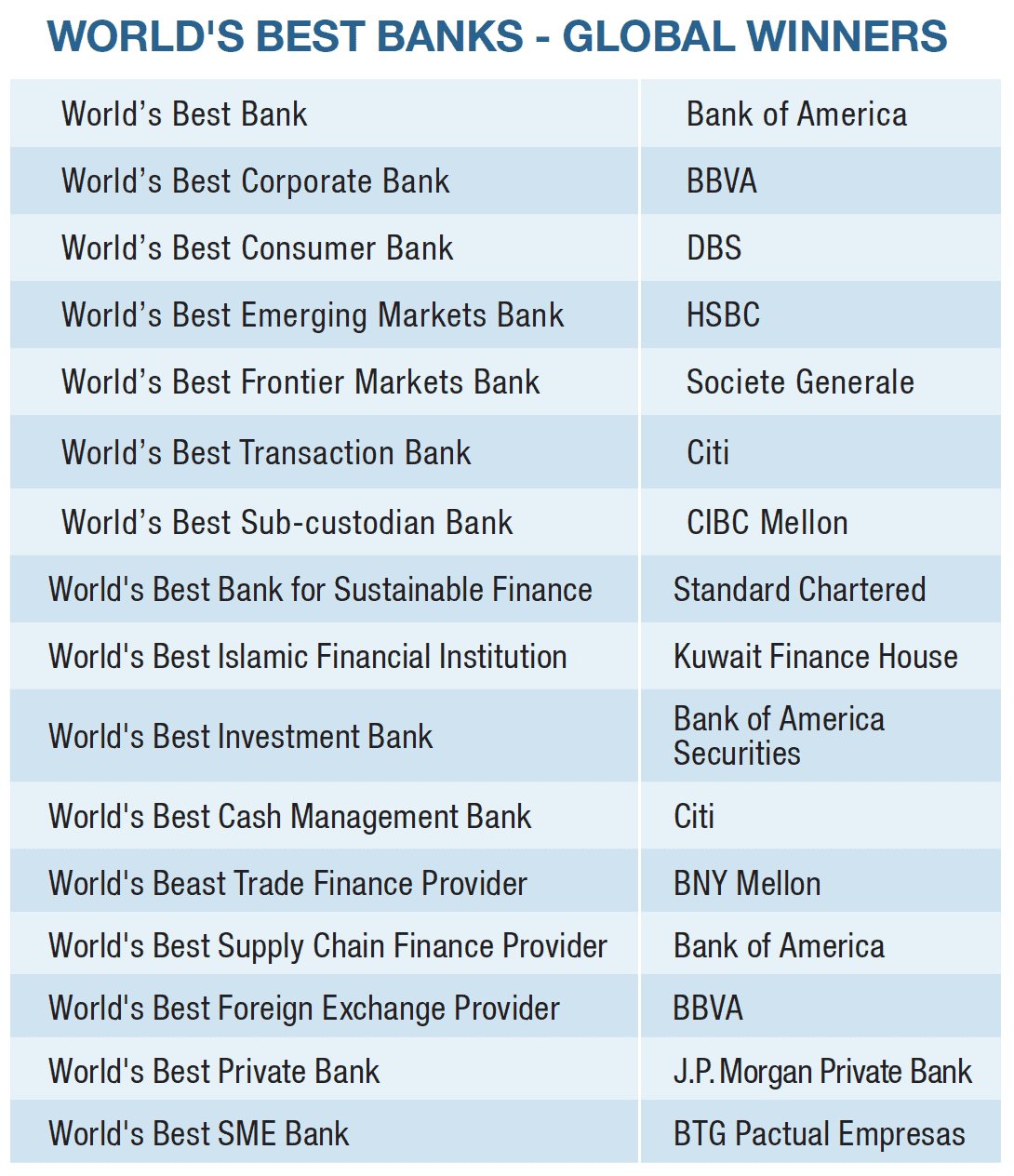

Our annual picks for the best of the best worldwide in key corporate and consumer segments.

