Despite the geopolitical and economic challenges of the past year, banks worldwide persevered.

Most of the world’s leading banks successfully navigated the geopolitical and economic challenges of 2022. These included Russia’s invasion of Ukraine and the resulting international sanctions, spikes in energy and food prices, the negative impacts of a strengthening US dollar on emerging economies, and inflationary pressures that prompted central banks to push through a rapid series of interest rate hikes.

Initially, banks benefited from higher base rates, increasing their margins and generating higher income. As they also continued to tamp down on costs, largely thanks to enhanced efficiencies that come with the digital transformation of internal processes and client relationships, their profitability rose sharply. Indeed, many of our winning banks reported record financial results for last year and rewarded investors with share buybacks and higher dividend payments.

They also invested in a sustainable future. Within their businesses, they did so mainly by accelerating the drive toward further digitalization of processes, products and services and by applying cutting-edge technologies that include artificial intelligence and quantum computing where appropriate. Similarly, more banks have been migrating their internal processes from legacy on-site to cloud-based facilities.

But many leading banks also increased their efforts to achieve a more sustainable future for society and the planet. During 2022, they increased the choice and scale of their sustainable offerings to investors while at the same time moving more rapidly toward aligning their portfolios with globally recognized environmental, social and governance sustainability goals.

Meanwhile, most leading banks continued to strengthen their capital buffers. Credit quality improved; the proportion of nonperforming loans declined; and liquidity and capital ratios were, as a rule, strengthened. However, recent turmoil in a few specific corners of the industry prompted bank runs and raised broader questions about the role and viability of global banking.

Financial regulators and central banks acted promptly to stem the panic, extending guarantees to non-insured depositors, opening liquidity windows and forcing bank mergers through at breakneck speed. However, these methods have raised questions about the moral hazard and the accepted order of seniority of bond and equity holders. More important, all this has prompted questions over whether regulators will impose stricter and more-widespread stress testing on banks along with higher capital and liquidity requirements. Also, the banking industry’s mutual insurance schemes will likely be reinforced to protect vulnerable banks and their depositors.

All of this has a cost. The return to historically standard interest rates has boosted income and profitability for most banks. But from here on, regulatory or prudential requirements mean banks are likely to rein in lending, thereby putting a brake on economic activity. This credit-tightening cycle puts greater pressure on customers and feeds through to poorer asset quality and higher cost of risk. Lower business volumes, combined with higher provisions and capital costs, will almost certainly prove a serious brake on banks’ profitability in the immediate future. As a result, few bankers expect 2023 to be another vintage year.

