FOREIGN EXCHANGE

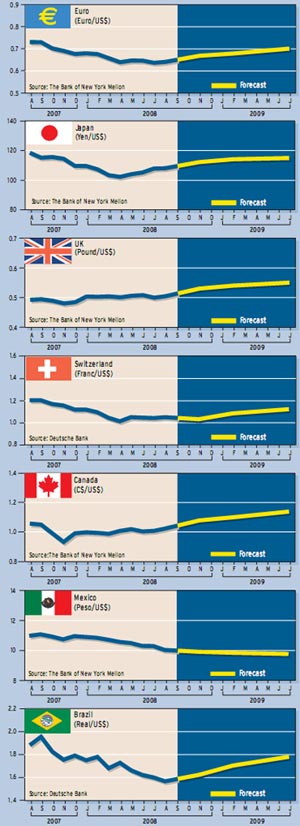

The dollar made strong and broad gains last month as commodity prices declined and economic data from Europe and Japan came in weaker than expected. Early signs of a global slowdown in real economic activity and falling oil prices could indicate that the dollar has hit bottom against the euro and the yen, although some emerging market currencies will remain buoyant, analysts say.

The weakest readings for the global economy are still to come, says Steven Wieting, managing director of economic and market analysis at Citi global markets in New York. “In the developed world, the US downturn began first and is the most advanced, and countercyclical policies have been the most pronounced,” he says. “We expect 2009’s US growth rate to exceed the euro area’s and Japan’s.”

Citi’s 2009 estimate for growth in gross domestic product (GDP) for the United States is 1.4%; for the euro area it is 0.7%, and for Japan, 0.8%.

With the US economy expected to grow the fastest and with oil prices potentially more stable in 2009, the six-year-long decline in the dollar’s exchange rate against the developed countries is likely to run its course this year, according to Wieting. “It is possible that oil price declines and dollar strength could be jointly reinforcing in the year ahead,” he says.

With the US economy expected to grow the fastest and with oil prices potentially more stable in 2009, the six-year-long decline in the dollar’s exchange rate against the developed countries is likely to run its course this year, according to Wieting. “It is possible that oil price declines and dollar strength could be jointly reinforcing in the year ahead,” he says.

While evidence of slower growth in emerging markets is also building, the data are more volatile or not yet available, the Citi economist says. However, weaker trade flows, particularly to the US, are showing up in slower Asian production growth rates. Citi economists forecast the overall growth rate for emerging markets in 2009 to slow to 6.1% from 6.3% in 2008 and 7.4% in 2007.

Michael Woolfolk, senior currency strategist at The Bank of New York Mellon, says the dollar is benefiting not only from weakening growth expectations overseas but also from strengthening growth expectations at home. “While the United States has won the battle of the growth expectations for now, opinions in the market are deeply divided over the way in which central banks will respond to the continued rise in inflationary pressures,” he says.

“If the United States ends up winning the battle of the interest rate differentials, with the Federal Reserve lifting rates sooner than expected, the greenback has far more upside potential than many expect,” according to Woolfolk.

With US disposable income growing at a healthy pace, personal income and spending appear more robust than recent lows in consumer confidence suggest, Woolfolk says. Consumers are spending a larger proportion of their disposable income at the gas pump, and rising inflation is eroding their real income, but the surprise is that consumers have held up as well as they have under the pressure, he says.

“The US economy is not buckling under to the degree many expected,” Woolfolk says. “While US second-quarter GDP came in slightly below expectations, it was well above recessionary territory at 1.9%.”

Marc Chandler, global head of currency strategy at Brown Brothers Harriman in New York, says the dollar hit bottom against half of the currencies of the Group of Seven industrialized nations in November 2007 and against the yen in March 2008. He says the dollar has also bottomed out against a number of emerging market currencies. “Yet the dollar continues to bounce along its trough,” he says. “It may be difficult for the dollar’s base to broaden further to include the euro until investors have greater conviction that interest rate differentials are going to move in the US direction,” he adds.

The foreign exchange market likely will continue to be driven by other markets, such as oil, equities and the general perception of systemic risk, according to Chandler. “As the world breathed a collective sigh of relief [after the US treasury committed itself to prevent the collapse of Fannie Mae and Freddie Mac], the equities markets roared back, and the dollar found better footing,” he says.

The actual status of government-sponsored agencies relative to the government’s obligations to support them has always been murky, Chandler says. “Once again, US policymakers demonstrated willingness and capability to innovate,” he says.

Meanwhile, the long-term decline in the dollar is encouraging foreign direct investment (FDI) in the US, Chandler says. “The decline in the dollar not only makes the US relatively cheap, but when coupled with the gains in productivity, the US has lower unit labor costs vis-à-vis most of the other major industrialized countries,” he says. Foreign companies are locating more production and sourcing in the US. Volkswagen, Europe’s largest automaker, recently announced plans to resume production in the US for the first time in two decades.

FDI in the US rose by roughly two-thirds last year to $277 billion, the highest since 2000, according to Chandler. Most of the rise came in the form of new acquisitions, but more than 25% came from expanding existing US operations.

While sustained FDI inflows could support the dollar, the latest budget forecasts from the US Council of Economic Advisers (CEA) are a stark reminder of the dollar’s structural weaknesses, says Ashraf Laidi, chief foreign exchange strategist at CMC Markets (US) in New York. The CEA projects a record-high deficit of $482 billion in fiscal 2009.

“Higher US interest rates would be required to maintain foreign flows into the US,” Laidi says. “But if the twin deficits [budget and current account] surge anew and US interest rates remain at current levels, or fall further, this would be a distasteful recipe for the dollar,” he says.

The dollar’s rise last month to a six-month high against the euro is no reflection of increased hawkishness by the Federal Reserve, which has modestly downgraded its assessment of the US economy, Laidi says.

David Gilmore, partner and economist at Foreign Exchange Analytics, based in Essex, Connecticut, says the idea that the Fed is debating when to raise rates is fanciful. The financial crisis of the past 12 months is merging with a consumer-led economic crisis and will make for a very hard landing for the US economy, he says.

“The consumer is not going to be resurrected by $100-a-barrel oil,” Gilmore says. “When oil really starts to unravel, it will be because the economy is unraveling.”

Gordon Platt