FOREIGN EXCHANGE

|

Following the dollar’s worst quarterly loss against the euro since 2004—a drop of 8.4% in the first three months of this year—currency analysts are watching for signs that the greenback could be ready to make a comeback. They caution, however, that the dollar is unlikely to rise significantly against other major currencies until US interest rates stop declining.

The dollar should do relatively well over the medium term, as it is probably quite near a bottom, says Mark Frey, head trader at Custom House, a global payments company and foreign exchange dealer based in Victoria, British Columbia, Canada.

In order to sustain a rally, however, the dollar bulls will need a clear signal from the Federal Reserve that it has reached the breaking point in its accommodative monetary policy, Frey says. “The dollar could trade sideways for a while, until the Fed changes its tune,” he says. “As a trader, I want to see confirmation from the Fed that it has reached the end of its easing.”

At some point, the Fed will likely become more concerned about inflation, according to Frey. “Aggressive rate cuts alone won’t necessarily help economic growth,” he says. “Market participants have confidence that the Fed will do what it has to do, and that confidence is a plus for the dollar.”

Traders Await Fed’s Signal

Even if growth in the US economy does not pick up later this year, but inflation is advancing, the Fed would have to address the inflation situation by raising interest rates, Frey says. The foreign exchange market is very sensitive to interest rates and would respond very quickly to the right signal from the Fed, he explains. “Even a modest tightening of policy will likely be enough to positively influence the overall sentiment with respect to the dollar,” he says.

|

With the dollar falling and oil prices rising, some market participants are moving into commodities, including petroleum and gold, Frey observes. “They are buying black and they are buying yellow,” he comments. However, any change of sentiment regarding the prospects for the dollar would likely take the froth out of the commodities markets, he predicts.

The Canadian dollar is strongly correlated with commodities prices and agricultural prices, according to Frey. “The run-up in commodities has underpinned the strength of the Canadian dollar,” he says. “Energy will be held dear for the next generation, and the Canadian dollar looks attractive and well positioned, but it is considerably overvalued against the US dollar right now,” he notes.

CURRENCY FORECASTS

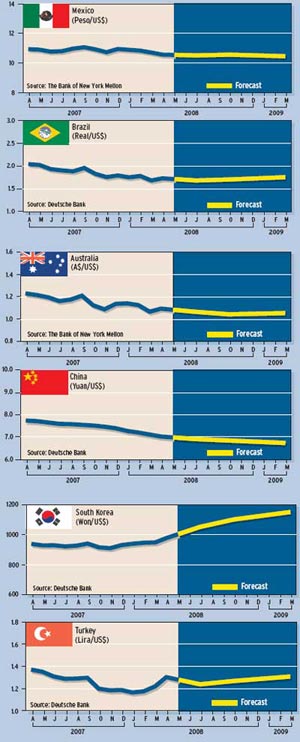

Meanwhile, the Mexican peso is doing well in the face of a US slowdown. One reason could be the peso’s relative underperformance in recent years compared to gains made by the currencies of Mexico’s main export competitors in Latin America and Asia, says Clyde Wardle, chief currency strategist for emerging markets at HSBC Bank (USA), based in New York. Mexico’s construction industry is also doing well, while its services sector is growing in importance and is less vulnerable to US trends than manufacturing, he says. The Mexican government is flush with cash, thanks to high oil prices, and foreign direct investment is strong, he adds. “However, we do expect the US downturn to worsen,” he says, which likely will cause the peso to weaken.

Meanwhile, the Mexican peso is doing well in the face of a US slowdown. One reason could be the peso’s relative underperformance in recent years compared to gains made by the currencies of Mexico’s main export competitors in Latin America and Asia, says Clyde Wardle, chief currency strategist for emerging markets at HSBC Bank (USA), based in New York. Mexico’s construction industry is also doing well, while its services sector is growing in importance and is less vulnerable to US trends than manufacturing, he says. The Mexican government is flush with cash, thanks to high oil prices, and foreign direct investment is strong, he adds. “However, we do expect the US downturn to worsen,” he says, which likely will cause the peso to weaken.

Losses Still Not Extreme

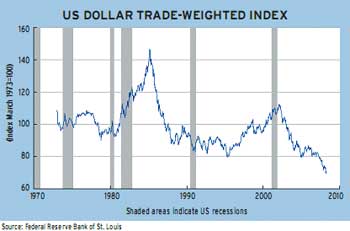

The US dollar has exhibited four major bear markets in the post-Bretton Woods era of floating exchange rates, with the current bear market the second worst on record, according to John Normand, global currency, commodity and fixed-income strategist at JPMorgan Securities, based in London. Despite the pace and extent of the dollar’s decline, however, the current environment is not yet as extreme as at the end of previous bear markets, he says. The euro’s gains over the past year are still shy of those seen in the dollar’s fall after the Plaza Agreement of 1985, for example.