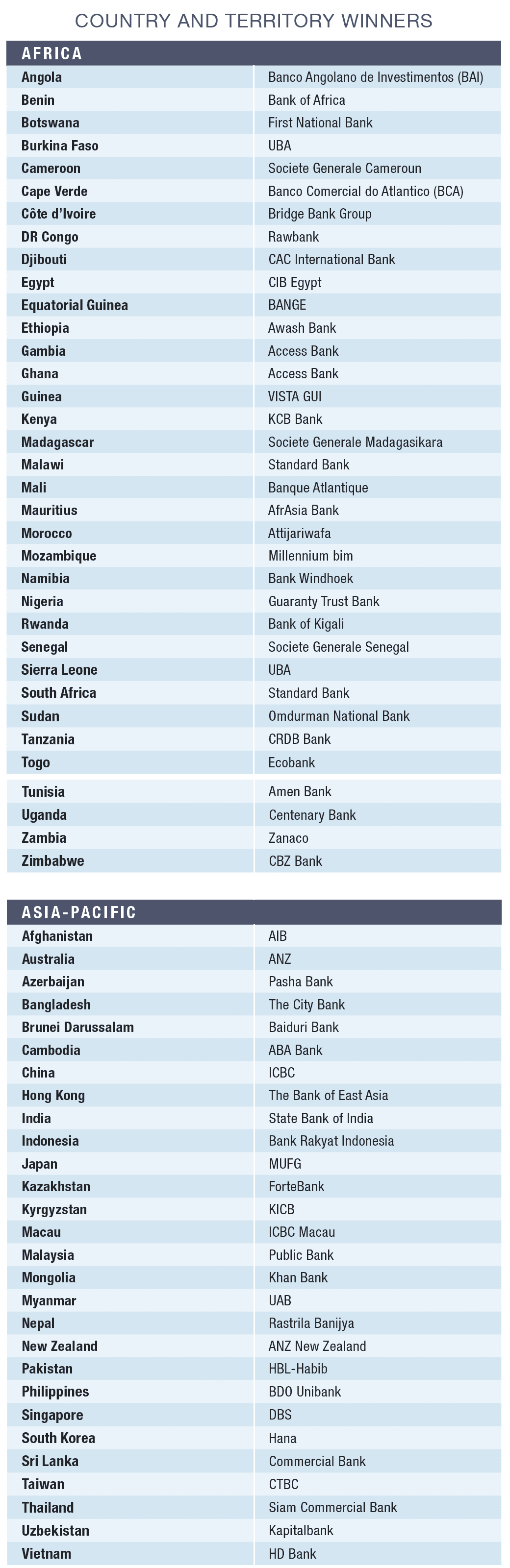

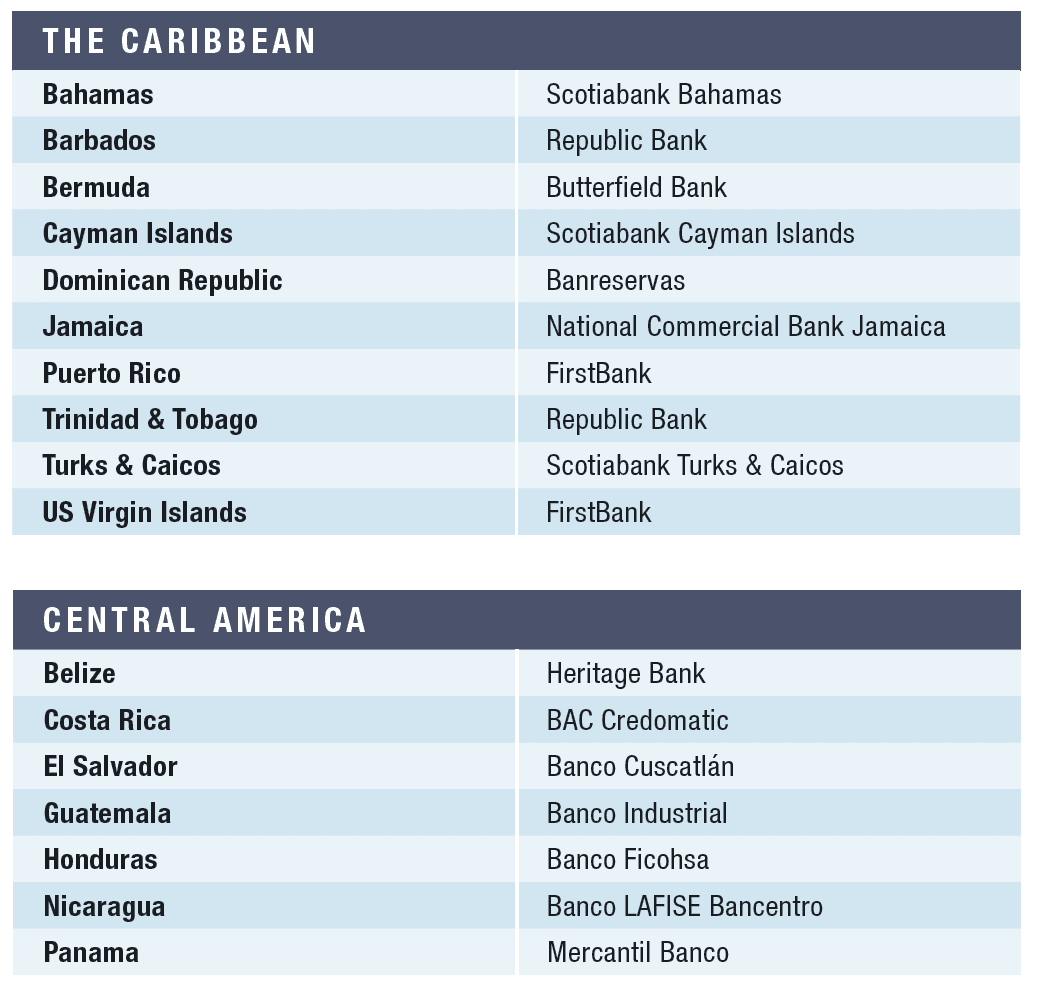

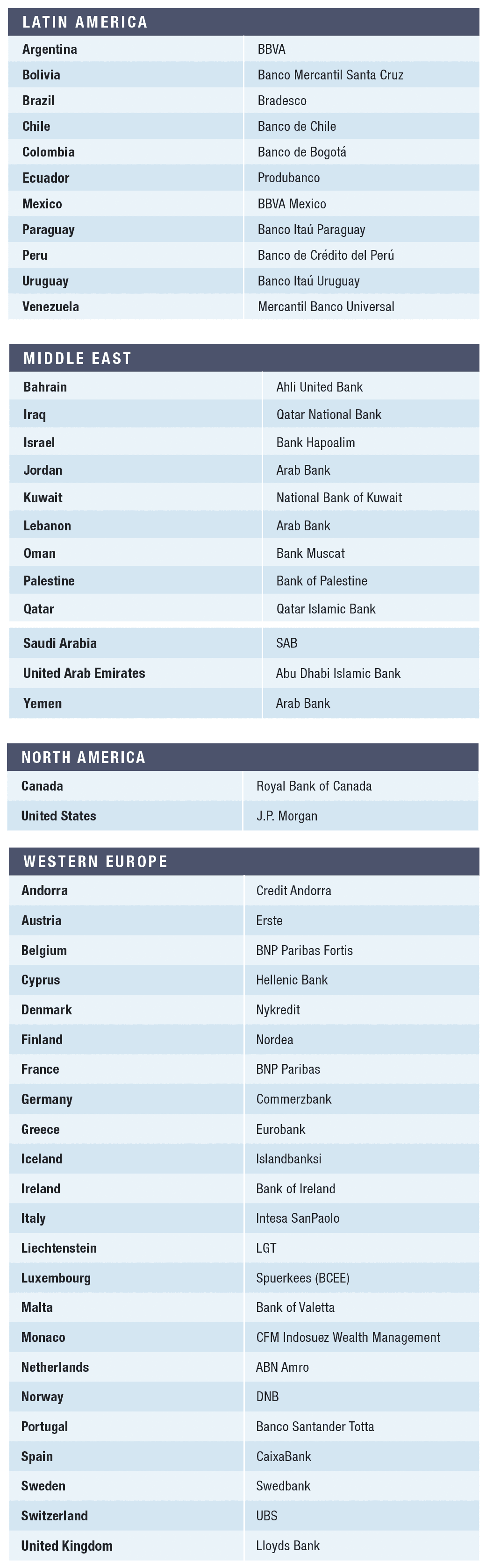

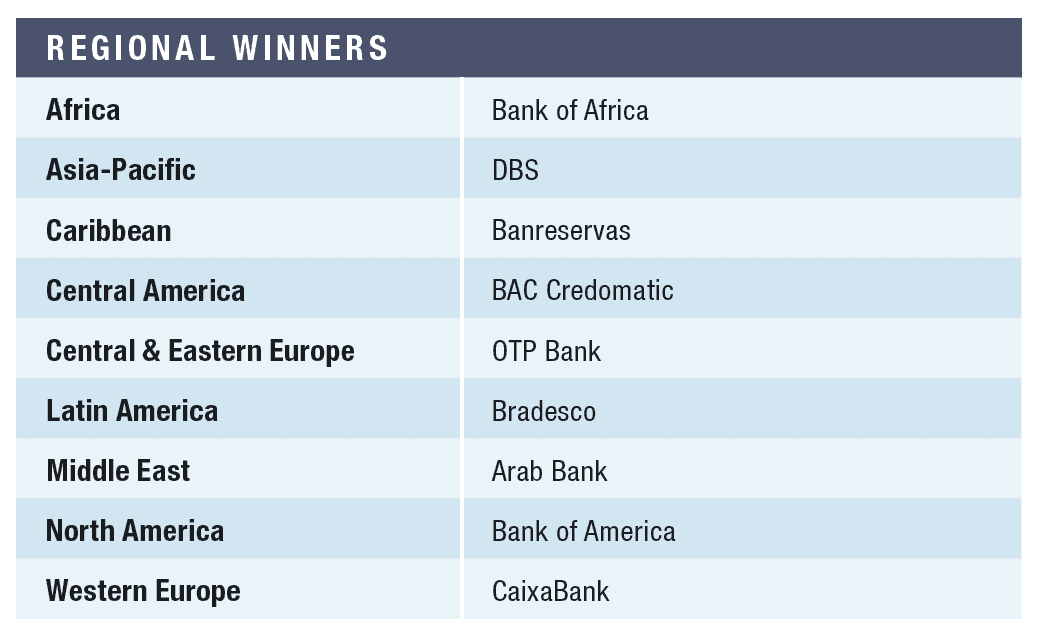

Methodology: Behind the Rankings

With input from industry analysts, corporate executives and technology experts, Global Finance editors select the winners for the Best Bank awards using the information provided in entries and independent research based on objective and subjective factors. It is unnecessary to enter to win, but materials supplied in an entry can increase the chance of success. In addition, entrants may provide private details.

Judgments are based on performance from January 1 to December 31, 2022. Then, we apply an algorithm to shorten the list of contenders and arrive at a numerical score, with 100 equivalent to perfection. The algorithm incorporates criteria weighted for relative importance, including knowledge of local conditions and customers, financial strength and safety, strategic relationships, capital investment, and innovation in products and services.

Once we have narrowed the field, our final criteria include the scope of global coverage, staff size, customer service, risk management, range of products and services, execution skills and intelligent use of technology. In the case of a tie, our bias leans toward a local provider rather than a global institution. We also tend to favor privately owned banks over government-owned institutions. The winners are those banks best serving the specialized needs of corporations as they engage in global business. The winners are not always the biggest but the best: those with qualities companies should look for when choosing a provider.