Africa faces an uncertain future as its key economies suffer multiple setbacks and the global slump threatens to constrict the flow of investment.

By Paula L. Green

Being positioned on the fringes of a global economy navigating the worst economic downturn in 60 years is the good news for sub-Saharan Africa. It also is the continent’s bad news. “Sub-Saharan Africa has less of a cushion than other parts of the world. It’s closer to the edge, and there is no margin for safety,” says Murray Low, who teaches at Columbia Business School in New York City.

“The good news is that, without as much credit in their societies, they were not as significantly connected to the global financial crisis. The negative is that there had been an increase in private investment by private equity firms and risk capital. That will dry up,” says Low, who directs the school’s Eugene Lang Entrepreneurship Center.

Adds J. Stephen Morrison, a long-time expert on Africa and senior vice president at the Center for Strategic and International Studies (CSIS) in Washington, DC: “The upside of marginality is that when bad things happen to others, it’s not going to hurt you as much. But the weakest of these countries are in poor, fragile places…countries dependent on donor aid. The downturn is hitting them hard.”

As the overall global economy heads for a 1.7% contraction this year and the economies of the Organisation for Economic Co-operation and Development (OECD) face the prospect of a 3% decline, sub-Saharan Africa is still expected to grow, although much less than in 2008. According to the World Bank, the region will see economic growth of 2.3% in 2009—less than half the 4.9% increase of 2008 and 1.8 percentage points below earlier projections.

Those numbers compare with an expected drop of 2% in the gross domestic products (GDPs) of higher-income economies in Europe and Central Asia and a decline of 0.6% in Latin America and the Caribbean, down from gains of 4.3% last year, according to the World Bank’s recent Global Economic Prospects update. Shantayanan Devarajan, the bank’s chief economist for the Africa region, says the slowdown is causing declines in the continent’s traditional drivers of growth: foreign investment and commodity exports.

The worldwide decline in commodity prices has translated into a significant blow for a struggling continent dependent on exports of its natural resources—oil, metals and minerals such as copper, cobalt and iron ore, and precious gems such as diamonds—to fuel its growth and fill government coffers. Angola, for example, is a major oil exporter, and its nominal GDP is expected to fall by 17% this year, notes Devarajan.

While the oil-importing nations of Africa are benefiting from lower oil prices, they are also hurt by declines in global demand and value for their own commodities, such as coffee, cocoa and cotton. But it’s not only the precipitous drop in commodities that is threatening the hard-earned economic gains and higher living standards achieved by millions of Africans in recent years. The continent’s reliance on foreign direct investment (FDI), remittances and tourism, all spiraling downward during the global recession, is contributing to its growing economic fragility.

“The global financial and economic crisis is now becoming an employment crisis and in the coming months will become a human crisis for some. Africa has not escaped, with the first effects concentrated in sectors that are integrated with the global economy,” says Houtan Bassiri, a spokesperson for the International Finance Corporation’s sub-Saharan Africa group in Johannesburg, South Africa, in an email response. A member of the World Bank Group, the IFC helps finance private sector investment in developing countries and mobilizes capital in the international financial markets.

As anxious workers cancel holiday trips and multinationals curb business travel and conferences, the slump in tourism will hurt many African economies, such as the Seychelles. Located 1,000 miles off the eastern coast of Africa in the Indian Ocean, this archipelago of about 115 islands relies on tourism for about 20% of its GDP. The sector also employs approximately 30% of the country’s labor force and provides about half of its hard currency earnings, according to the World Bank.

Shrinking global trade flows and the fear of additional protectionist measures as nations adopt stimulus packages and regulations to protect their own economies in a worldwide slump are also worrisome for African governments.

