Digitalization investments spur growth.

Europe’s banks showed strong resilience through the ongoing pandemic, pushing forward for a second year with efforts to serve retail customers and corporate clients who were coping with a range of obstacles thrown up by Covid.

Clients of all kinds became more demanding as greater implementation of digital innovations revealed vast new possibilities. Environmental, social and governance issues also continued to garner attention from corporate and institutional clients as scientific warnings grew increasingly dire. The past year saw some banking-sector merger and acquisition activity as banks sorted out strategic priorities, including the mega-merger of CaixaBank and Bankia.

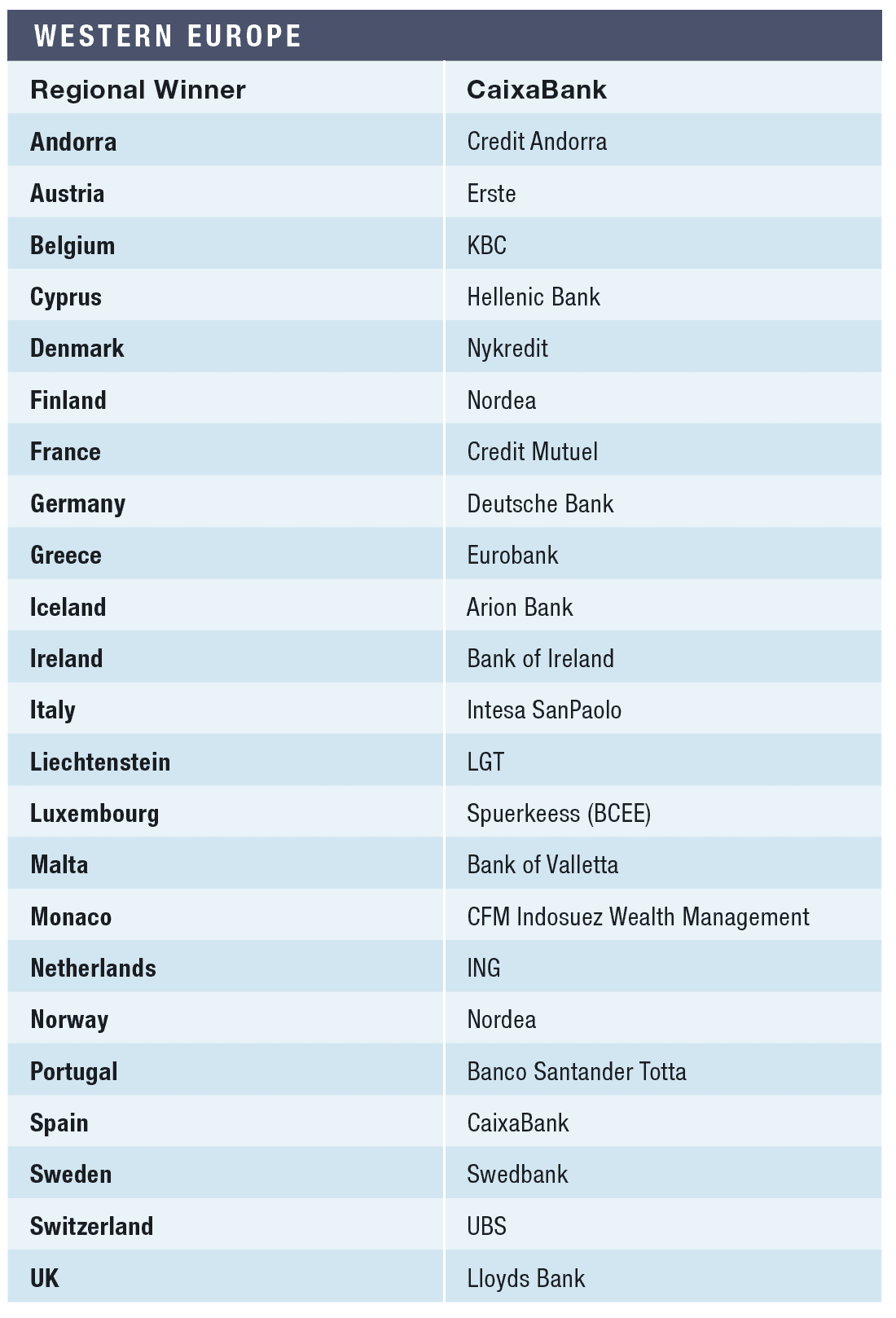

In part as a result of the Bankia merger, CaixaBank Group today serves 21 million customers through more than 5,300 branches in Spain and Portugal and exceeds €680 billion ($736 billion) in assets. Our overall winner for Western Europe, Caixa, also retains pole position as Best Bank in Spain, after a year of strong performance right across the board—from business restructuring to digital innovation.

