Seeking A New Paradigm

Emerging markets countries are unlikely to repeat the growth miracles of the past. But that doesn’t mean many won’t continue to outperform developed markets. Meantime, new definitions are arising to delineate these markets.

Emerging markets have been with us for more than a generation. Coined in 1981 by World Bank economist Antoine van Agtmael, the term “emerging markets” replaced descriptions such as “developing countries” or “third world,” which focused on these countries’ lack of development or importance (the first and second worlds were helmed by the US and Soviet Union). In contrast, “emerging markets” was optimistic: These were the next generation of global economic development.

The description found favor and was in common use by 2001, when Goldman Sachs chief economist Jim O’Neill came up with a nifty new moniker for the largest emerging markets—BRICs (for Brazil, Russia, India and China). Throughout this century’s first decade and beyond the financial crisis, the term emerging markets seemed to reflect a self-fulfilling prophecy—they were growing so fast that some observers speculated they could soon be described as “emerged.”

Now the BRIC countries are on different trajectories. China’s growth is slowing as it builds a consumer economy, Brazil is stagnating because of structural and infrastructural challenges, and Russia is focused on geopolitics rather than economics. Only India (after years as a laggard) is trying to reboot reform efforts to boost growth and modernize its economy. The divergence of the BRICs—and the slowdown of emerging markets’ growth—raises questions about the usefulness of “emerging markets” as a description for those countries that make up the majority of the world’s population. Moreover, it raises a further question: Is the halcyon period of emerging markets growth that ran from the 1990s to just after the financial crisis over for good? And how can we best differentiate the opportunities that do exist?

WHAT ARE EMERGING MARKETS?

To ascertain whether emerging markets is an obsolete term, we must first understand what it means. Emerging markets were defined not by common economic characteristics but as an investment opportunity, according to Benoit Anne, head of emerging markets strategy at Société Générale (SG). When the term first came into being, most investors looked only at developed markets; emerging markets as a category for investment was a differentiator from previous investment strategies, he explains.

But these newly-defined markets nevertheless had shared characteristics. When it came to foreign investment flows, “Emerging markets moved as a group,” says Maarten-Jan Bakkum, senior strategist “emerging markets” at ING Investment Management. “Global drivers—such as Chinese demand growth for raw materials, global trade growth and abundant global liquidity thanks to easy US monetary policy—dominated endogenous [domestic] drivers.”

Emerging markets also had a shared history, having come of age as the Cold War ended (creating a political vacuum that spurred experimentation) and globalization accelerated. Globalization enabled emerging markets countries to import capital, technology and knowledge and to export what they produced, notes Neil Shearing, chief emerging markets economist at independent research firm Capital Economics.

It prompted the widespread adoption of export-oriented industrialization, described as “history’s most certain path to riches” by Dani Rodrik, professor of social science at the Institute for Advanced Study (IAS), Princeton, and author of The Globalization Paradox: Democracy and the Future of the World Economy. Globalization also encouraged the formation of a loose consensus with economic and financial reform at its heart.

One important characteristic shared by most of the countries that have achieved emerging markets status over the past 30 years is the responsiveness of their governments—regardless of political creed—to demands from their populations. “People in emerging markets are poor and have no protection against inflation or economic instability,” says Jan Dehn, head of research at Ashmore Investment Management, which has $71.3 billion in funds under management. “They want improved living standards rather than ideology.” Local political accountability has resulted in economic stability and growth. While there have been plenty of market panics since 1998, “the fundamental strength of emerging markets has not been undermined,” says Dehn.