The slowdown of the global economy and the war in Ukraine are creating uncertainty and volatility in the global markets, piling pressure on banks’ profits. Add climate change as a long-term risk—further threatening increased financial market volatility from more frequent natural disasters.

Increasing competition from fintechs, rising regulatory compliance costs, cybersecurity threats and changing customer expectations require banks to invest in new technologies and attract and retain top talent to remain competitive.

While the banking crisis, which began in March 2023 with the failure of Silicon Valley Bank, has passed, the stress in financial markets remains. Hence, banks need to carefully manage these challenges to stay profitable and sustainable in the future. This is not the time to batten down the hatches—it’s more important than ever that banks invest in technologies to transform their operations and meet customer needs.

This year’s World’s Best Bank award winner, Bank of America, which spent more than $11 billion on technology in 2022, highlights the need for banks to focus on the stability, resilience and security of their platforms to help cope with volatility. “The increased dependency between banks, clients and the market as a whole requires greater operational resilience,” explains Andrew McKibben, International Head of Technology & Operations at Bank of America. “If you get the fundamentals right, you can focus on more significant and transformational enhancements for your clients.”

A strong emphasis on innovation ensures BBVA, the winner of the World’s Best Corporate Bank and Best Global Foreign Exchange Bank awards, can support client needs. With a strong presence in Europe and Latin America, BBVA places a lot of emphasis on ensuring that its corporate and investment banking division is local, international, digital and sustainable.

“In the dynamic landscape of foreign exchange markets, technology has progressively been transforming how corporate clients manage their currency-related risks and transactions,” says Luis Martins, head of Global Macro at BBVA Corporate & Investment Banking.

“One of the most groundbreaking advancements is the emergence of AI-driven predictive analytics and algorithmic trading platforms. These offer corporate clients advanced tools to navigate the complexities of the foreign exchange (FX) markets by enhancing decision-making, reducing risks, optimizing trading strategies, and ultimately helping companies achieve more efficient and cost-effective FX operations.”

Additionally, he notes that cloud-based treasury management systems are gaining prominence among multinationals, streamlining FX exposure monitoring and allowing seamless collaboration among teams across geographies. “Therefore, integrating seamlessly with them is an important objective for BBVA. These systems offer real-time visibility into global financial positions, facilitating smarter hedging strategies and minimizing exposure to volatile currency fluctuations.”

BBVA worked extensively to digitize FX options to catch up to other products, Martins adds. “This effort has also improved our offer of short-term yield enhancement FX-linked structured products, which have become more relevant in the current interest rate environment.”

In summary, Martins says the most innovative technologies in the foreign exchange markets empower corporate clients with enhanced data analysis, efficient payment solutions, and improved risk management, ultimately ensuring smoother and more profitable international transactions.

A cloud-based microservices-based architecture, meanwhile, is helping Citi, which took home the World’s Best Transaction Bank award, to be flexible enough to handle greater payment volumes and types while handling real-time processing and data demands. The CitiDirect banking and cash management platform is now nimble enough to meet clients’ fast-changing banking and transaction needs by replacing a legacy framework of tightly coupled applications with a flexible, cloud-capable, microservices-based modular structure.

BNY Mellon, the World’s Best Trade Finance Provider award winner, has invested in emerging technology solutions, including artificial intelligence, machine learning and optical character recognition, to help unlock greater levels of automation and reduce the risk and effort related to trade finance processes.

Bank of America, which also won the World’s Best Supply Chain Finance Provider award, has committed $1 trillion to support sustainable finance by 2030. This includes embedding ESG (environmental, social, and governance) within its trade & SCF offerings.

Standard Chartered, the Outstanding Global Leadership in Sustainable Finance winner, has committed to invest $300 billion in green and transition finance by 2030. With a strong presence in emerging markets, where climate change, inequality and other threats present real challenges, Standard Chartered offers ESG products to clients and provides them with the necessary information to make informed decisions.