Foreign Funding Dries Up

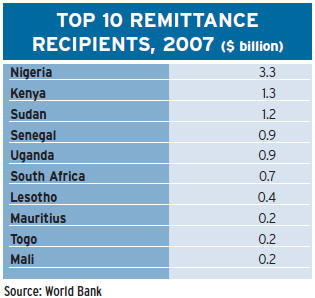

Remittances, another driver of the continent’s economic growth and a prime income source for many poor families whose breadwinners cannot find work in poverty-stricken rural areas, are down. Devarajan says that remittances to sub-Saharan Africa have already dropped 4.4% this year compared with the same time last year after increasing at annual rates of more than 6% in past years. In Kenya, for example, which had already seen its growth in remittances halved in 2008, remittances from Kenyans living overseas this year are expected not to increase at all.

Economists and politicians alike are concerned about how the region will fare as foreign investment, whether through capital inflows into debt and equity markets or direct investment in brick-and-mortar factories, wanes. Experts expect foreign direct investment, which reached $61 billion in 2008, up from $53 billion in 2007 and $36 billion in 2008, to slow. The figures, provided by the United Nations Conference on Trade and Development through the Corporate Council on Africa in Washington, DC, represent investment flows into all of Africa. The exodus of portfolio investment has already severely dented values in the continent’s primary stock exchanges, including the continent’s major economic engines—Nigeria, South Africa and Kenya.

An additional alarm going off in African capitals is the faltering level of Official Development Assistance, which is already running $20 billion short of the strengthened commitments made by the richest nations at the Group of Eight summit in Gleneagles, Scotland, in 2005. Officials and economists worry that ODA will stagnate this year. Even if all the major donor nations maintain their percentage of GDP, the absolute amount will shrink.

Morrison, now director of CSIS’s newly created Global Health Policy Center, sees sub-Saharan Africa separating into three broad categories as the economic downturn stretches on this year. The poorest nations, such as Guinea-Bissau, Burkina Faso and Togo in West Africa and Malawi and Swaziland, fall into one grouping. “Donor flows are 30% to 40% of the budget of some of these countries. If ODA or FDI is down, they are going to be hurt,” he comments.

The second group, according to Morrison, includes nations not endowed with oil that posted annual growth rates of 5% to 6% during the boom years and are suffering the least. These countries, such as Ghana, Tanzania, Ethiopia and Senegal, will fare reasonably well, though their growth rates will be halved. “They’re not in a tailspin,” he notes. “They’re more disciplined and better managed.” Morrison, who was the US democracy and governance adviser in Ethiopia and Eritrea from 1992 to mid-1993, adds that “Ethiopia is smiling now. They never opened themselves to the global banking system, and that has kept them outside the vulnerability zone.”

The oil-laden nations of Africa make up a third broad category. “They’re not exploding with cash like before,” says Morrison, adding that the impact of the steep fall in petroleum prices and subsequent recession will vary in countries like Nigeria, Angola and Sudan.

Usually an engine of economic growth for western Africa, Nigeria has been hurt by plummeting oil prices and a barely functioning federal government that uses a vast patronage system to run a giant nation of 140 million people sprawled across 36 states.

Kenya, traditionally an anchor of political and financial stability in eastern Africa, never quite emerged from its own economic meltdown sparked by riots after the January 2008 presidential elections. Columbia Business School’s Low, who was in Kenya for nearly three weeks in March, says Kenya’s story is the story of Africa. “Two steps forward and one and three-quarters steps back,” he says.

An emerging economy like South Africa falls into its own category, and its downturn, exacerbated by its greater dependence on credit and stronger links to the international financial system than the rest of sub-Saharan Africa, has hurt the southern African region. Even a well-regulated banking system and exchange controls on South African residents could not prevent a downturn that will produce 1% growth this year, down from 5% annual hikes between 2004 and 2007.

“The downturn has been less pronounced than in the United States, and the impact of the global financial crisis was not immediately noticeable,” says Janet Johnstone, chief administrative officer for the Middle East and Africa for The Bank of New York Mellon. Based in Dubai for the past six months, Johnstone previously ran the bank’s sub-Saharan regional operation out of its Johannesburg office and is a native South African who grew up on a farm in the Transvaal. “But everybody is affected. The sources of foreign funding into South African banks have dried up,” she says.

