As pandemic response continues to reshape human behaviors and attitudes, banks are strengthening in-house innovation teams and tapping broader networks to stimulate fresh ideation in financial services.

After a surge of innovation in 2020 as Covid-19 created new needs and accelerated take-up of digital channels, the past year saw only a modest pushing of the fintech envelope. Bank spending on tech grew slowly in 2021; Forrester, a technology consultancy, now expects it to see double-digit growth in 2022.

This is not to say 2021 was an innovation-free zone, just that groundbreaking innovations by banks were thin on the ground. This is our seventh year of this annual special issue devoted to financial innovation. The following pages recognize innovation standouts among banks and fintechs, as well as the most interesting finance-sector innovations of the year worldwide. We also honor excellence at the regional and category levels. Finally, we include our popular annual review of the world’s leading fintech innovation labs.

In our years studying finance innovation, we have come to recognize a certain ebb and flow, and today’s relative calm masks often robust activity that will later be revealed. This year, banks entering our awards bragged most about their innovations focused on user experience or payments—unsurprising when you consider how the pandemic brought a greater focus on both. But overall, in reviewing entries (required for all but the global-level awards), we saw a deepening embrace of change and an enthusiastic push to bring about the best possibilities the future may offer.

Still, banks have a long way to go before they can shake off their legacy shackles and match the agility and customer-centric way that fintechs innovate. The record VC investment flowing into the sector in 2021 should keep fintechs hungrily snapping at the tech toes of banks.

It’s not all about competition, however, as many banks rightly see fintechs as enablers and partners on the journey of discovery. Whether its payments, savings, loans or treasury technology, tech-centric upstarts experiment more nimbly than banks, and can help increase the speed and scale of innovation. Open banking, application programming interfaces and no code/low code are all helping bring about a more inclusive culture for the development of innovation. These features were characteristic of many of this year’s innovation leaders.