This year’s World’s Best Consumer Bank award winner, DBS, sends 45 million hyper-personalized nudges monthly to Singapore consumers with suggestions on making their money work harder. Meanwhile, a partnership with The Sandbox to create DBS BetterWorld, an interactive metaverse experience, will help showcase the importance of ESG issues.

Innovation is not limited to the virtual world; DBS launched a Managing Through Journeys (MtJs) program where the customer is the cornerstone of delivering outcomes. “Innovation is embedded in our new way of working,” says Han Kwee Juan, group executive and country head of DBS Singapore. “With MtJs, cross-functional teams comprising product, sales, marketing, technology, data science and operations focus on delivering a differentiated customer experience through experimentation and innovation. Through continuous discovery within MtJs, teams innovate with customers on new services and products. This enables DBS to launch new services and solutions that are seamless and joyful for customers, fulfilling our promise of ‘Live More, Bank Less.’”

Banks can stay ahead of the curve by investing in new technologies like AI, blockchain, and cloud computing while providing customers with more convenient and personalized services.

Digital transformation alleviates the negative impact of macroeconomic uncertainty. Despite the downturn, this year’s Best Banks have proved that investing in technology is helping them to drive change and continual improvement—even during difficult times. They will be in a more favorable position when the upturn arrives.

Methodology: Behind the Rankings

The editors of Global Finance, with input from industry analysts, corporate executives and technology experts, selected the global winners for the World’s Best Banks 2023 using information provided by entrants as well as independent research based on objective and subjective factors.

Entries are not required, but experience shows that the information supplied in an entry can increase the chance of success. In many cases, entrants present details that may not be readily available to the editors.

Judges considered performance from January 1 to June 30, 2023. Global Finance applies a proprietary algorithm to shorten the list of contenders and arrive at a numerical score, with 100 signifying perfection. The algorithm weights a range of criteria for relative importance, including: knowledge of the sector, market conditions and customer needs, financial strength and safety, strategic relationships and governance, capital investment and innovation; scope of global coverage; size and experience of staff; risk management; range of products and services; and use of technology. The panel tends to favor private-sector banks over government-owned institutions.

The winners are those banks and providers that best serve the specialized needs of corporations engaged in global business.

GLOBAL WINNERS |

|---|

WORLD’S BEST BANK

Bank of America

In his 2022 letter to shareholders Bank of America Chair and CEO Brian Moynihan says the company has benefited from its consistency in adherence to the tenets of its Responsible Growth strategy, mapped out in 2014. “More importantly,” stressed Moynihan, “we are positioned well for the future. In the post-pandemic period, we have reestablished our organic growth engine. We have delivered revenue growth, while controlling expense, in a highly volatile environment.”

Bank of America has set goals for reducing its environmental impact—to achieve net-zero greenhouse gas emissions by 2050, for example—and for supporting diversity, inclusion and community development. The bank has also invested in renewable energy projects, including solar and wind farms.

BofA has a mentorship program for women and minorities and supports several external organizations that are working to promote diversity and inclusion.

BofA also has several programs in place to support community development, such as a program that provides financial literacy training to low-income families. —Gilly Wright

CEO – Brian Moynihan

www.bankofamerica.com

WORLD’S BEST CORPORATE BANK

BBVA Corporate & Investment Banking

Undeniably, the past 12 months have posed a difficult landscape for corporate and investment banking, what with sticky inflation in most economies, high interest rates and debt financing harder to come by and slowing mergers & acquisitions activity. But BBVA, Spain’s second largest bank has prospered. The bank posted higher profits for the first half of the year, thanks to rising interest rates and higher loan activity, especially in Mexico, which accounted for just over half of BBVA’s net profit during the period, and record performance in debt capital markets, global transaction banking, and investment banking and finance.

“BBVA Corporate & Investment Banking’s strategy continues to be centered in our clients, sustainability, and technology,” says José Ramón Vizmanos, head of Global Client Coverage. Sustainability has been a longstanding centerpiece for the bank. Last year, it channeled €50 billion into sustainability projects, up 41% from 2021; of that figure, 81% was allocated to addressing climate change and 19% to inclusive growth. BBVA has now directed more than €136 billion into clients’ sustainable investments since 2018, when it announced a sustainable business mobilization target through 2025 of €100 billion. Last fall it tripled that target to €300 billion. BBVA’s sustainability teams and products are increasingly in demand by its clients, Vizamos says, including strategic advisory, and the bank expects them to invest heavily—specifically in decarbonization—going forward.

