Corporate Debt

A growing US economy will lead to rising interest rates and a more challenging climate for bond issuance in 2005, according to the Bond Market Association.

Total US bond issuance is expected to fall 15% this year, with the sharpest decline in the mortgage securities market, the association forecasts, based on a survey of member firms that was conducted in December.

Corporate borrowers took advantage of the low interest-rate environment of the past few years to issue new bonds and restructure existing debt. But as rates rise and corporate balance sheets improve, companies are expected to explore alternative sources of funding, such as issuing equity, the association says. After strong internally generated cash flows over the past year, the cash position of many corporations is significantly stronger, it says.

Nonetheless, certain high-yield segments of the corporate bond market may continue to experience higher issuance this year, as lower-rated companies continue to benefit from relatively low funding costs in a period of tight credit spreads, it adds.

“Moderate short-term interest rate increases over the past year have had a predicted effect on overall issuance and will continue to influence issuance in 2005,” says Micah Green, president of the association.

“The bond markets remain robust, however, and 2005 should be a solid year, reflecting financing needs generated by a growing economy,” Green says.

The credit markets are gaining strength and will remain strong in 2005, says Glen McDermott, director and global head of CDO research at Citigroup. “Spreads are tight relative to historical norms, but default rates are low and are expected to stay low,” he says. “Dont look for spreads to widen soon.”

Despite the tight spreads, investors are being adequately compensated for risk in a benign credit environment, McDermott says. Trading in collateralized debt obligations doubled in 2004 and will remain at least as high this year as investors continue to search for yield, he notes.

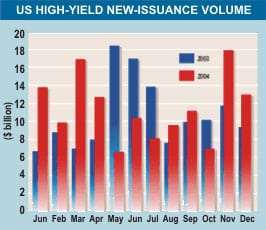

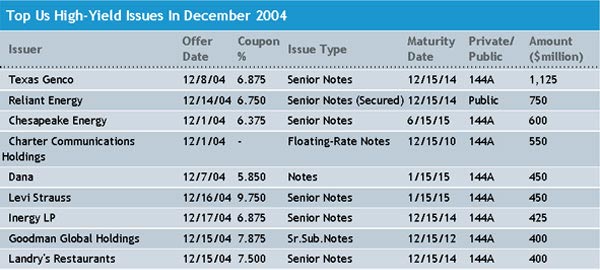

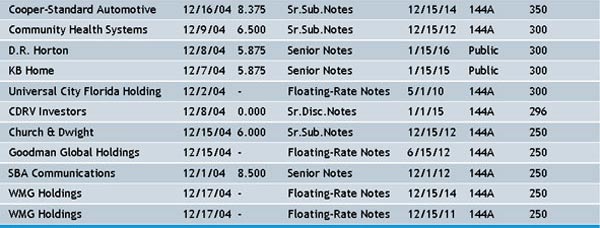

Total US issuance of high-yield corporate debt fell to about $13 billion in December from $18 billion in November.

Gordon Platt