|

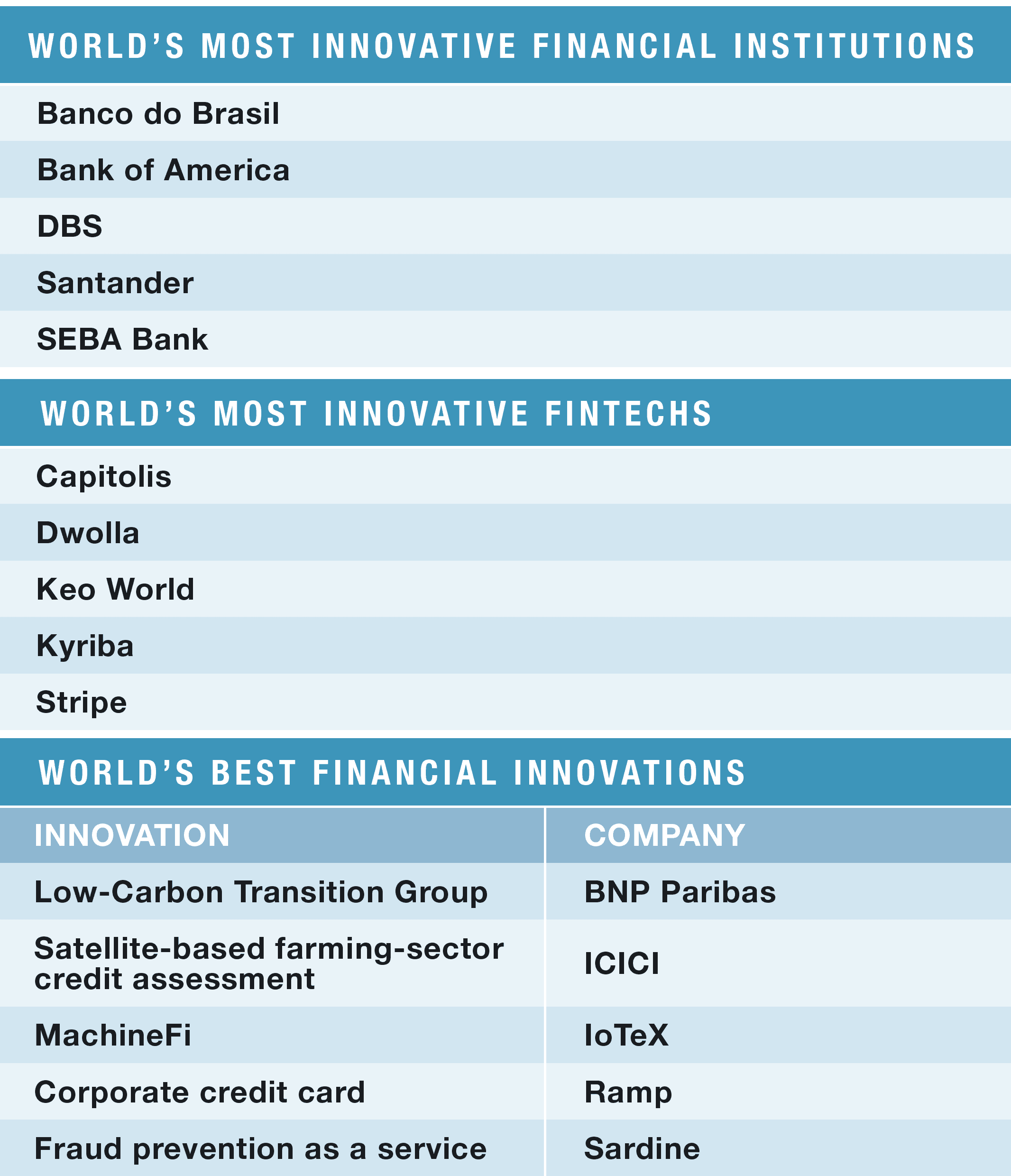

GLOBAL TOP FIVE MOST INNOVATIVE FINANCIAL INSTITUTIONS |

|---|

BANCO DO BRASIL

Banco do Brasil developed Mappiá, the first satellite crop-monitoring solution using artificial intelligence (AI). Brazil is one of the world’s largest grain producers and a global leader in the production and export of soy, with agriculture accounting for about 20% of the country’s GDP. The bank is the main financial agent in Brazil’s agribusiness and one of the world’s largest agricultural credit agents.

During the 2020-2021 harvest, Banco do Brasil was responsible for about $21.5 billion contracted for over 560,000 credit operations, about a 58% market share. While crop inspections are a part of these contracts, the bank had been unable to inspect many of the 71,000 financed soy and corn plantations to validate production numbers.

Monitoring the plants with satellite imagery and AI helps the bank identify irregularities and mitigate any potential credit risk. Mappiá uses financing data from agribusiness customers to determine where production issues may lie. The platform relies on a big data infrastructure and 16 machine learning models customized for the country’s different regions, to address variations such as vegetation and soil.

Mappiá also helps the farmers make decisions regarding their crops, by providing information and data integral to those decisions. The bank also works with Brazil’s National Institute of Meteorology and provides producers with climate information to inform their decisions regarding their crops.

BANK OF AMERICA

To help customers solve their most pressing challenges, Bank of America’s innovations spanned multiple products and processes with regards to mobile banking, payments, cash management and trade finance. The bank’s solutions change how consumers and businesses transact and are firsts for the industry.

At the center of the bank’s technology delivery is CashPro, which was created in-house and offers clients a treasury management solution for liquidity, payments, trade finance and reporting. To improve access, the bank recently introduced the CashPro API (application programming interface), which reduces the time to onboard clients. Additional innovations announced this year for the CashPro App include ACH Positive Pay, which gives customers more fraud protection; and CashPro Forecasting, which uses machine learning models to produce more-accurate cash forecasting.

Global Card Access is the first commercial card platform that functions as a single point of access for multiple users and solution sets. With this omnichannel approach, clients don’t need multiple credentials for different platforms. To address the shift in business-to-consumer (B2C) payments with increased adoption of mobile and electronic payments, Recipient Select is the first B2C digital platform that lets clients collect and manage their data and payment choices through a secure portal.

DBS

DBS Bank worked to transform how banks operate and markets function in Asia. The bank’s products provide commercial and retail customers with more-seamless processes. The bank is proceeding to digitalize Asia’s capital markets, starting with its FIX Marketplace product for the fixed income markets. This fully digital and automated execution platform is the first where issuers can connect directly with investors. This product is working to create a more inclusive and accessible market.

Working with different technologies, DBS is developing innovative products like its 24/7 multicurrency payment settlement on Partior. Partior is the first live permissioned, blockchain-based clearing and settlement platform for commercial bank money. This platform prevents cross-border payments from needing to travel through a network of banks and time zones. It thereby eliminates associated inefficiencies. Instead, Partior uses a programmable real-time value transfer that eliminates friction in cross-border payment processing.

DBS developed solutions for the country’s biggest industries. Close to 50 million tons of marine fuel was sold in Singapore in 2020, and DBS is the first bank to finance bunker fuel deliveries with a digital bunker delivery note rather than a physical copy. This solution eliminates potential human error due to manual processes and incorporates real-time data connectivity.