“We successfully completed the integration of CaixaBank and Bankia while at the same time concluding a very positive year, especially in the management of long-term savings,” said CEO Gonzalo Gortázar, at the time.

Core revenues came to €11.34 billion and pro forma recurring profit for the year was €2.42 billion. Fee and commission income climbed to €4 billion, up 6.7%. CaixaBank ended 2021 with a long-term savings market share of 29.4% and assets under management total of 48.2% in the year, of which 16.5% was organic growth. The Common Equity Tier 1 (CET1) capital ratio rose to 13.2%, well over the goal of 11%-11.5%.

Caixa continues to strengthen in digital banking, with the proportion of digital customers rising to 73.1%. In March, the bank announced a landmark partnership with BNP Paribas 3-Step IT, giving its professional clients access to innovative and sustainable IT solutions for the first time. Rated one of the world’s most sustainable banking groups, in 2021, CaixaBank became one of the founding members of the Net Zero Banking Alliance.

In neighboring Portugal, the winner Santander reached a million digital customers, increasing 7.5% compared with 2020. Sales through digital channels represented 56% of the total, up 13% over the previous year. Deposits increased by 7%, off-balance sheet resources grew by 17%, and the bank held onto market shares in mortgages and new corporate loans for nearly a quarter. Total income increased by 3%, costs were down 5%, and underlying attributable profit leapt by 42% over the previous year.

“These figures reflect the transformation that has been carried out, both at an operational and commercial level, with a focus on simplifying processes and technology, oriented towards improving our customers’ experience and satisfaction, within a new, more competitive, more digital context, and with increasingly demanding customers,” says CEO Pedro Castro e Almeida.

In Austria, winner Erste Bank more than doubled its profits, mainly due to sharply reduced risk costs. Operating income increased by 8.2%, with net fee and commission income up 16.5%, while risk costs were reduced from €1.3 billion in 2020 to €159 million. As a result, net profits for the year were €1.92 billion, compared to €783 million in 2020. Customer deposits were up 10.2% across core markets, most strongly in Austria and the Czech Republic. With war sanctions impacting other Austrian banks, Erste stated that ‘it has no direct operating subsidiaries in Russia or Ukraine and our direct exposure to these countries is negligible.”

The winner in Germany, Deutsche Bank, put in exceptional performance with core banking profits up by 48% to €4.8 billion before taxes. CEO Christian Sewing said: “In 2021, we increased our net profit fourfold and delivered our best result in ten years while putting almost all our expected transformation costs behind us. In addition, all four core businesses performed at or ahead of our plan, and our reduction of legacy assets progressed faster than expected.”

Overall, revenue rose 6% to €25.4 billion. This increase in profitability ran across the business at the corporate bank, where profits were up 86%, while asset management nearly doubled its contribution. Deutsche Bank also reduced its leverage exposure from €72 billion in 2020 to €39 billion. Risk-weighted assets came down sharply and provisions for credit losses were 71% lower. The bank’s CET1 capital ratio stood at 13.2% at the year end.

Italy’s largest lender and our repeat winner, Intesa SanPaolo, has more than 20 million customers, nearly 100,000 employees, and over 4,700 branches. It takes pride in its role as a growth accelerator for the Italian economy and its growing ESG and climate initiative. Financially, the bank had a particularly good end to 2021, with €1.7 billion of its total pre-tax profit of €2.2 billion coming in the last quarter. Net income for the year was up nearly 20% on a substantial increase in fee and commission income. Operating margins improved, as did credit quality, with over a quarter of gross NPLs removed by the year-end. The bank has strong liquidity and a solid capital position, reporting a fully-loaded CET1 ratio of 12.9%.

