Traditional banks and upstart challengers alike are pushing innovations to create the bank of the future. What might such a bank look like?

QIB headquarters |

From the creation of the first banks during the Middle Ages through the late 20th century, the greatest virtues in finance included stability, security, wealth and trust. Those principles were visible in bank buildings: solid, hulking constructions of impassive stone that said to clients, “We’ve got lots of money, and yours will be safe here.”

As finance modernized, bank architecture moved with it. Headquarters became more imaginative—like the airborne “boat” of ING Group headquarters in Amsterdam, completed in 2002; or the glossy, curvy towers of Qatar International Islamic Bank, completed in 2014. They denote not only financial power and security, but the very modern value of innovation.

The bank of the future probably won’t look like this at all. Its critical architecture will be built on ones and zeros, quietly inhabiting technology tools, not “bricks and mortar.” Those ones and zeros will be transmitted from machine to machine—no need for a vault in the basement.

Given the much-touted advances in artificial intelligence (AI) and robo-advisory, the bank of the future could even, conceivably, be led by a robot CEO. “[The bank of the future] will be AI-driven,” says Sitoyo Lopokoiyit, director of financial services at Safaricom, which launched one of the first mobile money-transfer services in Africa, M-Pesa. “The key [technologies] will be the smartphone, machine learning, AI, Big Data, robotics and chatbots.”

Today, M-Pesa is joined by plenty of other upstarts in finance, called “challenger banks” or “neobanks” (a subgroup that is digital only, with no legacy IT). They are seeking to woo business from traditional banks. And there is a rising challenge from mammoth interlopers from other sectors, like Apple, Google, Alibaba and Tencent.

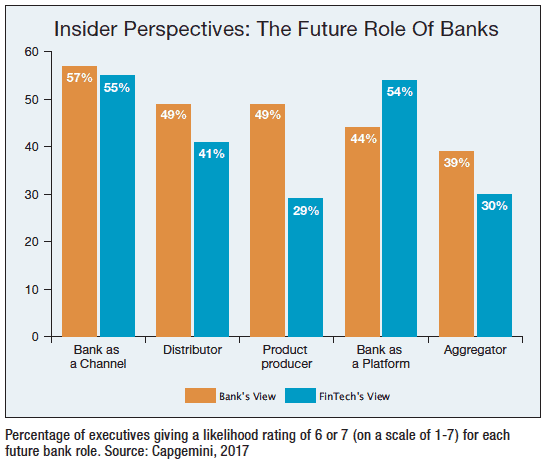

This new generation of banks—platforms or ecosystems, whatever you call them—are making transactions easier, faster and more transparent. They are literally plugging in different financial products (investments, savings, mortgages, currencies, cards, payments and lending) from a range of different third-party providers, to build the bank of the future.

“You can now build a new bank in six months, using technology from fintechs [companies that specialize in financial technology],” says Raj Rajgopal, president of business consultancy firm Virtusa’s Digital Strategy Group and head of Virtusa’s China Insights Group.

This sea change in finance is driven by technology, which is both expanding service capabilities and reshaping client expectations. Additional pressure comes from governments, which are pressing for “open banking” through vehicles such as the EU’s Payment Services Directives (1 and 2). UK regulators fully embraced the spirit of PSD1, which paved the way for nonbanks to enter the payments market traditionally owned by the incumbent banks; and PSD2, which was drafted into law in January. As a result, the UK has the largest number of challenger banks in Europe.

With all these new emerging models for banking, Charles Kie, managing director and CEO of Ecobank Nigeria, says compliance—know-your-customer and anti–money-laundering regulations—will be more important than ever. Traditional banks still see themselves as fortresses for client assets and may equate open banking with less security. Yet the neobanks that use the most up-to-date tech claim an advantage; for them, the security of customer data has been factored in from day one, not added later.

Open banking is absolutely a worldwide trend. “It exists in China with Alipay and in Africa with M-Pesa. In India, it’s a fight between Whatsapp and Google for payments,” says Edward Maslaveckas, co-founder of Bud, a London-based technology platform that works with banks. “In the US, it will happen in a different way.” Even in markets like Brazil, where it is not easy for new entrants to obtain a banking license, there are neobanks like Banco Original and Nubank, and a community of more than 200 fintechs.