“Contrary to the belief that currency markets are operating in uncharted territory, they appear more to be following a well-worn path which has further to run,” Normand says. The dollar offers no yield compensation for a further near-term decline in price, he says. The “capitulation trade,” or the last gasp lower before the dollar hits bottom, should be a point of maximum pessimism, characterized by significant position liquidation or reversal, he adds.

“It is difficult to rationalize bottom-fishing in the dollar until the capitulation indicators signal further pessimism [than they do now] or until rate trends within the Group of 10 [major industrialized countries] begin to reverse,” Normand  says.

says.

Recession Impact Unclear

Binky Chadha, strategist at Deutsche Bank Securities, based in New York, says the bank’s economists view the US economy as having slipped into recession, but that from a historical perspective the dollar has not displayed any clear patterns in past US recessions.

Longer-term cycles in the dollar have dominated the effects of recessions, Chadha says. “The empirical evidence suggests that it is relative [economic growth] rather than absolute or global growth that has been the more important driver of the dollar,” he says. This growth differential between the United States and its partner countries is expected to widen over the second quarter, but relative growth could narrow in the second half of 2008, when economic activity in the US is likely to pick up significantly in response to the planned fiscal stimulus and past rate cuts, according to Chadha.

Whether or not the dollar will rebound in the second half will depend on a recovery in the US economy, which Deutsche Bank economists are forecasting, Chadha says. By making such a forecast, the bank’s economists are implying that the recession will be mild and brief, he notes. A necessary condition for such a forecast to be realized, he adds, is some amelioration in US credit-market conditions.

Focus on Systemic Risk

Market participants have grown increasingly fixated on the systemic risk involved in the current crisis, such as sharp declines in credit liquidity, problems at banks and brokerages, and coordinated operations by central banks to boost liquidity, says Ashraf Laidi, chief foreign exchange strategist at CMB Markets US, based in New York. These events related to systemic risk have overshadowed the emerging weakness on the macroeconomic front, he says.

As the liquidity storm is calmed, market participants will tend to have a false sense of comfort, Laidi says. They will confound the avoidance of disaster with notions that the worst is behind us, he says. “The fallout on the consumer will be particularly punishing, as the combination of record-high fuel prices, rising unemployment, negative home equity and restricted access to credit play out,” he says.

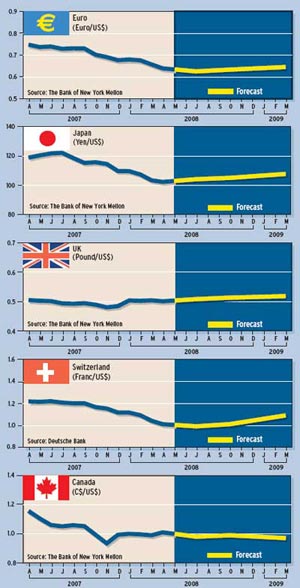

The British pound may be the least-favored currency among the G-10 currencies besides the US dollar, Laidi says. The pound hit a record low of 79.73 pence against the euro on March 31, after UK housing prices dropped in March for a sixth month in a row. Meanwhile, the United Kingdom’s high interest rates suggest that Britain has the biggest room for cuts in rates among the industrialized nations, considering the pace of declines in housing and the implications for the highly leveraged UK consumer, Laidi says.

The Confederation of British Industry, Britain’s top business lobby group, downgraded its growth forecasts for the UK economy to 1.8% for this year, saying that the credit crunch will continue well into 2009, despite easing from the Bank of England.

The fact that the euro is setting record highs against the pound as well as against the dollar is more telling of the euro’s short history than of an extreme in pricing, says Marc Chandler, global head of currency strategy at Brown Brothers Harriman, based in New York. Back in 1995 the pound was 12% lower against the old deutsche mark than where it is now trading against the euro, he says.

