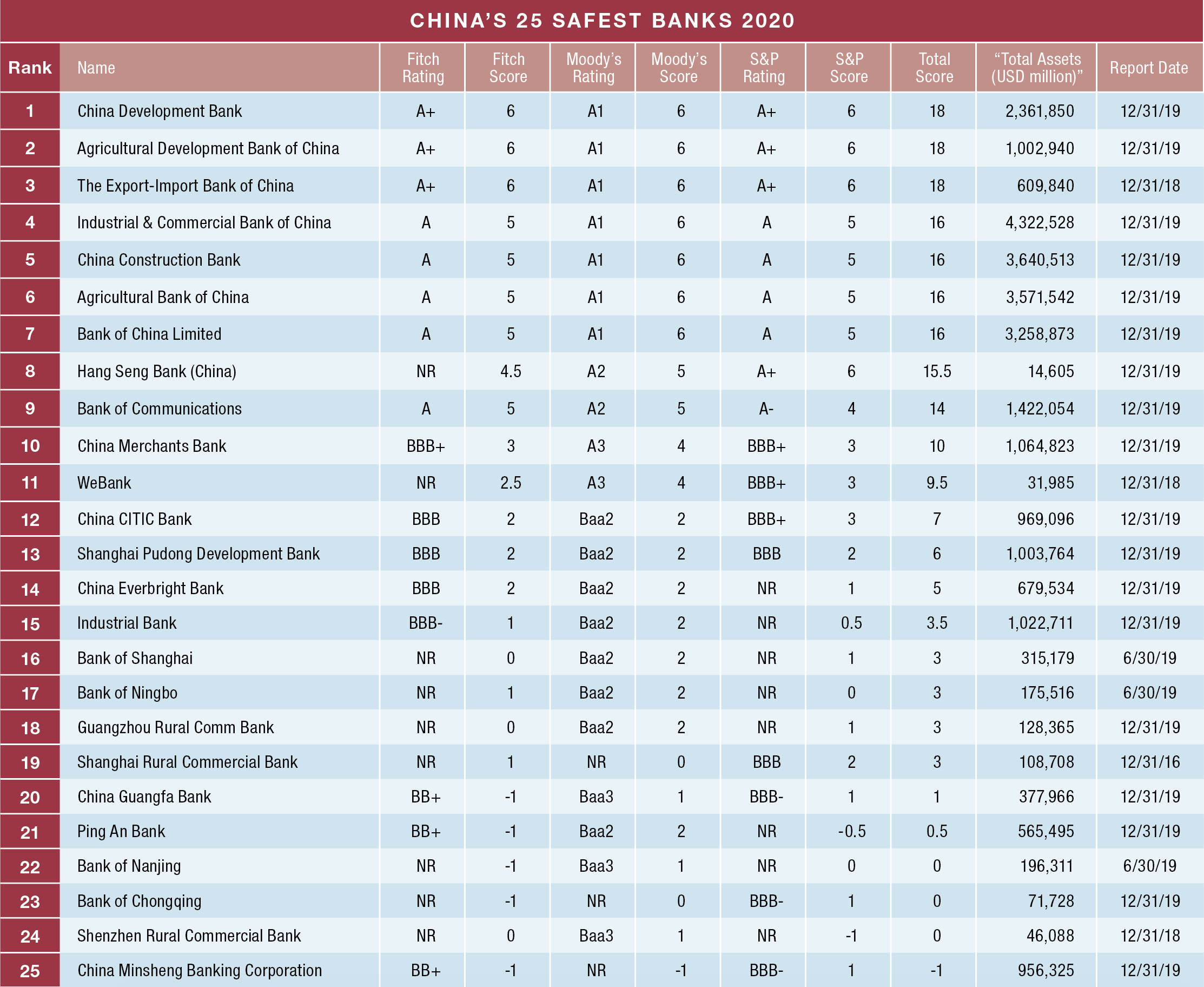

Ratings agency decisions were the salient factor behind most of the moves in Global Finance’s 2020 Safest Banks in China ranking. WeBank, a digital institution, is a new entrant at #11; Moody’s (A3) and Standard & Poor’s (BBB+) initiated coverage this year. Shenzhen Rural Commercial Bank is also a new entrant as Moody’s began coverage with a Baa3 rating in November 2019. Guangzhou Rural Commercial Bank fell three places; it is no longer rated by S&P. China Guangfa Bank rose four spots to #24 as S&P initiated coverage with a BBB- rating.

Methodology

The scoring methodology for the Safest Chinese Banks follows that used in our other Safest Banks rankings. A rating of AAA is assigned a score of 10 points, AA+ receives nine points, down to BBB- worth one point and BB+ worth -1 point, and so on. When a bank has only two ratings, an implied score for the third rating is calculated by taking the average of the other two and deducting one point. When a bank has only one rating, an implied score for the second rating is calculated by deducting one point from the actual rating, and an implied score for the third rating is calculated by deducting two points from the actual rating.