Less-developed parts of the world have even leapfrogged more-developed nations in mobile services. In fact, Liz Lumley, global fintech commentator and advisor, and former managing director of the 2015 Startupbootcamp Fintech London Accelerator Program, goes so far as to say, “Asia and Africa have the advantage.”

Liz Lumley, fintech specialist: Asia and Africa have the advantage. |

A huge part of the story is the rise of fintechs, which are encroaching on space traditionally occupied by bankers. Yet most challenger banks can only dream of reaching a big-bank customer base. Starling has tens of thousands of customers; N26, a leading mobile bank in Europe, has 850,000; Revolut has 1.5 million. Traditional banks number their customers in the tens of millions: Deutsche Bank (30 million), HSBC (38 million), or Bank of America (57 million).

Another huge new competitive factor is the encroachment of tech firms into finance. In the US, many predict that the bank of the future will arise at one or more of its tech giants, such as Google, Apple, Facebook or Amazon (GAFA). They already offer payment solutions (e.g., Amazon Pay and Google Pay) with massive customer bases—Amazon claims an active user base of some 250 million around the world. ApplePay had 127 million users worldwide at the end of 2017, and has been cutting deals with banks—including Chase, Citi, and Wells Fargo—for a piece (reportedly 0.15%) of each purchase made with an ApplePay app. The company explicitly aims to make ApplePay its customers’ primary payment system.

“Banking is not that far a leap for the GAFAs,” says Lumley. “If you’re playing Taylor Swift’s latest hits on the Amazon Alexa [voice-activated assistant], the next step is probably, ‘Alexa, buy this album’; and then it’s not long before you’re saying, ‘Alexa remortgage my house.’”

At the same time, legacy banks are not resting on their laurels. Another part of the story is the adaptations of traditional banks, embracing innovation and partnerships. Challenger banks claim to have a better understanding of consumers, while established banks boast solid customer bases and plenty of financial muscle. “Incumbent banks will have to work hard to remain relevant,” says Ewan Macleod, chief digital officer at Nordea Bank in Denmark, “but there are questions for the challenger banks around reliance and trust.” The banks that win the future will combine the best of both World’s.

The Challenge

What do neobanks offer that gives them an edge over incumbent banks? For one thing, according to KPMG, challengers offer better savings rates than traditional banks. Neobanks also tout their ease of use, customer focus and lack of legacy IT.

Consider Starling Bank, which started life in 2014 in the UK. Starling has a banking license, so it accepts customer deposits, lends money, makes money on interchange fees and is connected to the main UK electronic-payment systems. But it has no physical branches.

“The user experience is entirely different,” says Megan Caywood, co-founder and chief platform officer at Starling. “It takes five minutes to set up a bank account, whereas with traditional banks that experience is clunky. If you do two or three transactions, it shows up in real time with the merchant’s logo, so you know what it is for.”

Megan Caywood: The user experience with a neobank is entirely different. |

Starling has also set up a marketplace for mortgages, investments and travel insurance provided by third parties. “The marketplace is entirely different from what traditional banks do,” explains Caywood. “It’s like an app store for financial products.”

Starling uses Amazon Web Services and Google Cloud Services, “which is a very low-cost model,” says Caywood. According to KPMG, neobanks have lower costs as a percentage of income and a higher return on equity than the UK’s traditional banks. No wonder incumbents like RBS, Santander and BBVA are looking to set up separate “digital-only” banks.

But challengers believe their customer insight is qualitatively different from even the best banks’ service. “I don’t see traditional banks catching up,” says Valentin Stalf, founder and CEO of European mobile bank N26. “They may be investing billions in digital apps, and may copy what fintechs are doing; but we’re building a digital community. That is something you cannot buy.”

Not everyone is fully convinced that the reality matches the promise. “What’s the game-changing experience that means you’re not competing with someone else?” asks Maslaveckas of Bud. “What is the Facebook of banking that supports the different types of lives that people lead?”