To be more sustainable, the bank is changing how it does business. Its full-service branches now use the Internet of Things and robotics, integrating these with live-streamed video analytics data, to augment tasks typically performed by branch staff.

DBS is also facilitating processes for customers. Among such processes are the bank’s electronic document verification that leverages AI, and biometric authentication for the Hong Kong government-issued identity card. Now, customers can open accounts in about 10 minutes.

SANTANDER

Santander developed innovations advancing the agriculture sector. The bank has teamed with Agrotoken, a multichain infrastructure built on Ethereum, Algorand and Polygon networks, to provide loans to farmers.

The tokens issued represent the grain that has been stored, with one token equal to one metric ton (about 1.1 US tons). Each type of grain will have its own token, with SOYA for soy, CORA for corn and WHEA for wheat. The token’s value in US dollars is determined by the commodity’s price, and farmers can store these tokens in their digital wallets on PCs and mobile devices. Farmers can then exchange the tokens for various items like crops, automobiles, machinery, gasoline or a prefunded credit card, and can also use them as collateral for loans. Once the grain is released from the silo, the token is canceled.

This European bank is also the first to launch a payments solution for customers to make transfers into Brazil in real time. PagoNxt is the technology backbone for this new service. The time frame for payments through this platform is shortened from days to minutes, and intermediaries and foreign exchange documentation are no longer needed.

Santander Green Investment is an investment platform for renewable energy projects in Spain that are under development. Through this initiative, Santander invested in nine solar and wind projects with a combined capacity of about 500 Mw. The bank’s self-governance model expedites investments.

SEBA BANK

SEBA Bank is a fully integrated, Finma-licensed, digital assets banking platform that is a bridge between digital and traditional assets. The bank offers investors its Gold Token representing holdings of physical gold. With this digital asset, investors can demand to take physical possession of the metal from partner refineries. The Gold Token sets a new standard for stablecoin.

SEBA Earn is an institutional-grade solution for customers who want to earn yield on crypto holdings. This product addresses the institutional demand to manage a range of digital-asset use cases that include staking, decentralized finance, and centralized lending and borrowing.

With Banque de France, SEBA conducted a central bank digital currency (CBDC) pilot. They tested the delivery of TARGET2-Securities in a test environment. Based on the deployment of a smart contract, Banque de France simulated CBDC issuance on a public blockchain.

|

GLOBAL TOP FIVE MOST INNOVATIVE FINTECHS |

|---|

CAPITOLIS

Capitolis builds technologies that speed up and simplify how banks transact with each other, addressing capital market constraints in equities and foreign exchange. Capitolis works with more than 100 big banks and has transacted over $60 billion “notional” (a nominal amount used to calculate payments made on financial instruments) from over 30 investors. The company has optimized over $13 trillion in trades through its trade compression platform. By connecting market participants and automating manual workflow, Capitolis helps firms mitigate inefficiencies linked to reserved regulatory capital, tightening client credit capacity and reducing costs resulting from manual processes.

The New York–headquartered Israeli company can also come up with solutions to capital market problems. In response to the war in Ukraine, Capitolis was approached by a large network of global banks to design a solution to reduce their exposure to Russian rubles. Through its trade compression platform, Capitolis was able to reduce these large exposures, promoting financial soundness and stability for the benefit of the whole capital markets system. Ruble optimization is a first for Capitolis, and the company says it will continue offering a Russian ruble compression run for as long as it is needed.

DWOLLA

Payments platform Dwolla launched its real-time payments (RTP) option in April 2021, in partnership with Cross River Bank, allowing businesses’ clients to integrate Dwolla’s payment API (application programming interface) to connect with RTP-enabled financial institutions and send funds to a bank account within seconds. Existing clients can change a single line of code to initiate an RTP transaction using the Dwolla API. Dwolla has also expanded its library of drop-in components, to help lighten the technical lift that comes with integrating a payment API, offering a low-code solution that reduces a payments integration by thousands of lines of code. In July 2021, Dwolla partnered with financial data platform MX to help customers automate bank account verification, connecting any depository account securely and easily.

By building a flexible API, Dwolla enables companies of all sizes and technical expertise to implement account-to-account payment solutions. For startup companies, Dwolla’s scalable and customized low-code solution allows them to easily send and collect payments or facilitate transactions. In 2022, Dwolla plans to expand beyond the US with the introduction of foreign exchange transactions via RTP, ACH and push-to-debit functionality.