DIVERGENT PATHS

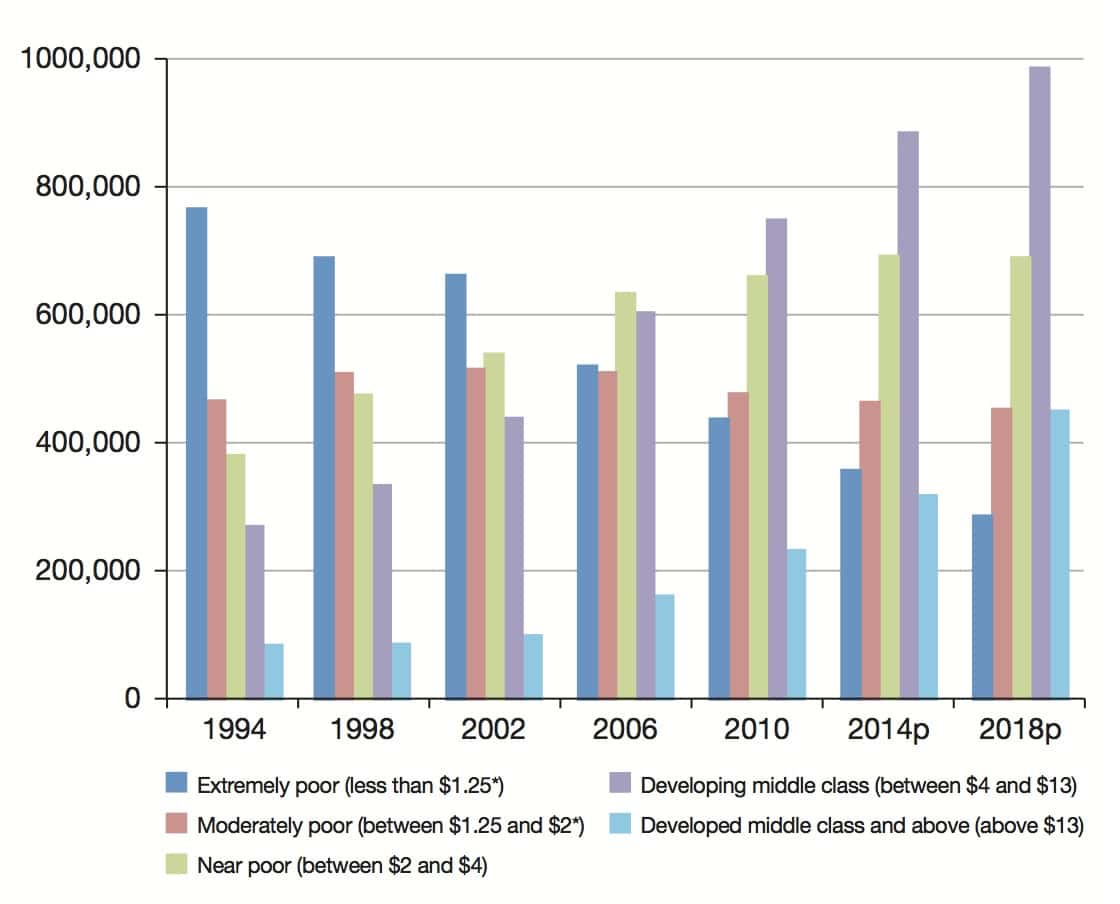

| RISE OF THE MIDDLE CLASS: EMPLOYMENT IN THE DEVELOPING WORLD, BY ECONOMIC CLASS (thousands of employed persons)  ** Wages are calculated per day, on a purchasing power parity basis; p = projected; ** Wages are calculated per day, on a purchasing power parity basis; p = projected;Source: International Labour Organization |

Although emerging markets have avoided a global crisis since 1998, their current prospects are underwhelming, compared with their prospects as of 10 or 15 years ago. This slowdown can be simply explained, according to Capital Economics’ Shearing: Many of the changes that drove growth from the 1980s onwards were one-off shifts. “Economies can never be opened up to foreign capital again, and communism can only come to an end once,” he notes.

Furthermore, the financial crisis and the slowing of growth globally, and particularly in China, have taken an inevitable toll. “Since 2010, Chinese growth has been slowing, putting pressure on commodity prices,” says ING Investment Management’s Bakkum. “And since 2013, markets have started to price the gradual normalization of US monetary policy, and thus capital flows into the emerging world [have slowed].”

The financial crisis and the fall in global growth also help to explain why emerging markets have started to diverge. According to the IMF’s World Economic Outlook, published in October, Brazil is expected to grow 1.4% in 2015, Russia just 0.5%, India 6.4% and China 7.1%. While the rising tide of global growth led by China lifted all boats, an ebbing tide has highlighted countries’ weaknesses, with a consequent impact on their growth rates.

Shearing says the financial crisis and its aftermath have revealed the BRICs’ different structural strains and constraints. For example, China needs to reverse its reliance on investment and switch to a consumption-based model of growth; Brazil must do the opposite; Russia should reduce direct control of its economy and increase industrial diversification; and India needs to free up its economy by improving infrastructure and reducing unnecessary controls.

In short, the shocks of recent years have exposed what some observers have always known—that emerging markets are not identical, although they share some characteristics and approaches to development. “Emerging markets have never been a homogenous group,” says Dehn. “They have been perceived as being one because of an investor mentality that divides countries into risk-free or risky categories.”

The slowdown in emerging markets growth and the BRICs’ economic divergence must be seen in perspective. First, growth in these markets still remains vastly superior to that in developed markets: The IMF predicts advanced economies will grow 1.8% in 2014 and 2.3% in 2015, while emerging markets will expand by 4.4% and 5%, respectively.