Capital Exporters Favored

In periods of heightened credit tensions, those countries, such as Japan and Switzerland, that are net exporters of capital tend to fare relatively better, Chandler says. At the same time, countries with current-account deficits are seen by market participants to be particularly vulnerable, he says. This was one of the factors that weighed on the Icelandic krona, which sold off in late March on a report of a major widening in Iceland’s trade deficit. The krona has been among the worst-performing currencies this year, losing 17% against the dollar and 25% against the euro in the first three months of 2008. Iceland is perceived to be vulnerable because its current-account deficit is more than 15% of the country’s gross domestic product, Chandler says.

“The need for external financing is particularly precarious given the risk aversion so prevalent in the global capital markets,” Chandler says. “That said, the krona began cracking a year ago, months before the credit crisis emerged in its full glory,” he adds.

Meanwhile, the economic news from Japan is not supportive of the yen, and its relative resilience appears to be a function of external developments, such as general risk aversion, Chandler says. There should be no mistake about it: The Japanese economy is weakening, as the government has acknowledged, he says.

Tankan Takes a Tumble

The yen fell sharply on April 1, after the tankan business sentiment survey dropped to a four-year low in the first quarter of 2008. Japanese business leaders said they were worried about the weak US economy, the strong yen and high oil prices.

The Japanese economy is heading toward recession, observes Carl Weinberg, chief economist at High Frequency Economics, based in Valhalla, New York. “Now for the really bad news,” he says. “We do not see any policy options here.” Japanese interest rates are already at a low 0.5%, leaving little room if any for the Bank of Japan to ease, he notes. Fiscal policy is not available for economic stimulus either, he points out, as the government budget deficit threatens to run amok in the next three years. “The government also has no viable options for currency intervention,” he adds. “So the outlook is grim.”

The yen will continue to rise as de-leveraging hedge funds close out carry trades, according to Weinberg. Such trades involve borrowing in yen and investing in higher-yielding currencies. As the yen rises, this will quash foreign demand for Japanese goods and cut into profits at the big manufacturing companies that told tankan pollsters they already are miserable, he says. “Flat wages will translate into further declines in domestic private demand,” he predicts.

Decoupling Debate

A key question for the foreign exchange markets is the extent to which the rest of the world can decouple from the ongoing US problems, according to a report by analysts at Barclays Capital, based in London. The resolution of this issue will have implications for a range of currencies, particularly the dollar, which should appreciate if the economies of the rest of the world begin to slow more sharply, the report says. The currencies whose fortunes are closely linked to commodities prices should also decline under such a scenario of global economic slowing, it says.

According to Barclays Capital, evidence of a “recoupling” could begin to emerge during the second half of 2008, led by signs of a slowdown in China and India. “In the case of China, we expect the impact of the export slowdown, the negative impact on real disposable income from the sharp increase in food prices, and the 40% slide in the local stock market since last August to soon become apparent,” the report says. “For India, we expect high interest rates and moderating external finance to act as headwinds for the economy,” it adds.

The ability of emerging market economies to cope with the negative impact of the recent surge in food prices has introduced a new angle in the decoupling/recoupling argument that may eventually tip the balance of the debate, the report says. So far, however, the data have strongly supported the decoupling argument, the report acknowledges. Germany’s economy appears to be getting support from domestic demand, for example. And while Japan’s exports declined in February on a seasonally adjusted basis, the unadjusted data show that export growth is being supported by strong growth in exports to Asia and Europe.

Dollar Still Vulnerable

“Arguably the biggest surprise in the first quarter of 2008 was the continued resilience of the global economy despite the US slowdown,” according to the report by Barclays Capital. Although the Fed is probably approaching the end of its easing cycle, which ultimately will boost the dollar, the combination of negative US real interest rates and a large US current account deficit leaves the dollar vulnerable to further bad news in the short run, the report says.

The continued ability of emerging market economies to support global demand for tradable goods holds the key to whether the eurozone’s decoupling from the US slowdown and the surprising strength of commodity currencies will continue, Barclays Capital says.

Steven Wieting, managing director of economic and market analysis at Citi, says that for consumers in emerging markets food and energy prices represent roughly one-third of their consumer basket compared to less than one-fourth of outlays for the US consumer. “As such, rapid food-price gains witnessed recently provide a brake on even rapidly rising incomes,” he says. “Ultimately, the combination of slowing exports to the US, tighter financial conditions and a far-from-seamless rise in energy and food producer incomes provide a basis for slowing [economic growth] abroad as well,” he says.

The International Monetary Fund cut its forecast for 2008 global growth again to 3.7% from the 4.1% growth it forecast in January and the 5.2% growth rate it forecast in July 2007. It says growth in the global economy is losing momentum as a result of the financial crisis in the US.

Gordon Platt