Intesa’s profits and capital buffers may come under strain in 2022 due to its considerable exposure (estimated at €5.7 billion) to Russia and Ukraine, which in a worst-case scenario could knock 1.4 percentage points off its core capital. Though the direct impacts are likely to be less than at its main rival UniCredit, the knock-on effects on Italy’s economy of a prolonged war and financial sanctions would further undermine credit quality and profitability.

Our Best Bank in France is Crédit Mutuel, whose strong financials underpin an equally strong commitment to the values of mutualism and staying close to its customers on a regional basis. Overall income rose by nearly 13% to €16 billion. More tellingly, this was an 8.7% increase over pre-pandemic levels. Profitability rose even faster, by 39% year-on-year or 11% compared to 2019. The bank increased its lending across the board with a 9% boost to mortgages and a 6.4% rise in consumer loans, while income from its insurance activities and specialized business lines grew by nearly a third. With a CET1 ratio of 18.8%, Crédit Mutuel is among the best capitalized financial institutions in France

Crédit Mutuel’s digital transformation gathered momentum, partly in response to the pandemic. The app using the bank’s video service, launched in 2020, recorded a sixfold increase, and nearly 12 million electronic signatures were completed, 73% more than during the first year of Covid-19. As chairman Nicolas Téry notes: “The Covid-19 crisis and its digital, environmental and social impacts have transformed us. We have mobilized our forces around the principle of mutualism in evidence. The 2021 results reflect these changes.”

KBC, the winner in Belgium, saw group net profit up by 81% to €2.6 billion, of which nearly €2 billion was generated by the bank’s domestic market, where profitability nearly doubled over the previous year. Given the low net interest margins prevalent in Benelux countries, KBC could pull ahead of its competitors, thanks to the richer mix of fee and commission income built into its bancassurance model.

Group revenues rose by 5%, with net fee and commission income up by 14%, driven primarily by an increase in fees for fast-growing insurance and asset management services. At year end, total assets under management amounted to €236 billion, up by 12% over 2020. Management kept a lid on costs and the capital base remains robust, with a fully loaded common equity ratio of 15.5%.

The winner in the Netherlands, ING, put in another strong performance with profit before tax up by 78% and full-year return on equity (ROE) rising to 9.2% on the back of higher fees and commissions and a substantial reduction in provisions against bad loans. The bank’s CET1 ratio strengthened to 15.9%, reflecting improved risk management and adequate capital buffers.

“Looking back on 2021, I’m pleased with our performance,” says ING CEO Steven van Rijswijk. “I’m encouraged by increased lending volumes and strong fee income growth in the final quarter of 2021, a sign of growing confidence in the economy as the world seeks ways to live with the coronavirus. … I’m particularly satisfied with the consistent growth we’ve recorded in our diversifying sources of income.”

ING was a front runner in the race to digitalize, and now some 51% of its customers are mobile-only. The bank is investing in a seamless digital customer experience and a crucial component of its scalable technology is the ING Private Cloud (IPC).

The Best Bank in Luxembourg is Spuerkeess, the largest lender in the Grand Duchy, actively diversifying its financing sources by issuing securities mainly intended for institutional investors. Over the first half of 2021, this type of funding increased by 35%, reflecting the appeal of a strongly capitalized bank with a CET1 ratio rising above 22%–well ahead of most competitors. The bank is expanding its lending, particularly to retail and corporate projects, and growth in customer deposits remains strong. Lower cost of risk and reversals of provisions made at the outset of the pandemic contributed to a 50%-plus boost to profitability over the previous year.

In Iceland, winner Arion Bank ended 2021 with its core income up 14.8%, while ROE rose to 13.4% on a solid operating performance. Customer loans grew by 13.8%, deposits from customers increased by 15.3% and total assets were 12.0% larger. CEO Benedikt Gíslason noted: “It was a record year in mortgage lending, with 211 billion Icelandic kronas [$1.6 billion] in mortgages, and the bank’s mortgage portfolio grew by 85 billion kronas over the year. Assets under management increased by almost 20% to 1.35 trillion kronas at year-end.” The bank’s CET1 ratio rose to 19.6% at year end, with strong liquidity maintained after dividend payment and share buybacks amounting to 31.5 billion kronas.