Mobile with the Customer

The bank of the future, it is widely assumed, will be able to maximize customer insight and revenue via Big Data analytics. For a glimpse of that future, look to China.

In China, mobile payments dwarf cash. They reached a whopping $8.6 trillion in 2016, according to eMarketer; and more than 90% of these payments were made using either Alipay, the payment arm of Ant Financial, which is owned by China’s largest ecommerce platform, Alibaba; or TenPay, an integrated payment platform launched by Chinese entertainment giant Tencent. Alibaba and Tencent also have banks: MyBank and WeBank, respectively.

Rajgopal, Virtusa: Alibaba and Tencent are creating the future of banking. |

“Alibaba and Tencent are creating the future of banking,” saysRajgopal of Virtusa. “All services in China will be consumed via them, which gives them access to valuable customer data. They know everything about you.”

The most visible manifestation of the change is the slow disappearance of cash in China. Even street vendors can be paid with a wave of the smartphone.

It’s a similar story in Africa, where the banking revolution is totally mobile and led, not by agile fintechs or wealthy tech giants, but by the telecoms. It started in Kenya in 2007, with M-Pesa, to help “unbanked” workers transfer money back home. Now M-Pesa is widely used to pay for utilities, restaurant meals and other purchases. Its latest innovation, M-Shwari, developed with Commercial Bank of Africa, allows M-Pesa users to borrow and save money via their mobile phone. “We’ve created a fintech bank that transcends anything,” says Lopokoiyit. “You can open an account without going to a branch and get credit without seeing a loan officer. Traditional banks can’t sell to the bottom of the pyramid; but with M-Shwari, CBA is making about 70,000 loans a day.”

The rise of mobile money in Africa, more particularly M-Pesa, was facilitated by the central bank in Kenya. In other parts of Africa, Nigeria for example, the central bank licenses banks, not telcos, to provide mobile money.

With customers, especially younger generations, expecting to do any transaction on their mobile phone, Ecobank Nigeria is using research for insight. Since more than 50% of Nigeria’s population is aged under 25, so Kie recently employed 400 graduates aged 18-23 to encourage the cross fertilization of ideas within the bank. They challenged him as to why they could not find him on Instagram. “You are how much you are liked [on social media],” he says. “We need to be part of that conversation.”

That generational divide is not unique to Africa. “I’m obsessed with the customer experience; the ability to switch a card on and off, without speaking to a call center,” says Nordea’s Macleod. “I’m enthusiastic about it, but my mother probably isn’t.”

Hutchinson, Standard Bank: The human changes required are often harder to achieve than the technology upgrade. |

Ecobank is also adapting, Kie lsays, by rethinking internal workflows to adapt to the new service approach. Tim Hutchinson, head of digital for Financial Markets at Standard Bank sees the same dynamic: “The human and cultural systems and client-behavior changes required to give this digital evolution life are often a lot harder to achieve than the technology upgrade.”

To support its growth, Ecobank recently announced a partnership with mobile operator MTN, which operates in 22 countries across Africa and the Middle East, to provide mobile financial products.

Kie sees a future in which consumers no longer access banking services via a bank account, but from social-media sites like Facebook or WhatsApp. “Where banks insert themselves into that will be a key challenge,” he says, “as it’s 180 degrees from where we are today.”

“The bank of the future will be inherently social and use intelligence to connect groups together. Customers will still need somewhere to go, but the opportunity is to create a Carphone Warehouse or Apple Store-like experience in banking that connects ecosystems,” ventures Maslaveckas. “For SMEs and corporates, it will be about creating better business-intelligence and financial-management tools using data so that they can better segment and distribute their products to customers.”

It will not be about just transacting, but also solving problems, says Stalf of N26: “[The bank of the future] is an app that you use multiple times a day, not only for financial products, but for a lot of the problems you need to solve,” he says. “Itwill give you access to the right mobile contract and make recommendations that make customers happier.” It will be “invisible” and frictionless and will take three taps to do anything, he adds.

And the humble bank branch? Will that be replaced by some virtual hangout for customers? “The branch is unlikely to disappear altogether,” says Maslaveckas, “but it will look a lot different.”