Technology is another area of greater concentration. “Corporate clients increasingly demand a more digitized interconnection with the bank,” says Vizamos, pointing to virtual accounts, cybersecurity, and accounts payable automation that minimizes operational risks and reduces processing times. He expects AI to become increasingly intertwined with products development and delivery as well as client interaction.

BBVA launched a new global software development division two years ago, and in the first half of last year, added almost 1,000 engineers. In July, it opened a jobs portal to hire over 2,600 STEM professionals by the end of this year.

A recent fruit of this ramp-up is PivotConnect, a human-to-human online platform that enables BBVA’s corporate clients to manage their treasury activities in any country where the bank has a presence. Another new initiative, Spark, has launched in Spain, Mexico, and Colombia to serve entrepreneurs and tech companies. —Eric Laursen

CEO – Onur Genç

www.bbvacib.com

WORLD’S BEST CONSUMER BANK

DBS

The completion in August 2023 of DBS’s NT$22 billion (US$684 million) purchase of Citibank Taiwan Ltd made the Singapore-based institution the largest foreign bank in Taiwan; more importantly, it cemented DBS’s ambitions in the Asian consumer banking space. So did the bank’s 2022 results, which saw total income from its consumer banking/wealth management businesses grow 25% to S$6.65 billion while net interest income rose 68% to S$4.27 billion, powered by higher net-interest margin and growth in loans and deposits.

Digital innovation has been key to DBS’s success. Instant account opening and automated transactions and financial statements, among other services, reduce costs and streamline the customer journey. Open banking gives DBS insight into an array of customer financial relationships, enabling the bank to provide more personalized service. NAV Planner, introduced in 2020, assesses the customer’s financial profile and makes recommendations using big data and artificial intelligence. The service has generated some 45 million hyper-personalized nudges. It’s a “democratization of wealth management” that extends capabilities to its consumer base that DBS formerly could offer only to high-income clients, says Shee Tse Koon, group executive and group head of Consumer Banking and Wealth Management.

More recently, the bank has added new online advisory centers serving its 8 million-some private and small-business clients. These fully automated branches, equipped with virtual teller machines, fill the gap between DBS’s branch banking and online/mobile banking services, enabling customers to obtain help from a remotely located teller at any hour. —Eric Laursen

CEO – Piyush Gupta

www.dbs.com

WORLD’S BEST EMERGING MARKETS BANK

HSBC

Emerging markets have weathered a difficult period, including the Covid-19 pandemic, supply chain breakdowns, higher interest rates both at home and in their larger trading partners, and a war in Ukraine that has forced many to choose sides. Foreign investors pulled money out of emerging markets for much of last year, according to the Institute of International Finance, while commodity markets, which underpin many of these economies, deteriorated.

HSBC, the largest trade finance bank globally and a longtime leader in emerging markets banking, particularly in Asia, has consistently defied the trend, combining its skills in lending, trade finance, and securities. Last fall, HSBC and the International Finance Corporation created the Global Trade and Liquidity Program, an approximately $600 million facility to help banks finance trade flows through Latin America, Central Asia, the Middle East, and Africa that had been rocked by pandemic-related disruptions. At that time, the IFC expected the program to be the first of several with HSBC “targeting the varying needs of emerging market trade finance.”

Two years earlier, months before the pandemic hit, HSBC partnered with the IFC on a very different project: the HSBC Real Economy Green Investment Opportunity Fund, the first green bond fund focused on “real economy”—i.e., non-financial—issuers in emerging markets. The fund closed with $538 million in commitments in 2021, meeting its targets even during the pandemic’s worst period.