KEO WORLD

Business-to-business (B2B) buy-now, pay-later (BNPL) startup KEO World was founded in 2020 and issues Keo American Express (Amex) Virtual Cards and credit lines with a quick digital approval process for small businesses. The Miami-headquartered company is working to extend its footprint from North America to Latin America; and in 2021, Keo formed an international alliance with Amex to become the first nonbank financial institution to be granted an issuing license by Amex Mexico. Following a fast digital approval process, small to midsize enterprises (SMEs) are issued a Keo Amex Virtual Card and a credit line. Keo’s Workeo product allows business buyers to access key inventory on credit, and suppliers to increase their recurring sales, enhancing working capital management via an all-digital, frictionless and low-cost inventory financing platform. Keo World recently announced a seven-year debt facility of up to $500 million from asset management firm, Hayfin Capital Management to boost its supply chain finance purchasing power for SMEs.

KYRIBA

In October 2021, the launch of Kyriba Working Capital Solutions furthered the cloud-based treasury-software provider Kyriba’s efforts to close the reported $3.4 trillion trade financing gap and help corporate buyers support suppliers, especially at-risk SME suppliers. Kyriba says the new capabilities will increase access to liquidity, mitigating supply chain risk. They include purchase order financing and a receivables financing platform to help CFOs enhance and modernize their enterprise liquidity programs.

In collaboration with Societe Generale, Kyriba launched a joint treasury management solution, including payment automation and fraud management functionalities, to make treasury management smoother and easier for the French bank’s corporate clients. Kyriba also launched its Open API platform to enable “composable” (modular, responsive and open-form architecture) technology solutions for CFOs, CIOs and treasurers, accelerating the next generation of finance innovation. Finally, Kyriba teamed up with BNPL payments fintech Openpay to allow its customers to use Openpay’s OpyPro software-as-a-service B2B payments solution to manage their trade accounts end to end, including applications, credit checks, approvals and account management.

STRIPE

Having earned its stripes removing many of the pain points behind online payments, the Irish-American financial services and SaaS company Stripe spent 2021 launching a suite of innovations that go beyond payments. In December 2020, Stripe launched Stripe Treasury to enable Stripe clients to provide bank accounts to their customers. It also provided an inkling that Stripe’s fertile environment for programmers and developers was going to get creative with its innovations. In 2021, Stripe never took its foot off the innovation accelerator. First came the launch, in May, of Payment Links—a no-code method for businesses to create a full payment page with just a few clicks. Then in June followed two more launches: Stripe Tax, to help businesses automatically calculate and collect sales tax, value-added tax, and goods and services tax in over 30 countries; and Stripe Identity, a simple and low-code way to verify identities online. In September came Revenue Recognition, built especially for fast-growing businesses with subscription-based or recurring revenue models, to simplify accounting and automate financial reporting. Finally, in December, Stripe upped its commitment to fighting the climate crisis with Stripe Climate, which allows any business to automatically direct a fraction of its revenue on Stripe toward carbon-removal technologies. Stripe is the most valuable privately held fintech in the US, at $95 billion. The company’s Irish founders, Patrick and John Collison, look set to continue their developer-focused spree of innovation with new products that will help build the best software platform for running an internet business.

|

GLOBAL TOP FIVE INNOVATIONS |

|---|

LOW-CARBON TRANSITION GROUP: BNP PARIBAS

Transitioning to net-zero greenhouse gas emissions is never easy for companies. The process needs significant investments while companies reengineer their operations and supply chains to make them more sustainable and less impactful on the environment.

Recognizing the challenges that environmental, social and governance (ESG) concerns present for its corporate and institutional clients, French bank BNP Paribas scaled up its support for its customers’ decarbonization journey with an October announcement regarding its Low-Carbon Transition Group, which provides access to the full spectrum of expertise across the bank.

BNP Paribas describes the group as “a dedicated and agile organization to support its clients around the world” that brings together more than 250 professionals, mobilizing a wealth of corporate social responsibility (CSR) and ESG expertise from across the bank, including its car leasing business Arval, BNP Paribas Real Estate’s expertise in high-performance buildings, sustainable investment funds provided by its asset management arm, and its Company Engagement/CSR team’s biodiversity and climate expertise.

CREDIT ANALYSIS INCORPORATING SATELLITE DATA: ICICI

India’s ICICI Bank is the first bank in India, and one of the first globally, to have looked to space to help it assess the creditworthiness of its farming customers. The bank is using earth-observation satellite data to track variables like rainfall and temperature, soil moisture levels, crop yields and cultivation area over several years. Access to such data has dispensed with the need for bank staff to travel to remote locations to verify information like crop quality and irrigation levels. The satellite data is then combined with financial and demographic data to help expand access to credit for farmers. The bank first tested the new methodology in 500 villages in the states of Maharashtra, Madhya Pradesh and Gujarat; and it is now scaling up the process to include more than 63,000 villages.