The Best Bank in Sweden this year, Swedbank, saw fee and commission income rose by 16% to record levels. Growth in mortgage volumes was sustained and the bank built on its market-leading position for new mortgage sales. Jens Henriksson, president and CEO, highlighted the bank’s substantial capital and liquidity position. “Swedbank stands strong in an uncertain time … The ROE was 13.2% for the full year of 2021. Our target of a 15% return remains unchanged regardless of the bank tax. Before the end of the year, we will present a plan to reach the target.” The bank’s CET1 ratio at year end was 18.3%.

Our winner for Norway and Finland, Nordea, “wants to become the leading relationship bank in the Nordics,” says their head of Personal Banking, Sara Mella. Nordea President and Group CEO Frank Vang-Jensen declared himself “happy with our progress,” reflecting on a milestone year in which the bank surpassed its financial targets for 2022 ahead of schedule. Operating profit was up 67% to €4.9 billion and ROE reached 11.2%, well above target.

Total income from personal banking grew by 9%, driven by solid mortgage activity. Finland was the star performer across the pan-Nordic bank, with an 8% increase in mortgages, improved net interest margins, and a 14% boost to fee and commission income, lifting total income by 14%.

Tighter lending margins in Norway more than offset higher mortgage volumes and a 23% rise in fees and commission, driven by higher savings and investment income. Group business banking income grew by 15%, with lending volumes up 6% on strong growth in Norway and Sweden. Assets under management grew by 17%, reaching an all-time high.

In a joint message from Danish winner Nykredit, Chair Merete Eldrup and Michael Rasmussen Group Chief Executive announced: “Despite the constant change again in 2021, Nykredit maintained its position of strength. The financial results announced today exceed our expectations and are the Nykredit Group’s best.”

The year saw strong business and customer growth at Nykredit Bank, resulting in a business profit of 5.3 billion Danish krones ($770 million) in 2021 (2020: DKK3.3 billion). Assets under management grew by 39% at newly acquired Sparinvest, now part of Nykredit Wealth Management. Specialist subsidiary Totalkredit increased its lending in 97 out of 98 Danish municipalities and a wave of new green investments was announced. At year end, Group CET1 ratio was 20.6%.

Switzerland’s largest bank, UBS, remains the Best Bank, having had a strong performance in 2021. Group profit leaped to $7.5 billion with sharp improvements across all divisions, and while costs remain an issue, the cost/income ratio of 73.6% came in under target. UBS flagship Global Wealth Management raised its profitability by 19% and contributed $4.8 billion pre-tax. The Swiss bank increased operating income by 13% to $481 million on a 5% growth in fee-generating assets but higher costs, including an $85 million increase in litigation provisions against historical involvement in tax evasion for French clients.

CEO Ralph Hamers says: “We now manage $4.6 trillion in assets and during 2021, assets invested in sustainability-focus and impact strategies across the firm increased 78%,” adding that “We’re adapting our coverage model to deliver more digital and scalable advice as well as bespoke solutions, and we’re accelerating our technology investments while maintaining strong cost discipline.” The CET1 ratio strengthened to 15% at the year end.

Some forty different banks are within a 10-minute walk of Monte Carlo’s celebrated casino. They are practically the only branch of an international group in the country and catering exclusively to ultrarich tax exiles. Our repeat winner as Best Bank in Monaco, CFM Indosuez Wealth Management, is different. The principality’s leading bank’s roots go back a century, to 1922, when it was created by prominent Monegasque families, some of whom still hold a minority stake in the bank. It maintains five branches and serves all types of clients, from private individuals and businesses to institutional clients. It is majority-owned by Crédit Agricole and its main business is providing bespoke services to international clients. Still, it is also a mini-universal bank with the region’s largest dealing room. Green investment offerings support its partnership with the Oceanographic Institute of Monaco.

Liechtenstein’s banking system is similarly devoted to servicing a wealthy international clientele, and our repeat winner, LGT, expanded its global reach through the acquisition of UBS’s wealth management business in Austria last July, to be followed this year by Crestone Wealth Management, Australia’s grew leading service provider for HNWIs, to provide coverage of the Indo-Pacific region. LGT produced strong results, with operating income up by 16% and net profits of 353 million Swiss francs ($369 million), representing a 21% increase over 2020. Assets under management grew by 19%, with net inflows of 24.8 billion francs. Having established a range of sustainable solutions for its clients, LGT launched its first impact fund.