In a recent report, the International Monetary Fund warns that a sustained financial crisis could weaken the continent’s banking system, which so far remains largely sound, with less exposure to complex financial products and fewer links to global financial markets. The IMF adds that the risks could grow if distressed foreign parent banks withdraw capital from their African subsidiaries, call in loans to these local branches, do not keep investing local profits in the local subsidiaries, or carry out any combination of the three scenarios. “The credit crunch is raising the cost of short-term finance for African banks and making it much more difficult to raise long-term finance for projects and initiatives,” says Bassiri of the IFC.

Risk on the Rise

As bank clients’ incomes drop, credit risk could also rise, especially in countries where credit growth rates have increased rapidly in recent years, according to the IMF. The fund urges regulators to sharpen their focus on the banking sector, which it says “must be monitored vigilantly in order to minimize vulnerabilities and mitigate risks.”

With their links to other regions, South Africa, Nigeria, Ghana and Kenya were hit first by the global financial crisis as equity markets fell, capital flows reversed and exchange rates came under pressure. The IMF says external financing for corporations and banks has become scarce in South Africa and Nigeria. And Ghana and Kenya had to postpone sovereign bond offerings worth at least $800 million, points out Devarajan of the World Bank.

The Democratic Republic of the Congo “doesn’t have much to brag about,” says Morrison, even with its vast deposits of copper, cobalt, diamonds and gold. “There was too much hubris.”

Adds Sridhar Srinivasan, managing director and head of Citi’s sub-Saharan African global transaction services in Johannesburg: “There was so much perennial hope for the future. But the Congo has been badly hit, with the fighting in the east and the fall in commodity prices.”

In Sudan, with a strong economic performance and continued investment from the Gulf states and China, the Sudanese remain confident, even as their country’s president faces an international arrest warrant issued by the United Nations International Criminal Court and their economy suffers amid plummeting oil prices. Chinese political support for the Sudanese at international venues, such as the United Nations Security Council, will continue even if tempered by economic realities. “The political influence is a means to an end, driven by the economics. China is driven by its need for prosperity and jobs…Where can it get oil and copper?” points out Derek Scissors, a research fellow for Asia economic policy at the Heritage Foundation in Washington, DC. The Asian powerhouse is expected to maintain its long-term strategic interest in the sub-Saharan region even as it pulls back from projects that are no longer commercially viable because of low commodity prices.

“They don’t want to burn any bridges. They haven’t disappeared,” says Scissors, adding that the slowdown is a blow to African budgets during a time of stress. “When prices go back up, they’ll be back in there.”

Srinivasan says the economic downturn has especially affected investments by small private Chinese investors even as the large state-owned entities remain. “In fact, some of those who were operating small mines, like the minor copper mines in Zambia, have either sold out or cut down production to the absolute minimum,” he adds.

Yet the crisis could help Africa become more self-reliant as it turns to internal sources to generate growth and uses technology. Calestous Juma, a professor at Harvard’s John F. Kennedy School of Government in Cambridge, Massachusetts, points to a $600 million telecommunications project backed by Seacom, a private company based in Johannesburg with 75% of its backing coming from African investors, as a path for Africa to follow. The fiber optic cable project, now under way, will link southern Africa with London. The project underscores the importance of investing in infrastructure as a way to stimulate productivity, diversify the economy and counter the impact of the downturn, says Juma, who is a professor in the practice of international development and director of science, technology and innovation at the school’s Belfer Center for Science and International Affairs.

“Certainly many countries will be adversely affected, but the crisis also presents new opportunities for indigenous experiences such as greater regional economic integration,” Juma says. “It is a stimulus for creativity among alert leaders.”

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

Risk on the Rise

Risk on the Rise