MACHINEFI: IOTEX

According to global consultancy McKinsey, the Internet of Things (IoT)—a network of internet-enabled devices and sensors—could generate a $5.5 trillion to $12.6 trillion market worldwide by 2030. In 2021, Juniper Research estimated that the number of connected IoT devices had reached 46 billion. By the start of the next decade, Juniper expects it to climb to 125 billion devices.

However, unlocking the value of the machine economy is likely to prove challenging. In November 2021, Silicon Valley–based IoTeX launched its MachineFi, which combines IoT devices and decentralized finance to monetize the data derived from the devices. Using decentralized applications, or Dapps, built on IoTeX’s blockchain, the company plans to “democratize” the IoT, enabling consumers to easily monetize their data and earn rewards rather than having their data controlled by Big Tech, like Meta, Google and Microsoft.

“MachineFi ties the machines together and lets them trade information and resources in real time and at a global scale, which is unprecedented,” IoTeX Blockchain and Cryptography Lead Xinxin Fan explains.

IoTeX launched its MachineFi portal, a registration hub for devices such as its logistical tracking device Pebble Tracker, and its blockchain-enabled home-security camera Ucam, in 2021. This year, the company plans to release a decentralized identify framework that will let all IoTeX blockchain-registered machines or smart devices own the data and value they generate.

FRAUD PREVENTION AS A SERVICE: SARDINE

As the world pivoted to digital channels during the pandemic, fraudsters also congregated there. According to Sift’s Q1 2022 Digital Trust & Safety Index, fintechs were among the hardest-hit companies, with payment fraud attack rates for the financial services sector ballooning by 70% in 2021 over the previous year—the highest increase across any vertical in Sift’s network.

With the motto, “Every company will be a fintech company unless fraud kills them first,” Sardine had fintechs in mind when it launched its fraud prevention as a service platform in March 2021. The company designed the platform to detect and identify payment fraud and account takeovers. Describing it as the first such platform “built from the ground up for all digital institutions like cryptocurrency and neobanks,” Sardine maintains that existing antifraud platforms are not readily adaptable to new digital businesses, resulting in low levels of fraud detection and high false-positive rates.

Sardine’s fraud and compliance platform uses a risk-assessment algorithm based on user behavior, biometrics and thousands of data points. The algorithm detects activities like segmented typing, where users toggle between different windows while typing basic information like their name—an indicator of potential fraud. The company also collects phone accelerometer sensor data (to detect whether a phone is moving or stationary), gyroscopic data and network traffic information from users to assess the threat of fraud.

CORPORATE CREDIT CARD: RAMP

Corporate cards have not changed much in decades. Physical cards have become virtual cards to further protect against fraud. But one of the areas still ripe for innovation is corporate card expense management. Keeping track of wasteful corporate card spending, and controlling how employees use their corporate cards can often entail many spreadsheets and inefficient manual processes. Ramp purports to be the only physical or virtual corporate card on the market that can completely block or restrict spending to a specific vendor—for a particular card or across the entire company.

It is not only a card. Ramp’s secret sauce is its expense management software, allowing users to add vendor restrictions for recurring big-ticket expenses dynamically. The software also can automatically collect receipts and categorize expenses. Initially focused on small businesses, it now works with companies of all sizes. It has expanded beyond its corporate card offering to include a buyer service, which uses machine learning to analyze spending data to find ways companies can save money and negotiate better deals so as not to overpay.

