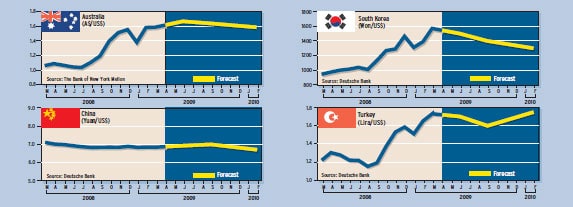

DOLLAR STAYS STRONG, BUT YEN TUMBLES

The US dollar index, a measure of the value of the dollar against a basket of currencies, rose to a three-year high in March, as investors continued to seek the safe haven of US treasury securities.

The US dollar index, a measure of the value of the dollar against a basket of currencies, rose to a three-year high in March, as investors continued to seek the safe haven of US treasury securities.“The decline of the yen in recent weeks is the most dramatic development among the major currencies,” says Marc Chandler, global head of currency strategy at New York-based Brown Brothers Harriman. “Previously, and frustratingly for Japanese officials and businesses, the yen was the strongest currency.”

On a trade-weighted basis, the yen appreciated by 35% from last summer through late January 2009. “This is an exchange-rate shock of incredible proportions,” Chandler says. In January Japanese exports were almost 46% lower than in January 2008. Japan’s current account swung into deficit in January 2009 for the first time since 1996.

“The good news is that the yen’s bubble appears to have popped,” Chandler says. As was the case with the onset of the financial crisis itself, few could envision the end of the yen’s advance, he says. “Yet it has happened and without a clear cause.”

While some analysts blame the yen’s turnabout on the release of a report showing that Japan’s gross domestic product contracted at a rate of 12.7% in the fourth quarter of 2008, Chandler says the report was

released on February 15, three weeks after the dollar and euro had already bottomed against the yen.

released on February 15, three weeks after the dollar and euro had already bottomed against the yen.Japan’s economy is now in tatters, and its recession is worsening, although the country did not appear to have the excesses in housing that occurred in the US and the UK. Nor did it have the leveraged-loan portfolio and emerging market exposure of many continental European economies, according to Chandler. Nevertheless, the Japanese economy has been the hardest hit, he says.

“Japan’s exports have simply and unsurprisingly collapsed amid the synchronized contractions of the major economies,” Chandler says. Meanwhile, domestic demand is also poor, wages are falling, and Japanese politics are in shambles, he adds. The government’s modest fiscal stimulus measures have been stymied by the Democratic Party of Japan, which controls the upper house of the Diet.

In one of its few innovative measures, the Japanese government has decided to tap its reserves to provide $5 billion to the Japan Bank for International Cooperation to help provide financing for Japanese multinational companies. Japan has nearly $1 trillion of reserves, which traditionally are meant to protect a country from an import surge or a dramatic decline in exports, which is precisely what Japan is experiencing, Chandler explains. “What, pray tell, are the officials waiting for?” he asks.

The $5 billion the Bank of Japan will lend out is not even equivalent to the interest on its reserves, Chandler says. “This timidity warns that the economic downturn in Japan will be deeper and more protracted than expected,” he says.

As the global economic crisis continues to unfold and broaden, it has been hard to find a currency that can do well, says Paul Brain, investment leader of fixed income at London-based Newton Investment Management, a subsidiary of The Bank of New York Mellon. “Rather than looking for currencies that will shine, we are forced to judge a ‘least ugly’ contest,” he says.

Global growth collapsed in the fourth quarter of 2008 and is set to be equally weak in the first half of 2009, Brain says. “In the yen, we now have an ugly-currency contender, and we are looking for less ugly currencies into which to switch,” he says.

The Norwegian krone is one candidate that seems less ugly than the rest, Brain says, since Norway’s large sovereign wealth fund gives its economy major support. Last year the Norwegian economy was vulnerable to the decline in the oil price, but since December the oil price seems to have found a floor, according to Brain.

“We have also increased our exposure to the Australian dollar, although the positives are not as compelling,” Brain says. “Following the boom years of the commodity cycle, the Australian government is in the enviable position of entering this crisis with a very low debt-to-GDP ratio.”

The tide is turning against the yen owing to the significant damage done to the Japanese economy, Brain says. “The deleveraging story keeps us out of emerging market currencies for now, as the shift toward domestically focused policies continues,” he adds.

The US dollar has remained one of the strongest currencies this year, even though the US budget deficit is expected to grow by more than 12% this year. David Gilmore, economist and partner at Essex, Connecticut-based Foreign Exchange Analytics, asks, “Can the US Treasury fund a $787 billion stimulus on top of a $600 billion budget shortfall without a bond [market] and dollar rout?” The answer, he says, is “yes” for the foreseeable future.

“We are in the midst of a global ugly contest,” Gilmore says. “Every major economy and policymaker will be where the Federal Reserve and US Treasury are,” he says. And based on the collapse in global trade, including industrial production in Europe and Japan, this will happen much faster than anyone would have imagined just a few months ago, he says.

Every major economy in the world is heading toward zero interest rates and large fiscal stimuli, Gilmore says. The US has a head start on this policy mix, which will also give it a head start in getting out of this mix in the medium term, he says.

The US savings rate is rising rapidly as households and firms stop spending and investing in response to economic fears and declining asset prices, Gilmore says. Fear also permeates portfolio preferences, and this favors US treasury securities. “My hunch is that even very bad policy mistakes—and there will be more ahead—will take a far longer time to trigger a funding problem for the US government than they would for, say, Argentina or Britain,” he suggests.

Every prior economic and political crisis in the US was met with cries to halt the printing presses or run the nation into ruin, Gilmore says. And these crises were all followed by periods of technological innovation, productivity enhancements and a much larger private sector, reducing debt-to-GDP ratios substantially, he notes.

—Gordon Platt