Big Cross-Border Mergers May Remain Rare Occurrences In Europes Financial Sector

When Abbey National, then the sixth-largest bank in the UK, agreed in July 2004 to a takeover bid of about $15.5 billion from Banco Santander, Spains biggest bank, analysts said the deal could herald a wave of major cross-border bank mergers in Europe. The long-awaited consolidation of the European Unions financial services industry was under way, and the creation of a pan-European system would result, they said.

It wasnt until a year later, however, that the next big cross-border acquisition took place in Europes fragmented banking sector.

In July 2005 Italy-based UniCredito agreed to acquire Germanys HVB and its Bank Austria Creditanstalt unit with an extensive network in the fast-growing economies of Central and Eastern Europe.

The $18.7 billion bid to take over Germanys second-largest bank followed failed attempts by UniCredito in recent years to form alliances with Spains Banco Bilbao Vizcaya Argentaria, or BBVA, and with Commerzbank, also of Germany.

Together, UniCredito and HVB will be a strong new force rooted at the heart of Europe, says UniCreditos chief executive, Alessandro Profumo. We will become the first truly European bank.

While the deal was the largest cross-border banking merger ever in Europe, analysts say that mega-mergers that cross Europes borders will remain an anomaly. This is not the start of a frenzied game of musical chairs that will have Europes big banks aggressively seeking new partners, they say.

Politics and cultural differences, as well as differing legal, regulatory and tax systems, make it difficult for any EU banking monolith to emerge, industry participants and analysts say.

There wont be many more transformational deals, says Stephen Jancys, vice president of mergers and acquisitions at New York-based Trenwith Securities, an independent investment banking affiliate of BDO Seidman and BDO International, which has a global network of 600 offices that provide financial advice and consulting services.

The volume of middle-market deals in the European financial services industry will continue to be much larger than that of the major mergers, Jancys says.

Trenwith Securities represents both US and non-US companies in middle-market transactions. Its clients range from middle-market businesses to multinational corporations seeking to acquire or divest middle-market companies.

European banks need to step up their domestic mergers to avoid being absorbed by international rivals, including the big US banks, Jancys says. They need to become bigger fish so that they are not takeover targets themselves, he explains.

There will be more consolidation in European financial services, particularly in the fragmented markets of Italy and Germany, Jancys adds.

* Figures may not add up, as more than one bank typically obtains credit for any one transaction.

|

Quality Assets for Sale |

|

Private equity firms will increasingly be involved in the restructuring of banks and insurance companies, with many institutions divesting non-core businesses, according to Jancys.

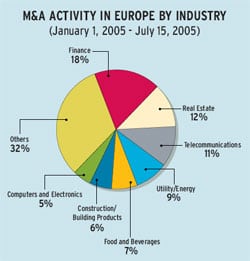

A lot of quality assets are available for sale, including credit-card businesses and consumer finance operations, he notes. There also will be further consolidation in the asset-management industry, where costs have increased in order to keep up with the growing burdens of financial reporting, Jancys says. Deutsche Bank signed an agreement in July 2005 with UK-based Aberdeen Asset Management on the sale of part of the German banks asset-management businesses in the UK and the US, in a transaction valued at about $450 million, depending on future fee revenue. Deutsche Bank said the deal followed a comprehensive and strategic review of its asset-management business globally. The objective is to create a stronger, more focused Deutsche Asset Management business that can provide greater value to our clients and shareholders, says Kevin Parker, member of Deutsche Banks executive committee and global head of Deutsche Asset Management. The German banks UK-based hedge-fund and real-estate businesses and its Philadelphia, Pennsylvania-based high-yield business were not part of the deal and remain part of Deutsche Asset Managements global platform. Meanwhile, Spains BBVA is pursuing Italy-based Banca Nacionale di Lavoro, while ABN AMRO of the Netherlands is battling for control of Banca Antonveneta. Overall M&A; activity within Europe reached $427 billion in the year-to-date through July 15, 2005, according to Dealogic. That represents an increase of 33% compared to the same period of 2004, it says. Finance was the most-active industry for intra-European M&A; activity, with $75.8 billion from 331 transactions. The UK remains the most-targeted country for M&A; in Europe, Dealogic says. |

Turkish Banks Targeted

|

|

|

Rabobank of the Netherlands agreed in July to buy a controlling interest in Sekerbank, the bank of the sugar-beet cooperatives, for about $350 million.

