Steady revenue streams make transaction banking attractive during times of volatility. But tech and upstart competitors are remaking the business.

Global transaction banking provides what you might call the “plumbing” of international business. It ensures that salaries get paid, money for goods and services gets delivered, investment returns are credited where they belong, and the wheels of world trade keep turning. But despite its links with the real economy, transaction banking has historically commanded less attention from C-suite executives than investment banking, which delivers richer, more volatile revenue streams. That changed during the financial crisis, when investment banking revenues went south—and they have yet to return to their pre-crisis levels. Major global banks found respite in the steady, predictable income that transaction banking provided.

Now, global transaction banking (or GTS, as some banks call it, for global transaction services) is a more clearly delineated division within global corporate and institutional banks, and senior executives view it more strategically. “GTS was out of vogue for most of the 2000s, but it has now returned to favor with commercial banks,” notes Dominic Broom, head of treasury services, Europe, Middle East and Africa, at BNY Mellon. “GTS represents the core of most companies’ banking needs, and compared with other aspects of banking, the capital requirements are relatively favorable; hence its return to fashion.”

Not only is GTB in vogue, but confluent factors are contributing to one of the biggest shake-ups the transaction banking industry has seen for decades. These forces include nonbank tech disruptors like bitcoin and the blockchain, the eastward shift in global economic power, low-interest earnings in developed markets, the emergence of so-called challenger banks, and regulatory pressure to reduce risk and inefficiency in payment-clearing infrastructure. A clear geographical divide has opened up between banks that started investing seriously in GTB only after 2009 and are still growing the business, and the better-established transaction banks in developed markets that are now consolidating and cutting costs, largely driven by regulatory changes following the financial crisis.

FILLING A VACUUM

Not so long ago, analysts were predicting that the transaction banking business would be concentrated in the hands of a few global players. But now some of the global giants are reviewing where they want to play, says Andrew England, a director at financial technology provider Intellect Design Arena, UK, and head of strategy for iGTB, its GTB division. That allows challenger banks to rush into the transaction-banking vacuum the big banks leave behind.

England, former head of GTB for Central and Eastern Europe at Italian bank UniCredit, says global banks are casting a cold eye on their market positions. If they are not among the top three banks in a given market, they either withdraw or retrench, he says. The most extreme example is Royal Bank of Scotland, which in early 2015 announced it would reduce its global footprint from 38 to 13 countries. Other global banks, including HSBC and Deutsche Bank, have scaled back their activities in certain markets in an effort to deliver higher shareholder returns, squeezed by a low-interest-rate environment, regulatory changes and cost-cutting pressures.

Digitization … has become strategic for the corporates, and they expect a lot more from their banks.

Elliott Limb, Misys

The upstarts taking advantage of such retreats are domestic or regional players that have poached GTS talent from larger rivals. One such challenger is DBS Bank in Singapore. DBS began investing in transaction banking just six years ago but is already giving the global giants a run for their money in Asia, having successfully leveraged its regional franchise and investment in digital services to meet growing demand for intra-Asia transaction banking.

John Laurens, head of GTS at DBS Bank, says the bank has benefited from the trend among corporate treasurers to diversify their portfolio of transaction banks. The shift in global economic activity from West to East has helped too. “Corporate boards are looking strategically at their banking group looks to ensure it aligns with their economic activity around the world—particularly in Asia, given its growth dynamic,” says Laurens. “That plays to DBS’s strengths and our focus on delivering Asia to corporates globally.”