|

MOST INNOVATIVE BANKS AND FINTECHS BY REGION |

|---|

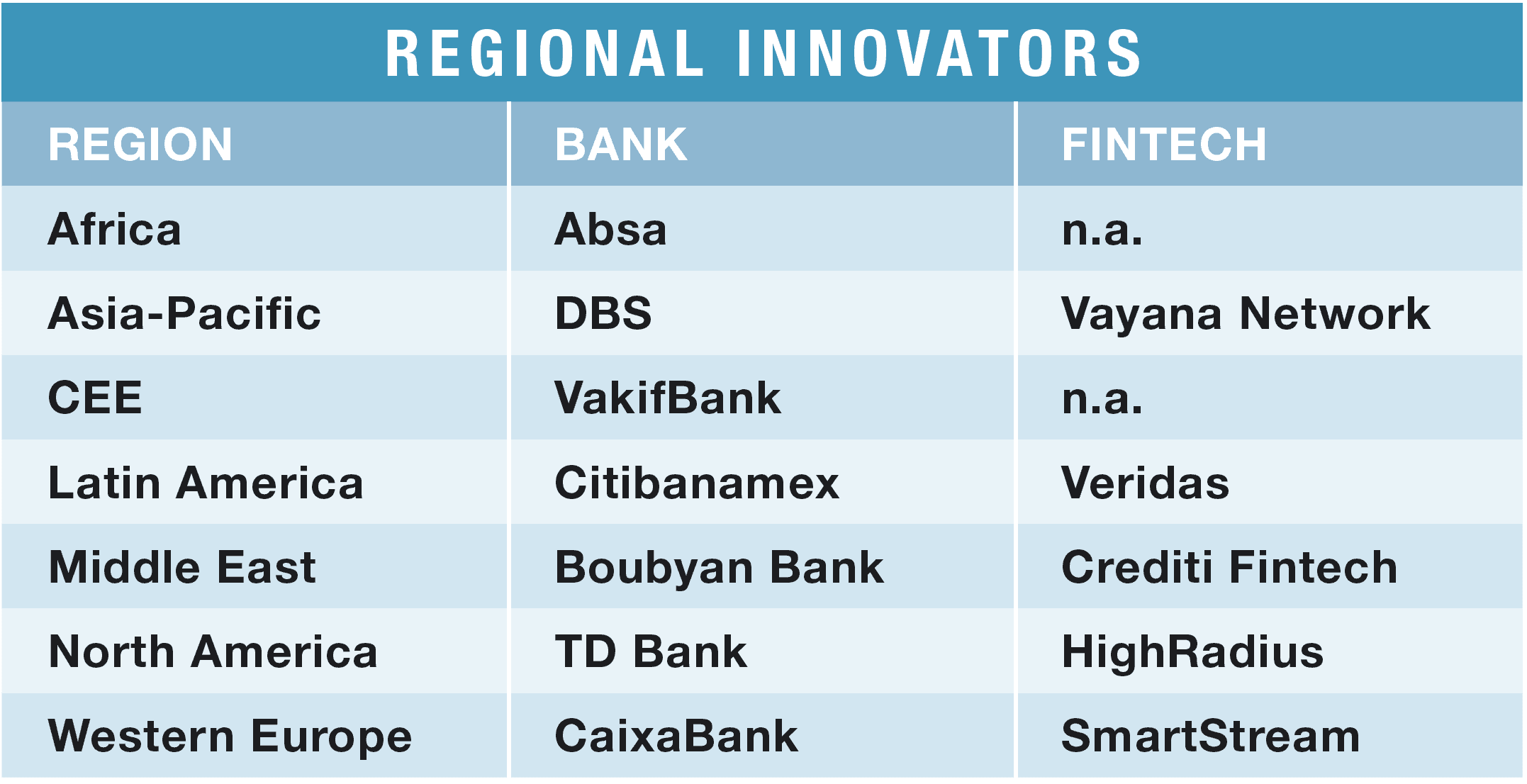

Africa: Most Innovative Bank

ABSA BANK

Absa’s Abby, launched in July 2021, is one of the first-to-market in-app conversational AI virtual assistants (chatbots) in the South African banking sector. The chatbot was built using an AI capability the bank developed in-house, rather than relying on third-party tech, and the bank says Abby supports more advanced use cases than competitors, allowing its customers to interact with its banking app “in a truly conversational manner.” It also purports to be the first African bank to allow new account opening on its website using a “selfie,” which is then checked against government identity databases—something we’re used to seeing from neobanks, but not traditional banks. In fact, all these plays from Absa are indicative of a bank that is striving to embrace being a “digitally led” business in all its interactions with its customers to increase customer engagement, help streamline its business and promote “always-on” digital banking. As the bank says, “With Absa, banking is not boring anymore.”

Asia-Pacific: Most Innovative Bank

DBS

DBS Bank claims innovation in its DNA, and 2021 was no exception. Notable launches included an automated fixed-income execution (FIX) platform, where issuers can directly connect with investors—a first in Asia. Along with JPMorgan Chase and Temasek, DBS was behind Partior, the first live permissioned blockchain-based clearing and settlement platform for commercial bank money. DBS became the first bank in the market to finance bunker fuel-shipment deliveries using a digital bunker delivery note (eBDN); the first bank in Singapore to integrate video analytics with robotics for oversight and customer meet-and-greets at self-service branches 24/7; the first bank in Taiwan to enable customers to link their Economy Stimulus Vouchers to their credit card, using the DBS social media platform; the developer of QR code deposits via ATM; the first end-to-end comprehensive digital solution for credit card applications in Hong Kong; an industry first to offer a seamless straight-through journey from customer onboarding to instant US stock trading. Behind the scenes, DBS launched Client Connect—the first all-in-one, AI- and data-driven customer-relationship management platform to help frontline relationship managers and investment consultants to prioritize their call lists based on data and algorithms.