The winner in Andorra is Credit Andorra, which on top of strong organic growth, reinforced its leading position through the acquisition of smaller local lender Valls Bank. CEO Xavier Cornella says: “[This] is a strategic operation that reinforces our growth plan and that is intended to consolidate our leadership position in Andorra and strengthen our long-term commitment to the economic and social progress of the country.” Following the acquisition and alongside the integration of GBS Finanzas Investcapital A.V. in Spain, Credit Andorra Group’s business volume amounts to €23 billion, well above the forecasts of the bank’s strategic plan.

Malta’s largest lender, Bank of Valletta, has come out of a sticky period of being hacked by cybercriminals, abrupt changes in management and major litigation that is still unresolved to produce a sparkling set of figures for 2021. Profits rose fivefold to €81 million on stronger commission and net interest income. Costs remain an issue, increasing by 15%, though this includes a hefty increase in strategy costs, disbursements for card fraud and regulatory fines. The bank embarked on a digital transformation process and is upgrading branches accordingly. However, the directors recommend no final dividend be paid–possibly due to an Italian court’s judgment against Bank of Valletta requiring it to pay €363 million to bondholders of a failed ship-owner that BOV backed. The bank is appealing the outcome.

After a difficult financial decade for Greece, winner Eurobank led the way in restructuring bad loans and, in 2021, reduced its NPL ratio to 6.8%. Core operating profit was up 64.9% to €482 million, new loan disbursements increased by €7.8 billion, and customer deposits increased by €5.9 billion. The bank’s CET1 ratio rose by 60 base points year on year to 14.5%

CEO Fokion Karavias says: “As Greece exits a decade of deleveraging, the economic recovery will be investment-driven, and banks have a crucial role. We believe we are in a pole position to capitalize on this growth cycle. Our profitability will be based on loan growth, our leading position in fee businesses, cost containment, with a shift from ‘run the bank’ to ‘grow the bank’ and investments both in people and systems to leverage data and digital tools.”

In December, Eurobank announced that, as part of its strategy to expand its international presence, it had completed the acquisition of 12.6% of Hellenic Bank, Cyprus’ second-largest lender and this year’s Best Bank in Cyprus. Hellenic worked hard to improve the quality of its portfolio, with NPLs now at 14.5% after a program of resolution and deleveraging. Profit to end September was €21 million.

Hellenic is currently acquiring a performing loan portfolio worth €556 million from RCB Bank, subject to compliance with international sanctions. CEO Oliver Gatzke comments: “In line with the bank’s strategy of growing its business in Cyprus, the transaction increases the bank’s client base in business lending, provides cross-selling opportunities, improves its operating income through higher interest income and creates the potential for growing its non-interest income.” The bank’s CET1 ratio was 20% in the third quarter.

Bank of Ireland rebounded strongly in 2021, delivering €1.4 billion in underlying pre-tax profit on 12% income growth and a successful cost reduction program stripping out €1.65 billion of operating expenses. Asset quality improved, with NPE down to 5.5%. The bank boasts a solid capital position, with a CET1 ratio of 17.0%. As CEO Francesca McDonagh comments: “We grew income, reduced costs for the eighth consecutive reporting period and significantly increased capital ahead of the anticipated completion of two transformational acquisitions of Davy and KBC Ireland’s portfolios.” The bank achieved an adjusted ROTE of 12.7% last year.

Our Best Bank in the United Kingdom is Lloyds, whose focus on domestic individuals and business clients served it well in 2021. Net profit increased fourfold to nearly £5.9 billion ($7.6 billion) on a 9% increase in net income due to higher lending volumes and improved margins. A hefty reduction in impairment charges generated a net underlying impairment credit of £1.2 billion.

A disciplined approach kept the lid on costs, with operating expenses rising just 1% overall. Strong savings demand and investment performance in insurance and wealth management produced a £7 billion boost to new open book assets under administration. A long time leader in banking IT, Lloyds continued to enhance its digital capabilities with mobile app releases that nearly doubled the previous year’s usage and led to a three-fold increase in corporate clients onboarded to the new cash management and payments platform. The bank’s CET1 ratio was 17.1% at the year end.