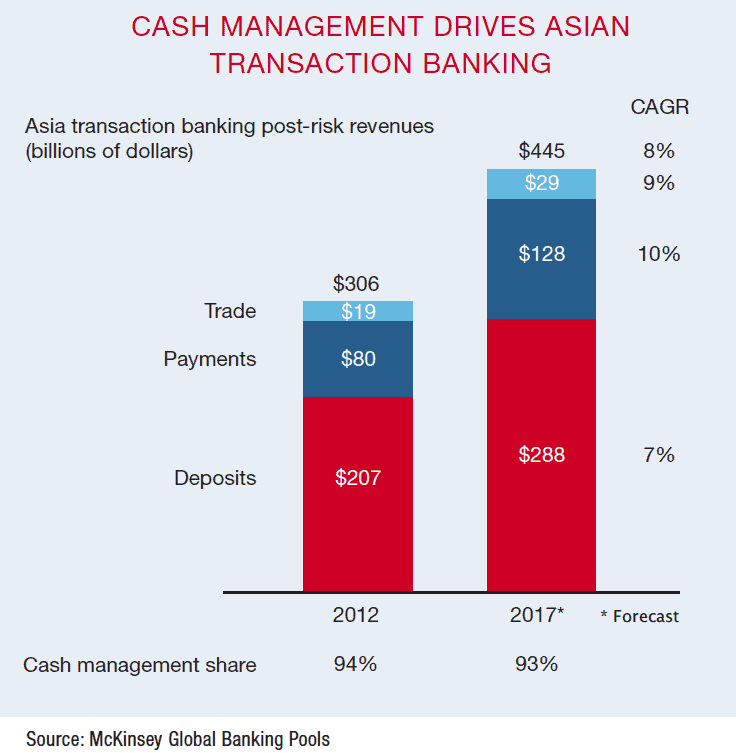

The renminbi’s growing internationalization means Chinese companies with “redbacks” in their pockets are looking to invest them globally, including on acquisitions. “We’re well placed to benefit from that trend,” says Laurens, “being headquartered in Singapore and with extensive experience supporting Chinese companies.” Meanwhile, an increase in intra-Asian trade is also benefiting DBS, he says, particularly in the open-account trade space and supply chain finance—the fastest-growing part of its transaction banking business. Indeed, according to McKinsey, Asia is the world’s largest transaction banking market, representing 53% of the global opportunity, with total revenues in the region predicted to reach $578 billion by 2017. And research firm Greenwich Associates estimates that foreign banks’ share of domestic cash management in Asia fell from 75% in 2005 to 60% in 2012.

ASIAN INNOVATION

Asia is not only the largest and fastest-growing trade area, says Elliott Limb, global head of transaction banking at financial software provider Misys. It is also becoming the innovation driver. “This makes sense,” he says, “if you think about the fact that, as well as net exporters the rising mass affluent are also becoming net importers in some areas.” Limb explains that as intra-Asian trade flows swell, it’s in the regional banks’ best interests to make transaction processes as simple and effective as possible. Their motivation to innovate “could be a very exciting development,” he says.

In traditional trade finance, various initiatives over the years have sought to address inefficiencies in processes around letters of credit and other trade documentation. However, many of these processes remain manual and paper-intensive. But DBS Bank believes it may have the answer in the form of the blockchain, or distributed ledger technologies.

Tech experts originally devised the blockchain as a “permissionless, distributed database” for digital currencies like bitcoin, which do not require financial intermediation by a bank. Bitcoin directly challenges banks’ dominance of payments, but banks are focusing their energies on the blockchain’s potential to provide a “single source of the truth,” as fintech mavens say. DBS believes blockchain could be used to avoid duplication of funding in trade finance and to “dematerialize,” or automate, trade documents. “We’re looking at linking physical [trade] documents with blockchain tokens, which could transform traditional trade operations and drive efficiencies for corporates and banks,” explains Laurens.

Such technological advances, plus competition from challenger banks, are forcing global transaction banks to confront issues that some have avoided for centuries, says Limb. “Digitization is no longer optional,” he says. “It has become strategic for the corporates, and they expect a lot more from their banks.”

Laurens says DBS can be nimbler in leveraging new technologies like blockchain because it has less legacy IT to maintain than some global banks, is less constrained by risk and regulation, and is imbued with a culture of innovation. “DBS’s investment dollars are focused on customers and embracing digital, which was an absolutely refreshing experience,” says Laurens, who prior to joining DBS in 2014 was HSBC’s Asia-Pacific head of global payments and cash management.

Broom of BNY Mellon says the days when transaction banks could develop their own infrastructure and manage every step of a transaction process are gone. He says banks need to partner with carefully vetted third parties—either with other banks, including those with the international networks that could bridge gaps in coverage, or with third-party providers. Cloud technologies will also be important, says Broom, enabling banks to overcome legacy IT constraints by more readily updating core banking platforms and hosting value-adding applications from third-party providers.

Another change agent in GTB is the move toward real-time payments. The UK’s Faster Payments Service was the first to introduce same-day settlement for low-value payments, but similar platforms are being established in Australia, Singapore and India. Such developments are being driven by regulators looking to reduce risk and inefficiencies in payments. As a side effect, immediate-value payment systems will put pressure on transaction banks to deliver enhanced reporting around payment status and delivery. Limb says the global drive toward real-time payments is particularly noteworthy in markets like the US where payment systems haven’t changed for decades.

One region leading innovation in payments is Africa. Under a program approved in 2010, the South African Development Community’s Integrated Regional Electronic Settlement System has already implemented real-time electronic payments and cross-border standardization for nine of SADC’s 15 member countries: South Africa, Namibia, Lesotho, Swaziland, Malawi, Tanzania, Zimbabwe, Mauritius and Zambia. Limb believes the SADC initiative “will probably wake us all up to the speed that we need to do things at.”

But all the talk of transformational digital technologies like the blockchain and real-time payment systems is somewhat misleading. While some transaction banks are eagerly embracing digital technologies to transform inefficient processes and reinvigorate the customer-facing front-end, other banks are still grappling with providing sufficient levels of straight-through processing for payments and the level of transaction reporting that corporate customers require to reconcile payments and gain control and visibility over their cash.

The “customer-centric nirvana that the corporates need is not so easily implemented in the banks,” says Limb. That’s because it’s not just about improving technology but also about changing the culture and processes within banks, which takes time. So will transaction banking look radically different five years from now? “I don’t think so,” says Broom. He believes that, despite the emergence of digital currencies like bitcoin, fiat currencies will remain the primary means by which value is settled for many years to come. Still, streamlining and transparency will keep improving. “The units of value exchange will remain the same,” Broom predicts, “but technology will continue to evolve to help companies and their banks implement more-efficient processes that offer richer management information at a lower cost.”