We are developing bank partnerships in a selected number of fast-growing Central and Southeastern European countries, says Harry de Roo, member of the managing board of Rabobank International. Our aim is to develop local community banks which operate close to their customers, with a particular focus on non-metropolitan areas, he says.

Sekerbank has 201 branches, of which 130 are located outside Istanbul and Ankara.

Also in July, the Dutch-Belgian banking group Fortis purchased an 89.3% stake in Disbank of Turkey for $1.27 billion. Disbank, Turkeys seventh-largest privately owned bank, has more than 1 million customers.

UniCredit of Italy paid $1.46 billion in May to acquire a 57% controlling stake in YKB, or Yapi ve Kredi Bankasi, in cooperation with the Turkish finance company Koc Finans.

Earlier this year, BNP Paribas of France acquired 50% of the holding company that controls Trk Ekonomi Bankasi, or TEB. Meanwhile, Deutsche Bank bought the remaining 60% it did not already own of Bender Securities, a mid-size brokerage house based in Istanbul. The German bank also acquired a commercial banking license in Turkey.

|

Merger Activity Increases |

In 2004, European financial services M&A; activity increased by approximately one-third in terms of total announced deal values and total deal numbers compared with 2003, according to a report by PricewaterhouseCoopers, or PwC. With approximately $54 billion of deals announced, financial services was the second most-active sector in Europe after pharmaceuticals last year. According to PwC, there was a significant increase in the proportion of cross-border deals, representing 61% of all financial-services merger activity in Europe in 2004. The report predicts increased appetite from private-equity investors and a continued focus on divestments of non-core businesses. In banking, PwC foresees limited significant European cross-border M&A;, with larger deals such as the acquisition of HVB by UniCredit continuing to be a rarity. We had one big cross-border deal last year [Santanders purchase of Abbey] and another big deal this year, says Nick Page, London-based partner in TS Financial Services, part of the transaction services group of PwC. There remain impediments to the industry consolidating quickly, Page says. Cross-border mergers will continue to increase in coming years, but we may see only one big transaction a year, he says. Following the big banking mergers in the US in the past few years, US predators may look to the UK or possibly Europe for their next move, according to the PwC study. In the short term, however, Asia might offer slightly more exciting opportunities, Page says. It wont be easy for a major US bank to create a pan-European banking company with a single acquisition, Page notes. If you buy a bank in the UK, you are buying a UK bank, Page says. And if you buy a bank in Germany, you are getting a German bank. You are not gaining a pan-European presence, he says. Meanwhile, European financial institutions will continue to rationalize the products they want to offer, according to Page. Some diversified groups with asset-management operations might divest these activities, but there will be no big consolidation in this sector, he says. |

Rise of Private Equity

Private-equity investment in European financial services is expected to grow and is a potentially significant trend, Page says.

In recent years, private-equity funds have been getting bigger, following a greater focus on alternative investments, resulting in a significant increase in the amount of money these funds have to invest. Fund managers are becoming adept at operating within the regulatory regime of European financial services and at managing compliance issues, according to PwC.

There are plenty of opportunities for private equity funds to participate, such as in buying non-performing loans in Italy, Germany or emerging Europe, Page says.

The availability of billions of dollars of relatively low-cost credit that the major banks are offering has enabled private-equity funds to leverage the companies they are acquiring, according to the PwC report.

Some market watchers are talking about a potential credit bubble, but the major financial services deals seen in Europe are all built on recurring cash flows, it says. It is precisely the cash-generating nature of these financial services businesses that makes them particularly attractive to private-equity investors, it adds.

Increased activity from private-equity firms in the financial services sector may increase the pressure on major corporations to make acquisitions earlier than they otherwise would, it predicts.

In one of the biggest changes in the German banking industry in many decades, the countrys Landesbanks, which are partially state-owned, lost their government backing in July. These guarantees, which had enabled them to raise money at lower interest rates than their private-sector competitors, were eliminated at the EUs insistence.

In what analysts describe as a healthy trend, the Landesbanks, along with the municipally owned savings banks, now have to compete on a level playing field with the countrys private banks. Some of the Landesbanks could seek merger partners as they try to defend their market shares in the newly competitive environment.

While the Landesbanks have become more like commercial banks, the transformation is not yet complete, according to New York-based rating agency Standard & Poors. The Landesbanks need to continue with restructuring efforts and successfully implement their game plans, the rating agency says.

Top Mergers and Acquisitions (July 1, 2005-July 28, 2005)

Gordon Platt