Asian emerging markets look to be a focus for HSBC for some time to come. In 2020, it announced a goal of directing about half of its tangible equity to the region, and has been moving to dispose of some of its units in Europe, Russia, and Canada. Last year, Asia contributed 56% of the bank’s operating income. —Eric Laursen

CEO – Colin Bell

www.hsbc.com

WORLD’S BEST FRONTIER MARKETS BANK

Société Générale

With a presence in 19 African countries, Societe Generale has a long history on the continent that is today embodied in the second phase of its “Grow with Africa 2025” initiative. Grow with Africa seeks to support positive transformations on the continent, particularly the renewable energy transition. In practical terms this means supporting SMEs, innovative financing for agri-businesses and renewable energies, infrastructure financing and encouraging financial inclusion.

To support African SMEs on the continent and French SMEs in the region, Societe Generale is a key partner in initiatives such as Agence Française de Développement (AFD), which provides financing and technical assistance to projects in both developing and emerging countries and in French provinces overseas. Over the past ten years, AFD and Societe Generale supported more than 1,250 African businesses in their development projects through more than €500 million of financing guaranteed by ARIZ, a risk-sharing mechanism. Societe General was named Best Bank in Cameroon, Madagascar and Senegal by Global Finance in our regional Best Bank Awards earlier in the year.

Recent news that Societe General plans to sell its business units in Congo, Equatorial Guinea, Mauritania and Chad is offset by the decision to partner with Absa to offer the broadest pan-African coverage—27 countries. Societe Generale is also promoting China-Africa and intra-Africa corridors with eight China desks and three dedicated African desks, in Morocco, Algeria and Tunisia, to encourage trade flows between the Maghreb region and sub-Saharan countries. —GW

CEO – Slawomir Krupa

www.societegenerale.com

WORLD’S BEST TRANSACTION BANK

Citi

Citi Treasury and Trade Solutions (TTS) is as wide as it is deep—facilitating transactions in 144 currencies and 96 countries. The CitiDirect global platform enables corporates to execute all their cash and liquidity management, payments and receivables, as well as trade and foreign exchange services through online and mobile apps.

Shahmir Khaliq, Global Head of TTS, said on Citi’s Investor Day in March 2022 that the company would be investing $1 billion specifically in payments and treasury innovations.

In 2022, Citi launched a real time cash concentration capability—Citi 7-Day Sweep, which extends the automated funding of negative balances and centralization of positive balances to non-business days—to help reduce risks, increase efficiency and optimize liquidity for businesses that run 24/7, such as high-growth technology and e-commerce companies.

Citi Real-Time Liquidity Sharing, being gradually rolled out, optimizes the use of available balances—across multiple entities, currencies and accounts—enabling virtual lending and borrowing between pool accounts via a single global platform.

CitiConnect API helps treasury and enterprise systems to connect with Citi’s back-end systems. To date, Citi has processed more than 1.6 billion API calls for 90 APIs—helping to reduce the complexity and cost of bank integration while providing greater visibility and control. The ongoing implementation of a flexible cloud-capable, microservices-based modular structure will enable Citi to continue to bring greater agility to clients’ fast-changing banking and transaction needs. —GW

CEO – Jane Fraser

citigroup.com

WORLD’S BEST SUB-CUSTODIAN BANK

CIBC Mellon

This exceptional franchise encompassing all elements of the post-trade process is built on engaging and responsive client service, scalable IT infrastructure, and market leadership. The 50/50 joint venture of CIBC and BNY Mellon amassed more than $1.8 trillion in assets under administration as of year-end 2022, a strong track record of generating new mandates, and a near 100% client retention rate. Maintaining consistently high service depends on a top-notch workforce, and CIBC Mellon’s dedicated team of 1,800 holds long tenures in the sub-custody business

Cutting-edge systems and technology are the backbone of securities services, and ongoing technology initiatives are focused on continued process automation, with updated Swift messaging standards to provide seamless secure data transmission and high straight-through processing rates. Additionally, CIBC will continue migrating clients from its legacy platform to BNY Mellon’s GSP custody platform through 2023 to ensure service continuity.

