MERGERS & ACQUISITIONS

|

The volume of worldwide mergers and acquisitions totaled $730 billion in announced deals in the first quarter of 2008, a decline of 24.2% from the first quarter of 2007 and the lowest level for deal activity since the third quarter of 2006, according to Thomson Financial. The outlook is not entirely bleak, however, with a significant number of takeovers likely this year in the troubled financial services industry as well as in the booming energy sector.

Private equity firms were left largely on the sidelines during the first three months of this year due to the uncertain environment in the global credit markets, Thomson Financial said. The $81.3 billion in announced deals involving financial sponsors was the lowest since the third quarter of 2005.

“While objectively there has truly been a slowdown in M&A; activity, particularly in the private equity world, this should be put in perspective,” says William Kucera, partner at Chicago-based Mayer Brown, who represents buyers and sellers in acquisitions and divestitures. “The recent past was a statistical outlier, with the highest volume of deals on record,” he says.

|

|

Kucera: “The recent past was a statistical outlier.” |

A significant number of deals are still getting done, particularly those involving strategic buyers with good balance sheets and cash reserves, according to Kucera. Private equity firms are still doing deals as well, but the transactions are not as big as they were a year ago, he says. “The middle market is still relatively strong,” he points out. “If you are a well-positioned buyer, there are opportunities.”

Two industries that will continue to have a large volume of M&A; transactions this year are finance and energy, but for completely different reasons, Kucera says. In financial services, deals are being done out of necessity, whereas in the oil and gas industry, where companies are making a lot of money, they are buying assets at inflated prices, he says.

Meanwhile, sovereign wealth funds, such as the Government of Singapore Investment Corporation and the Kuwait Investment Authority, took significant stakes in US banks, including Citi and Merrill Lynch, in the first quarter of 2008 and are likely to make additional investments.

The number of sovereign wealth funds has surged, as Asian nations and oil exporters in the Middle East seek higher returns on their massive currency reserves by taking stakes in companies. The funds have assets of about $3 trillion, and Morgan Stanley forecasts that their holdings may quadruple by 2015. They more than doubled their global M&A; spending last year with acquisitions of companies and minority stakes of more than $60 billion.

Sovereign wealth funds could take up some of the slack in the market caused by the slowdown in the private equity industry. They take a longer-term view of investing and are not affected by changes in the credit cycle. These funds accounted for more than one-third of global M&A; in 2007.

|

Hedge funds have increasingly become takeover targets. Sales of alternative investment firms, the majority of which were hedge funds, accounted for a record 40% of deals in the global investment management business in the first four months of this year, according to Jefferies Putnam Lovell, a division of New York-based investment bank Jefferies.

“We expect record demand for alternative asset managers to continue throughout 2008, motivated by buyers’ search for absolute returns and innovative products in challenging capital markets,” says Aaron Dorr, managing director at Jefferies Putnam Lovell. The firm has advised on several of the most significant transactions involving alternative investment firms so far this year, including the sale of an interest in Stamford, Connecticut-based Aladdin Capital Management to Mitsubishi. It also advised on the sale of Carlsbad, California-based hedge fund administrator HedgeWorks to Deutsche Bank.

Leveraged buyouts, which had played a major role in driving M&A; activity in recent years, came to an abrupt halt in the first quarter, as US announced volume decreased by nearly 90% due to the deteriorating credit environment, according to Thomson Financial. However, stock-swap transactions increased significantly and accounted for 34.2% of US announced M&A; volume in the first three months of this year.

US companies continued to attract foreign investment during the first quarter, as the dollar declined against the euro for a sixth consecutive quarter. However, the $46.5 billion of inbound cross-border M&A; transactions was down 40.3% from the same period a year earlier.

Europe Takes the Lead

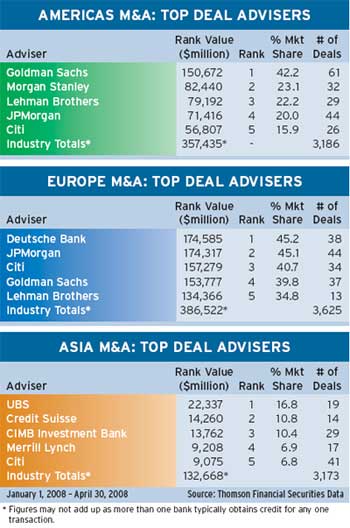

European announced M&A; volume outpaced that of the US in the first quarter of 2008. The European total of $340 billion represented an increase of 2% from the first quarter of 2007. Altria’s $113 billion spinoff of Philip Morris International, one of the world’s biggest tobacco companies, was by far the largest deal of the first quarter of 2008 and comprised 28.7% of European M&A; activity.