Asia-Pacific: Most Innovative Fintech

VAYANA NETWORK

India’s largest network for trade financing, Vayana believes that by making trade credit run smoothly, it can ensure that all the different threads of a supply chain remain woven together, “unlocking affordable and easily accessible trade credit for every member of the supply chain.” It makes supply chain financing (SCF) solutions automated, scalable and reliable. Vayana handles integrations and vendor migration to a new financing program, in addition to maintenance and security. It can also take care of everything from bringing SMEs onboard client supply chains to account setup and monitoring, digital authentication of documents, settlement updates and all other elements in the SCF workflow. By leveraging plug-and-play APIs, data analytics and digital technologies it enables companies of any size to participate in SCF programs, seamlessly connecting buyers and sellers. Vayana Network is the first full-stack financing platform for banks and financial institutions in India, enabling the disbursement of around $1 billion every two months.

Central and Eastern Europe: Most Innovative Bank

VAKIFBANK

Turkish VakifBank developed Vinov, the first digital cash-management product in the banking industry that guarantees payments for all customers regardless of their sector. The product is linked to customers across personal, corporate, small and midsize enterprises (SME), commercial and retail lines, and offers payment guarantees through digital channels for all industries for forward or installment payments in Turkish lira. Vinov is a solution that addresses basic problems for companies, like the maturity mismatch between receivables and payments and cash shortages resulting from limited access to liquidity. The VakifBank assurance is an alternative to traditional payment schemes like checks, open accounts, promissory notes, or letters of guarantee. Vinov increases access to liquidity for customers by cross-checking payables and receivables. Since customers can benefit from partial and full discounting functions, suppliers don’t have to discount their receivables, as they can include the required amounts in their cash flows, which limits liquidity problems.

Latin America: Most Innovative Bank

CITIBANAMEX

The World Bank estimates that almost half of Latin America and the Caribbean’s adult population is unbanked—more than 300 million people. Those eye-watering numbers have declined somewhat as more people looked to access financial services online during the pandemic, and due to the concerted efforts of fintechs that have been chipping away at the region’s unbanked population for some time. Citibanamex’s Camelot solution uses machine learning to come up with a more reliable employment-stability indicator for use in credit decisions. According to the bank, it is the first time a machine-learning model has been used to predict employment stability, utilizing both non-traditional (employer) and traditional (customer) and customer data—40,000 variables—to better understand the natural employment cycle in certain industries. This has allowed it to expand credit eligibility to clients with less well-established credit histories by more than 30%.

Latin America: Most Innovative Fintech

VERIDAS

The legacy of the Covid-19 pandemic on banking and how people access financial services in Latin America is still playing out. A good illustration of this is the Biometric Proof of Life for Pensioners solution, developed by facial and voice biometrics specialist Veridas for BBVA Bank in Mexico. Launched last June, the solution means that, for the first time, senior citizens in Mexico can provide “proof of life”—required every six months to collect their monthly pension allowance—without having to physically visit a BBVA branch. Integrated with the bank’s existing systems, the solution allows a person to verify their identity by voice with a three-second telephone call which can be conducted from anywhere. What about the rise of deep fakes? Veridas says its solution features an “anti-spoofing” layer that can detect prerecorded voices and warn of possible identity theft. Veridas says more than 90,000 pensioners have registered for the service, with a success rate of over 99.9%.

Middle East: Most Innovative Bank

BOUBYAN BANK

Boubyan Bank launched several innovative product and process features in 2021, covering its retail app, corporate app and digital assistant, Msa3ed. Boubyan also launched Kuwait’s first SMB Banking App, to help with money collection, salary transfer and vendor transfers. In retail banking, Boubyan expanded PayMe into an ecosystem to facilitate payments among Boubyan users with Face ID, PayMe on Apple Watch and Pay Me Split the Bill. In October 2021, Boubyan launched the Fils Challenge—Kuwait’s first savings challenge. Boubyan also launched Kuwait’s first end-to-end digital onboarding using the government issued PACI ID authentication. Boubyan’s digital-assistant innovations are also becoming available via Apple Business Chat, with the conversion handled by Msa3ed. Boubyan provided Msa3ed with several humanization features covering non-banking information such as travel, vaccination campaign updates, and spending insights. Msa3ed can predict the services that a customer is most likely to use upon login and suggest next best actions.