Recognizing the importance of customer alignment in a technology-driven business, CIBC continues to engage with its clients in a deep-dive data-assessment initiative. One area is in digital assets, where CIBC is collaborating with stakeholders to support digital asset offerings. The bank serves as fund administrator for the world’s first retail bitcoin and ether ETFs, in addition to servicing 21 of the 42 retail cryptocurrency offerings available in Canada. —David Sanders

CEO – Mal Cullen

www.cbicmellon.com

BEST BANK FOR SUSTAINABLE FINANCE

Standard Chartered

Standard Chartered’s portfolio of sustainable finance assets grew by 40% year-on-year (from $9.2 billion in 2021). Focusing on emerging markets, where the financing gap for sustainable growth is the greatest; Standard Chartered is committed to mobilize $300 billion in green and transition finance by 2030.

Emerging markets are lowest contributors to global CO2 emissions and yet are disproportionately harmed by climate change. “Their ambitions to grow and prosper are no different than elsewhere, but because of their starting point, they have the potential of being able to incorporate the latest technologies and lessons learned by other geographies,” says Marisa Drew, Chief Sustainability Officer, Standard Chartered. “Often the hardest part of climate change mitigation is transitioning deeply embedded legacy systems. This is where the emerging markets have a unique advantage and outsized role to play. They have an ability to more easily and quickly adopt the emergent, game-changing technologies that will support their sustainable future.”

Drew notes a key element of Standard Chartered’s excellence focused training and resourcing that enable staff to deliver tailored solutions. “As sustainable finance is a relatively new proposition for most companies and one that is complex and evolving rapidly, timelines for implementation and scaling need to take into consideration organizational readiness to embed,” she continues. “It is critical that the front-line origination teams through to the second line and support functions in risk, operations, compliance and legal are well educated, both on the sustainable finance topic generally and on the bank’s specific product offering—and are well resourced to support the delivery.” —GW

CEO – Bill Winters

www.sc.com

BEST ISLAMIC FINANCIAL INSTITUTION

Kuwait Finance House

Kuwait Finance House’s $11.6 billion acquisition of Ahli United Bank last year boosted its assets to around $121 billion and made KFH the second largest Islamic bank in the world, behind Saudi Arabia’s Al Rajhi Bank, and a major player in Gulf Cooperation Council markets.

The first half of 2023 saw KFH post a record $1.9 billion net profit, an increase of 141.4% over the same period in 2022, and a 73.3% increase in earnings per share, reflecting big jumps in both net financing and net operating income and smaller increases in total assets and depositors’ accounts.

KFH is striving to offer a forward-looking profile in the Islamic space, capitalizing on the steady advance of shariah-compliant banking even through the Covid-19 pandemic crisis. Last year, the bank expanded its investment and trading activities in primary and secondary capital markets, boosted its dealmaking for sovereign and corporate sukuk, and participated in major development projects in the GCC and globally in infrastructure, energy, water and electricity, transportation, communications, real estate, and oil. It is also seeing to its green bona fides, having signed a memorandum of understanding in January with the United Nations Development Program committing KFH to a stronger alignment with the UNDP’s Sustainable Development Goals.

Perhaps just as importantly, KFH is moving to establish itself as a digital innovator. Following its acquisition of Ahli United, it announced that it would convert AUB Kuwait into a digital bank. More broadly, it is using fintech and artificial intelligence to enhance operations and the customer experience. —EL

CEO – Abdulwahab Iesa Alrushood

www.kfh.co

WORLD’S BEST INVESTMENT BANK

Bank of America Securities

Inflation declined in the first half of 2023, and by skipping a rate hike in June, the US Federal Reserve signaled that the worst of the post-pandemic inflation may be over. The investment banking sector nevertheless continues to feel the effects of an unsettled global landscape for borrowing and investment, including China’s uncertain economic recovery, political and trade tensions between Beijing and Washington, and the trade disruptions caused by the accelerating war in Ukraine. Mergers and acquisitions fell 40% globally during the first half, according to Dealogic, and investment bankers sustained a 37% decline in global revenue on M&A transactions, one of the biggest drops on record.