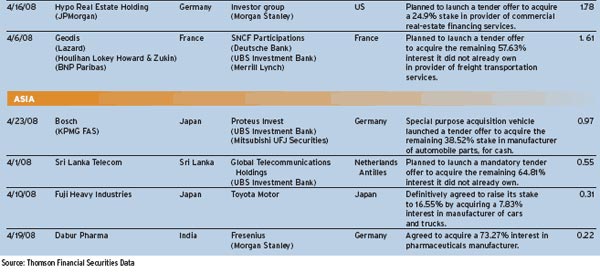

M&A; activity in Asia, excluding Japan, increased by 12.2% to $120.6 billion in the first quarter of 2008. Japan’s activity decreased by 49.2% from the same period last year to $26.9 billion, the country’s lowest first-quarter total in four years.

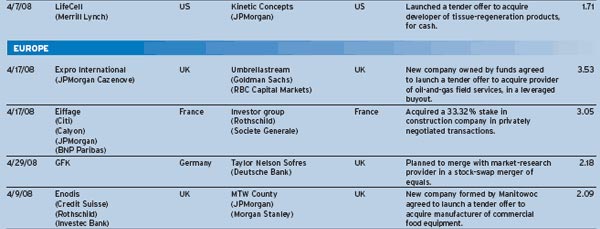

The biggest M&A; deal announced in Europe in April was in the energy sector. Funds managed by private equity firm Candover Partners, Goldman Sachs Capital Partners and Amsterdam-based AlpInvest Partners agreed to buy UK-based oil services company Expro International for $3.53 billion. The funds agreed to launch a tender offer through a special-purpose acquisition vehicle known as Umbrellastream. They were required to put up more than 40% of the purchase price in cash. JPMorgan Cazenove advised Expro International, while Umbrellastream’s financial advisers were Goldman Sachs and RBC Capital Markets.

Expro International provides specialized services to the oil and gas industry that focus on measuring, improving and controlling flow from oil and gas wells. Oil and gas industry services providers are coming into growing demand as energy companies increase their exploration and development budgets in response to record-high oil prices. In the United Kingdom alone, oil-services firms Abbot and Sondex have been takeover targets in the past six months.

Optimism Begins to Wane

While M&A; activity in Europe has held up relatively better than in the US this year, optimism in the European deal market has fallen since last September as the credit crunch continues to bite, according to the latest biannual survey conducted by London-based IntraLinks, which provides workspaces for secure document exchange. The firm’s recent survey of corporate bankers, lawyers and advisers throughout Europe found that positive sentiment has declined by 30% since September 2007 but that 61% of respondents are still optimistic on the outlook for M&A; in the next 12 months. More than 80% of those with a pessimistic view of M&A; see the lack of debt-financing opportunities as the primary barrier to deal flow. Nearly three-quarters of respondents expect a reduction in the number of very big deals and an increase in mid-size deals as the key M&A; trend for 2008. Two-thirds of those surveyed said general economic uncertainty will restrict the number of transactions.

Across sectors, respondents predicted that the energy industry would see the highest level of M&A; activity in the next 12 months. Deal activity in the financial services industry was also predicted to feature prominently.

“The M&A; market faces very challenging conditions, for the time being at least, but opportunities are still out there,” says Andrew Pearson, managing director for Europe, the Middle East and Africa at IntraLinks. “The market, quite correctly, is cautious but not cowed,” he says. IntraLink expects a flight to quality, he adds, as companies choose their engagements with even greater circumspection.

|

While companies are struggling in some cases to raise money for takeovers in the current credit environment, some very big deals are still getting done, even in the quiescent US market. On April 28 it was announced that Warren Buffett’s Berkshire Hathaway and Mars would acquire Chicago-based gum maker Wm. Wrigley Jr. for $23 billion.

To help fund the buyout, privately held Mars is relying on $4.4 billion in subordinated debt from Berkshire Hathaway, which will also buy a $2.1 billion equity interest in Wrigley when it becomes a Mars subsidiary. Goldman Sachs and JPMorgan also provided financing for the transaction.

The deal is structured as a private equity leveraged buyout with a reverse termination fee structure. The fee is payable to the target company in the event of a failure to close the transaction. Mars can walk away from the deal at any time if it pays Wm. Wrigley Jr. $1 billion. The fee is also payable if the deal fails to get antitrust approvals.

If the buyout receives regulatory and shareholder approval, it will create the world’s largest confectionery company, ahead of UK-based Cadbury Schweppes. The transaction could spur a round of consolidation in the candy industry. Hershey and Cadbury Schweppes have been discussing a potential merger for years but have so far been unable to tie the knot.

Fees Fall Faster Than Deals

Outpacing the decline in new deal announcements in the first quarter of this year, fees for completed M&A; financial advisory assignments fell 28.8% to $7.4 billion from $10.4 billion in the first quarter of 2007, according to Thomson Financial and Freeman, a boutique M&A; advisory and consulting firm. New York-based Freeman uses an algorithm-based model for imputing fees from deal volume.

Goldman Sachs ranked first in imputed fees for worldwide M&A; deals completed in the first quarter, with $433 million from 68 deals, followed by Credit Suisse, with $324 million from 69 deals. The rest of the top five, ranked by imputed fees in the first quarter, were Merrill Lynch, Lehman Brothers and Morgan Stanley. Lehman Brothers was the only major investment bank to record an increase in fees in the first three months of this year compared to the same period a year earlier.

Gordon Platt