Middle East: Most Innovative Fintech

CREDITI FINTECH

Crediti Fintech is the mastermind behind the platform and fintech of the UAE Trade Finance Gateway, a national project supported by the Ministry of Economy and led by Etihad Credit Insurance (ECI) to help UAE-based exporters and their international buyers access credit facilities and insurance through a single unified portal. ECI insurance enables exporting SMBs to obtain collateralized loans from participating banks (First Abu Dhabi Bank, Emirates NBD and RAK Bank) leveraging the advanced technology of the Crediti platform, Monimove. Monimove is a blockchain, smart-contract solution that provides the maximum possible prevention of fraud, late payment and unresolvable disputes.

North America: Most Innovative Bank

TD BANK

TD’s consumer-centric strategy leverages a multichannel approach to serve its 26 million customers worldwide. TD is Canada’s leading digital bank and also leads the domestic market for direct Investing. The bank’s innovations have resulted in over 60% of digital adoption, over 90% of self-service financial transactions, and over 2 billion mobile sessions since the beginning of the pandemic in Canada. Recent innovations focus on improving the digital customer experience, particularly for financial wellness and digital inclusion. As part of its innovation strategy, TD operates a testing lab that has produced over 300 proofs of concept and prototypes to date, as well as an AI lab and iD8, which works to implement employee ideas. TD’s UGO accelerates new business models for the bank and new digital developments across business lines by building on innovations at startup speeds.

North America: Most Innovative Fintech

HIGHRADIUS

HighRadius Corporation’s accounting products are the first of their kind to use AI to improve treasury by creating efficiencies and streamlining processes. The ultimate result for clients is more liquidity on the balance sheet. Autonomous Accounting puts the process of identifying anomalies and missing transactions on autopilot, leveraging AI to continuously evaluate transactions and flag those needing review on a daily basis. Autonomous Receivables connects the end-to-end order-to-cash cycle across multiple functions into a single business process, leveraging $2.3 trillion of financial transaction data to predict which invoices will be paid. As a result, companies have improved net recovery rates, can manage coming orders and are able to fast track past-due recoveries. HighRadius’ AI-based cash forecasting helps treasurers realize accurate, real-time cash forecasting without manually collecting data across various systems and spreadsheets. By automating this function and incorporating statistical modeling to drive more accurate forecasts, treasurers improve their working capital and make better decisions regarding daily funding and investments.

Western Europe: Most Innovative Bank

CAIXABANK

CaixaBank has been a leader with some of the first financial apps and services in Spain that give customers the ability to transact digitally. With a focus on customer-centered innovation, the bank has incorporated new technologies into its offerings. Customers can access a portfolio of services through the CaxiaBankNow mobile app, which currently has 8.21 million active users logging in almost daily, on average. These services include ATM withdrawal using facial recognition rather than a PIN, a range of nonfinancial services, and an omnichannel voice bot that customers can tap for assistance at any time of the day. This app gives customers better control of their finances with a dashboard and direct access to their favorite transactions, and they can easily use their phone for mobile payments through the app. Noa, an AI-based chatbot, helps guide users through the bank’s electronic channels and can “discuss” a customer’s personal finances. Enhanced security allows users to manage the devices that they’ve enrolled to access the bank’s application to include foldable devices. Users can also communicate with their adviser via WhatsApp.

Along with financial services, CaixaBank’s Wivai e-commerce offers customers a catalog of products, while Smart Buy provides valuations to help promote the circular economy and reduce technology waste.

Western Europe: Most Innovative Fintech

SMARTSTREAM

SmartStream’s Affinity and Air products make a cloud-native data comparison tool that matches rates faster than other products on the market. Affinity was developed via SmartStream’s Innovation Lab to meet the technical and agility demands for operational data management and data quality processes. It automatically learns how records correlate and mimics a user’s actions to reduce the time traditional data verification process to seconds. Air is a cloud-native AI data reconciliations solution, and Affinity works with Air to ensure that the algorithm adopts any manual changes to the matched data. Air now has enhanced exceptions management capabilities and attribute-by-attribute matching. The platform supports limitless datatypes that support reporting requirements under MIFID II and MiFIR regulations. SmartStream’s Reference Data Utility (RDU) is able to source, validate, and cross-reference data required for financial institutions electronic trading, analysis, automation of operations, and regulatory reporting. RDU recently launched the Exchange Notification Service (ENS) that presents a view of exchange notifications from derivatives exchanges that are used to manage derivatives reference data.