The picture brightened somewhat in the second quarter, and nowhere was this more apparent than in results posted by our Best Investment Bank Award winner, Bank of America Securities. BofA’s sales and trading revenue increased 3% from a year earlier in the second quarter, for a total of $4.3 billion; revenue from fixed income, currencies, and commodities trading rose 7% to $2.7 billion from the same period last year. The New York-based bank posted $252.9 billion in M&A advisory fees through mid-July, placing it fourth on Dealogic’s M&A Scorecard—and while that figure was down more than half from the same period in 2022, many other major providers fared worse. —EL

CEO – Brian Moynihan

bankofamerica.com

WORLD’S BEST CASH MANAGEMENT BANK

Citi

The demise of Silicon Valley Bank and Signature Bank earlier this year, coupled with high interest rates, are concentrating corporate treasurers’ attention on protecting their cash. Some are looking to tame counterparty risk by diversifying their deposits among multiple banks while further centralizing cash management across the organization in order to gain better visibility and thus greater efficiency and tighter control of their cash positions.

Cybercurrency theft and cyber-attacks loom as major risks; payment hubs and in-house banks offer more direct control of payment execution, but also promise better fraud detection via payments process controls. At the same time, treasurers and cash managers are looking to technologies such as AI to help them improve cash forecasting and get ahead of liquidity and counterparty risk.

Citi is addressing the demand for greater control by offering a real-time liquidity-sharing capability that automates and optimizes the use of net available balances dispersed across multiple entities and accounts. It also provides virtual lending and borrowing between pool accounts via a single global platform with automated liquidity controls and other limit-setting capacities. —EL

CEO – Jane Fraser

www.citigroup.com

BEST TRADE FINANCE PROVIDER

BNY Mellon

BNY Mellon has made significant investments in emerging technology solutions—such as artificial intelligence, machine learning and optical character recognition—to bring greater levels of automation and reduce the risk and effort related to existing processes within the trade finance process.

“Our agile approach to optimizing traditional trade finance products is what stands out this year. For instance, our new hybrid outsourcing offering is helping to solve clients’ major pain point areas such as technology implementation costs. Our clients can access our portal service and our full outsourcing offering without fully integrating the whole back-office system,” states Joon Kim, Global Head of Trade Finance Product & Portfolio Group, BNY Mellon Treasury Services.

“Elsewhere, we are leveraging our robust correspondent banking coverage—and our position as a largely unconflicted provider—to create and offer various risk mitigation services for clients to expand reach as well as consider a flexible global supply chain financing program with short implementation times.” By offering trade outsourcing capabilities to other banks, BNY Mellon helps them avoid the high costs of contracting with a third-party trade platform whilst allowing them to benefit from a state-of-the-art, customizable trade portal, BNY Mellon’s extensive global network, trade expertise, and contingency planning infrastructure to enhance their trade service offerings. —GW

CEO – Mal Cullen

cibcmellon.com

WORLD’S BEST SUPPLY CHAIN FINANCE PROVIDER

Bank of America

Having offered SCF as a core solution for clients for the past decade, last year Bank of America made enhancements in CashPro Trade to include SCF APIs, ESG-linked Trade and SCF, new Trade Receivable Finance and Trade Risk Purchase modules and a Third-Party Module and channels, which can be integrated via either API or host-to-host to connect clients’ platform with CashPro Trade.

In 2022, a Supplier Enablement Portal (SEP) was rolled out in all regions to enable the speedy onboarding of suppliers across the whole supply chain. In addition to an online portal

SEP includes advanced data analytics software, powered by AI, personalized microsites for suppliers with information, such as a calculator to gauge financial benefits and real-time supplier status reports, to enable tracking of onboarding.