Second, the changes that took place in emerging markets from the 1980s onward had a profound effect that continues to be felt today. Those changes lifted hundreds of millions out of poverty and changed global economic and political dynamics. “Even when I worked at the IMF, from 2000 to 2005, [maintaining] the stability of emerging markets remained its major priority,” says Anne at SG. “Now that is no longer the case. Instead, the IMF’s priorities are often problems in developed countries.”

Political stability and policymaking within emerging markets countries has vastly improved. FX reserves were built up during the good times rather than squandered, for example. Dehn at Ashmore estimates that 80% of the world’s FX reserves are now held by emerging markets. Meanwhile, debt-to-GDP ratios in these markets are now around 30%, compared to 80% in the mid-1980s, and few countries have inflation problems.

“Emerging markets used to be a dirty word,” says Anne. “But the subprime and eurozone crises revealed such markets to be relatively solid. In the past, emerging markets experienced significant market volatility and concerns about political credibility. Now, the Australian dollar has greater volatility than many emerging markets’ currencies, while the eurozone crisis [has questioned that region’s] political credibility.”

WANTED: A NEW GROWTH MODEL

Although they cannot recreate the impact of one-off changes like market liberalization, emerging markets can find new ways to stimulate growth. “A fresh wave of reform is needed: Emerging markets need to go back to the 1980s,” says Shearing at Capital Economics.

A crucial question is whether the export-oriented model that drove emerging markets’ growth for 30 years is sustainable. For the countries that have advanced most in recent decades, the growth model has inevitably changed. “In many countries, a middle class is emerging and economies are becoming less export-focused and more inward-looking,” says Anne at SG. It remains to be seen if China can manage the switch smoothly.

Some observers question whether export-driven growth is viable for any emerging markets nowadays. “Manufacturing has become much more capital- and skill-intensive, with greatly diminished potential to absorb large amounts of labor from the countryside,” says the IAS’s Rodrik.

However, Shearing believes that “export-focused manufacturing still has a significant role to play in many emerging markets’ growth strategies.” And Anne holds that the experience of emerging markets in previous decades can be repeated in so-called frontier markets in Africa, for example. “They can also learn from the mistakes of the Asian tigers by [noting] that export competitiveness—and therefore exchange rate flexibility—is essential, as is production diversification,” he adds.

WHAT’S IN A NAME?

If the world accepts that emerging markets are heterogeneous, how then should they be categorized? Ashmore’s Dehn says that forthcoming gradual global financial tightening will separate countries that are forward-looking from those that are less adaptive to new conditions. “By far the most important factor in the success of countries in the medium term is whether their governments are prudent, flexible and smart enough to cope with shocks,” he explains. However, Dehn sees most emerging markets as forward-looking and believes the broad outperformance of emerging markets will continue: His “prudent” categorization doesn’t easily differentiate between emerging markets.

Shearing at Capital Economics suggests a categorization based on the type of reform required. Higher-income countries, such as those in much of Latin America, emerging Europe and richer countries in Asia, need to raise skills, education, research and development spending and productivity. In contrast, lower income countries, such as those in sub-Saharan Africa or parts of southeast Asia, need to get the basics right by opening up trade, simplifying tariffs and running prudent fiscal and monetary policies.

Alternatively, emerging markets can be grouped according to whether they have a current-account deficit—like Brazil, Turkey, South Africa and Indonesia—or a surplus, like China, the Gulf states or South Korea. “While Turkey is often viewed positively, the risk is that its borrowing is used to finance domestic demand rather than to improve its capital stock,” explains Shearing. “As quantitative easing is withdrawn and rates rise, it could become harder for the country to sustain its deficit.”

Another way of classifying countries is to divide them into commodity producers (or even further, into producers of agricultural commodities, energy or metals) and manufacturers. “Global trends, such as the shale gas revolution, affect different countries in different ways. Shale gas has cut oil exports from Nigeria to the US and led to a fall in oil prices,” says Shearing. “But it has benefited Chile, which is a huge energy importer and metals producer.”

Similarly, the end of China’s export boom has led to a fall in many commodity prices. “For commodity producers, the immediate future may be determined by what they have done with their commodity windfall from recent decades. Generally, Latin American countries have spent it, whereas Gulf states have saved it,” says Shearing.

Anne says that from an investment strategy perspective, emerging markets can also, most obviously, be grouped by region. “Asia remains a growth story and is expected to outperform; Latin America remains sensitive to the US economy; and EMEA has significant geopolitical risk—and CEE, vulnerability to the eurozone,” he notes.

The lack of consensus about how emerging markets should be categorized reflects broader uncertainty about the global economy. It presents investors with a challenge but also an opportunity. Many of the countries that currently fall under the emerging markets banner will continue to generate significant returns in the years to come. But not all will. Investors will have to be much more selective than they were in the past. n