More mergers in the mining industry are likely in 2008, analysts say, including potentially some of the biggest M&A; deals ever.

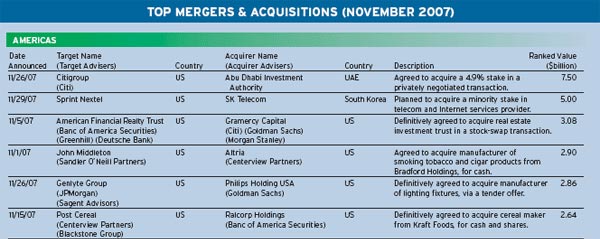

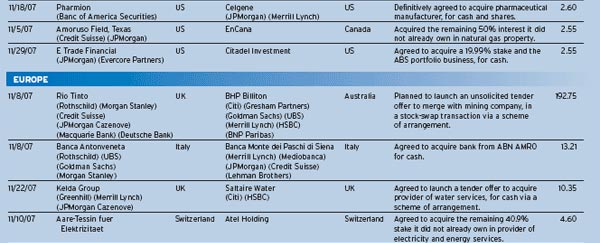

Australia-based mining company BHP Billiton in November announced plans to launch an unsolicited tender offer to merge with UK-based Rio Tinto in a stock-swap transaction for which Thomson Financial gave a rank value of $192.75 billion. The proposed merger between the world’s number-one and number-three mining groups came as Rio Tinto itself was wrapping up its acquisition of Canada-based Alcan in a deal valued at $38.1 billion that would create the world’s largest aluminum producer.

There were more deals in the metals and mining sector in 2007 than ever before, as metals prices soared on rising demand from China and other emerging market countries. Standard & Poor’s Ratings Services says it expects BHP Billiton’s bid for Rio Tinto to spur further consolidation in the industry. The rating agency warns that mergers could trigger potential downgrades if they are financed with large amounts of debt.

At least three more transactions totaling more than $50 billion are likely by June, Ernst & Young’s partner in charge of global mining and metals, Michael Lynch-Bell, told a conference in London in November. It is easier for mining companies to acquire new reserves through acquisitions than via exploration and production in ever-more-remote areas of the world.

At least three more transactions totaling more than $50 billion are likely by June, Ernst & Young’s partner in charge of global mining and metals, Michael Lynch-Bell, told a conference in London in November. It is easier for mining companies to acquire new reserves through acquisitions than via exploration and production in ever-more-remote areas of the world.

“Smaller companies that are still exploring or developing mining projects are finding it much more difficult than usual to get access to finance,” Lynch-Bell says. The trend for major producers to acquire smaller mining companies is likely to continue, he predicts.

“It is very rare for a small mining or exploration company to go from obtaining an exploration license all the way through to production,” Lynch-Bell says. “The mining industry has always historically grown by acquisition; it’s nothing unusual and is seen by many boards and their shareholders as a sign of success.”

Rio Tinto rejected BHP Billiton’s proposed all-share offer shortly after it was announced, saying that it tremendously undervalued the company. But as Global Finance went to press, BHP was persevering with its approach. BHP chief executive Marius Kloppers sweetened the appeal for Rio Tinto’s shareholders, who would own 41% of the combined company, by proposing a $30 billion share buyback if the deal goes through.

The merger would have to pass muster of competition authorities. The European Confederation of Iron and Steel Industries, or Eurofer, already has claimed that the proposed combination would create an even greater monopoly of iron ore.

China’s sovereign wealth fund is expected to become more active in buying shares in metals and resources companies, considering the country’s growing need for raw materials, analysts say. Russian companies, such as Norilsk Nickel and Rusal, also are likely to participate in the ongoing consolidation in the industry. Rusal, Russia’s largest aluminum producer, merged with smaller rival Sual along with Switzerland-based commodity trader Glencore International in 2006. Rusal said the merger would solve the problem of the historic lack of available bauxites and alumina in Russia. Glencore contributed its alumina-refining assets to the new company.

Mining mergers will be welcomed by investment bankers, who are suffering a decline in deal value as a result of fallout from the subprime crisis and credit crunch. The value of announced US mergers and acquisitions fell 71% in November from the same month a year earlier, according to Dealogic.