BofA is also involved in two pilots with the distributed ledger, Marco Polo Network. One is focussed on digitalizing the end-to-end procure-to-pay process by facilitating the flow of information and funds seamlessly within a private DLT system. The second combines artificial intelligence, DLT and digital verification databases to unlock the ability to on-board the entire supplier base and scale programs at speed. —GW

CEO – Brian Moynihan

www.bankofamerica.com

WORLD’S BEST FOREIGN EXCHANGE PROVIDER

BBVA

BBVA boasts a strong global network—providing its customers, who include individuals, SME’s, corporates and investors with access to foreign exchange markets in over 100 countries.

To help SMEs cope with today’s high inflation and interest-rate environment, BBVA has been particularly active in ensuring that smaller clients use FX derivatives for hedging purposes. Speaking with Global Finance earlier in the year, Luis Martins, head of Global Macro at BBVA, said this involves providing necessary credit so they can trade without any liquidity requirements, launching some online hedging tools for clients to simulate potential scenarios and hedging strategies and making FX instruments available electronically for easy and fast execution.

BBVA has also adopted technologies, such as SWIFT GO, FX Net Cash and BBVA eMarkets. BBVA was one of the first ten banks in the world to join SWIFT GO and was the first bank to launch it in Spain, Mexico, Peru and Turkey. With 85% of payments completed in three minutes or less, SWIFT GO aims to be a solution for low-value payments and help streamline the collection of payment for services to cross-border clients for SMEs.

BBVA posted record revenues for the first half of 2023, with year-on-year growth of 48%. Of merit was growth for Global Markets, highlighting the FX business in all geographies where BBVA operates, with an extraordinary contribution from emerging markets. Also noteworthy is the excellent performance of BBVA’s rates business in South America and growth in the US. —GW

CEO – Onur Genç

www.bbva.com

WORLD’S BEST PRIVATE BANK

J.P. Morgan Private Bank

A multiyear Global Finance award winner, J.P. Morgan, with client assets of $2.1 trillion, again takes the title of World’s Best Private Bank. That places it in a premier position in a heady business that is expected to grow dramatically; Cerulli Associates has calculated that wealth transferred through 2045 will total a staggering $84.4 trillion, including $72.6 trillion in assets passing to heirs and $11.9 trillion donated to charities.

J.P. Morgan is positioning itself for private banking as a more global business. Last year, it announced plans to double the headcount in its European and MENA operations and also grow its headcount in Asia, which boasts one of the world’s fastest growing contingents of very high and ultra-high net worth clients, by 100. In July, it launched a new US Family Office Practice with 150 specialists including in tax planning, estate, and cybersecurity.

“Our clients are looking for highly customized solutions, innovative digital services, and resources to address the growing complexities of multi-generational wealth,” Andrew L. Cohen, executive chair of J.P. Morgan Global Private Bank, said in a statement at the time. “The launch of this practice will provide a robust solution set for family offices across the wealth spectrum.”

J.P. Morgan is also sharpening its technological edge. Over the past two years, it has bought two fintech firms, OpenInvest and Global Shares, and invested in two others, Edge Laboratories and Evooq, Swiss firms that specialize in analyzing risk and customizing portfolios for wealthy clients. —EL

CEO – David Frame

privatebank.jpmorgan.com

WORLD’S BEST SME BANK

BTG Pactual Empresas

Few areas of financial services are as ripe for digital transformation as banking for small and mid-sized enterprises. A little over three years ago, Brazil’s BTG Pactual set up a new operating arm, BTG Pactual Empresas, to serve smaller business. Since then, the unit has lent BRL130 billion to SMEs—16% of the bank’s total credit portfolio. It balances the innovation and agility of a startup with the range and capabilities of an established brick-and-mortar bank.

BTGP Empresas attributes its rapid success in attracting platform users, new SME clients, and new partners to its fully online onboarding process; multichannel customer support; as well as payroll, federal tax accounting, and other offerings.

The digital bank has integrated its business and technology teams, giving its developers a deeper understanding of customers. A strong network of early-adopter customers provides feedback at all stages of product development. Last year, it partnered with a startup to introduce a tool that estimates past crop yields and predicts future performance for farmers via satellite data analysis. —EL

CEO – Roberto Sallouti

ri.btgpactual.com