Foreign Exchange

Japans trade surplus and the weakness of the yen were not singled out, however, when the G-7 finance officials met in London in early December. The low level of concern by G-7 officials about the yens weakness encouraged further yen selling.

Is yen weakness a one-way street? Or will the US and other G-7 countries pressure Japan at some point to stop allowing the yen to decline? Analysts say the outlook remains bearish for the yen, particularly since Japanese officials appear satisfied that a weaker currency may boost profits of Japans exporters and has helped the Nikkei stock average climb to a five-year high.

Japanese finance minister Sadakazu Tanigaki told reporters at the G-7 meeting that the 15% decline in the yen between January and early December 2005 reflects relative economic performance. Bank of Japan governor Toshihiko Fukui said the protracted weakness of the yen was not a problem. He said movements in the exchange rate were not inconsistent with Japans economic policy of achieving sustainable economic growth and price stability.

US treasury secretary John Snow went out of his way at the London gathering of the G-7 to deny that he had voiced concerns about the steep drop in the value of the yen.

There was some coverage that I heard about statements that I didnt make, Snow said, scotching reports that the falling yen would be a topic of discussion at the meeting. He added that he was pleased that the G-7 communiqu stated that further flexible implementation of Chinas currency system would improve the functioning and stability of the global economy.

Despite the US hands-off policy on the falling yen, US automakers will have issue with the weakness of the yen, as will the National Association of Manufacturers, says Robert Lynch, head of Group of 10 foreign exchange strategy-Americas at HSBC Bank (USA) in New York. To the extent that the White House takes those views and acts on them is a completely different story, he says.

It is true that the decline of the yen puts China at a competitive disadvantage with Japan, Lynch says. And the trend toward a weaker yen has occurred despite renewed G-7 calls for more flexibility in Chinas currency, he says.

If the yen were to fall far enough, or if the decline is steep enough, intervention by the Bank of Japan is a possibility, Lynch says. The Bank of Japan could explain such a move by saying it was acting to counter volatility or to reintroduce two-way risk in the market, he says. Japan has not intervened to support the yen since 1998, and the last time it entered the market to sell the currency was in March 2004.

Even though, on a trade-weighted basis, the yen is at its lowest level since October 1985, Japanese officials are unconcerned, says Marc Chandler, global head of currency strategy at Brown Brothers Harriman in New York. And if officials are unconcerned, then investors and speculators do not need to be concerned, he says. The market is continuing to bet heavily against the yen, he notes, judging by the high level of short positions in yen futures contracts.

Meanwhile, the US Treasury declined to name China as a manipulator of its currency, when it released its long-delayed report to Congress on currency practices of major US trading partners. Chinas decision last July to abandon its peg of the yuan to the dollar and to revalue by 2.1% was its saving grace in the eyes of the Treasury, says David Gilmore, economist and partner at FX Analytics, based in Essex, Connecticut. But the verdict also left China very much on parole, with the Treasury noting that failure to do a lot more soon will result in a guilty verdict in the next report due in mid-April, Gilmore says.

China is not only up against the Bush administration over its manipulation of the yuan, but it is also very much up against Congress, which is eager to move on passing legislation slapping duties on imports from China unless China lets the market set the value of the yuan, Gilmore adds.

The Treasury has indicated that President Bush will veto protectionist bills passed by Congress. But ahead of a key mid-term election in November 2006, overriding a presidential veto is more than plausible, especially in light of a president depleted of political capital, Gilmore says.

Meanwhile, China continues to move at its own pace to bring more flexibility to the market. It took another step in late November, with the Peoples Bank of China carrying out its first currency-swap deals with local banks. Whats more, the State Administration for Foreign Exchange, or SAFE, also invited banks to apply to become market makers for spot yuan trading. SAFE didnt say when such trading would be introduced.

Analysts say the dollar remains strong on the basis of positive growth- and interest-rate differentials with Europe and Japan, despite the European Central Banks quarter-point rate increase in December.

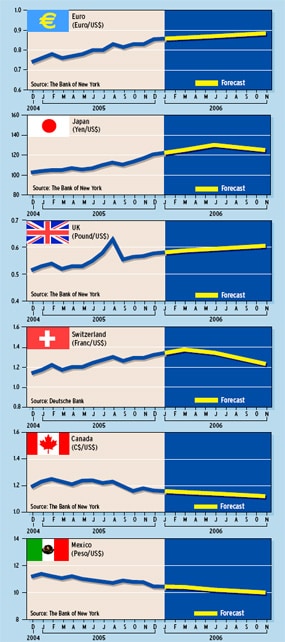

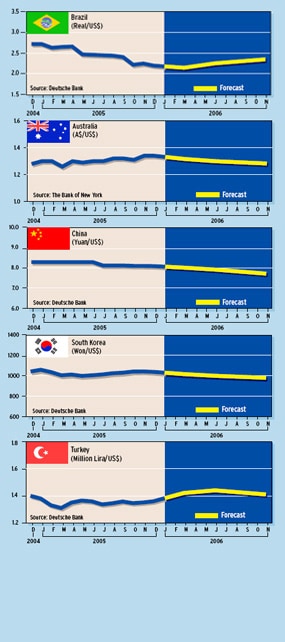

Currency Forecasts

Gordon Platt