President Obama’s determination to do “whatever it takes” to rebuild the economy appears to be paying off. But it is his actions across the whole range of policy initiatives that will have the greatest impact on global corporations.

By Jonathan Gregson

When Barack Obama entered the White House last January, it looked like the world economy was falling off a cliff. Six months on, and stock markets around the world have made good practically all of the losses racked up in the first quarter. Emerging markets such as China and India have surged even further into positive territory. Near universal fear has given way to cautious optimism.

When Barack Obama entered the White House last January, it looked like the world economy was falling off a cliff. Six months on, and stock markets around the world have made good practically all of the losses racked up in the first quarter. Emerging markets such as China and India have surged even further into positive territory. Near universal fear has given way to cautious optimism.

Recent weeks have seen a rash of signals indicating that the United States might be the first of the developed economies to enter recovery. Banks are lending to each other again, though mortgage and consumer credit remains tight. Both inter-bank and credit spreads have returned to levels last seen before Lehman’s collapse. Goldman Sachs, Morgan Stanley and other major banks have pushed through multi-billion dollar recapitalization issues and started to pay back loans from the government. Even battered hedge funds have seen investment inflows outpacing redemptions. “The improvement in market sentiment since last October,” says Stuart Green, global economist at HSBC, “should not be underestimated. If there are doubts about the sustainability of the recovery, we’re still talking about a recovery.”

How much of this new confidence is due to the “Obama Factor”? The first US president of African-American parentage was voted into office on the promise of change, and so far his administration seems to be delivering, whether it be his $800 billion fiscal stimulus package, his sweeping healthcare reform plans or more recently his proposals to overhaul and strengthen the US financial regulatory system. Of course, these might be watered down as they go through Congress, but with a popular mandate and Democrat majorities in both houses, he is likely to win through.

Green points to Obama’s fresh mandate and continuing high approval ratings as “key to pushing through fiscal policies on such a scale and so quickly.” And given the fearful market conditions prevailing when he took office, speed was definitely of the essence. “Right across the policy spectrum,” observes Green, “every area was pushed to exceptional levels.” The scale of the stimulus, both monetary and fiscal, “has been significantly ahead of what was anticipated during the presidential campaign,” he notes.

Business Reaps Benefits

Business Reaps Benefits

“There’s definitely an Obama factor, particularly in sending a message of confidence to the world,” says Paola Subacchi, research director for international economics at the London-based think-tank Chatham House. And that has been achieved not only by the boldness of decision-making and the sheer scale of his pro-recovery and healthcare programs, but by the more cooperative tone adopted when addressing other nations.

There has been a shift from the Bush administration’s application of “hard power” toward a softer approach built around regaining the moral high ground, encouraging dialogue and using persuasion instead of force. Obama’s commitments to withdraw US combat troops from Iraq and to close the detention camp at Guantánamo Bay were more than election pledges; they sent out a message to those in the Middle East, in Europe and in Latin America who questioned America’s moral leadership and resented its unilateralism.

Combined with the Obama administration’s commitment to move the Israeli-Palestinian peace process forward, this time with the involvement of moderate Arab governments, Obama’s efforts are diluting-if not entirely removing-the root causes of jihadist recruitment and broader hostility to America within the region. Obama has likewise used a series of finely balanced speeches to mend fences with sometimes unwilling partners like France and Germany and to defuse latent anti-Americanism in Europe.

The White House rushed into damage limitation after it was suggested that China was manipulating its currency, while many commentators have suggested that Obama’s superbly balanced Cairo speech on the Middle East may have swung the balance in favor of a pro-Western government in Lebanon’s recent elections. “Obama has showed that the US wants to be engaged in dialogue,” says Subacchi. An indirect benefit of this cooperative approach to US-based multinationals is that it should become easier to do business in countries that resented the Bush administration’s more confrontational stance.

Almost as important as what the Obama administration has done is what it has not done. Judging from some of his campaign speeches, it seemed likely that Obama would assume a more protectionist line on trade, immigration and keeping capital and investment within the country-policies that go down well with the Democrats’ core “blue collar” supporters. Instead, he has pushed onto the back burner such campaign issues as renegotiating the North American Free Trade Agreement (Nafta).

Aware that he needs the cooperation of key partners in Europe and Asia to revive the world economy-and, in the case of China, Japan and other creditor nations, to keep buying treasury bonds-Obama has moved toward anti-protectionism and closer dialogue. Subacchi says the Group of 20 summit in London was a turning point. “It worked toward preventing an outbreak of protectionism,” she says, “and was unexpectedly effective in coordinating policy response, both to end the current crisis and to prevent a future one from occurring.”

Obama’s commitment to do “whatever it takes” to get out of the financial crisis effectively gave the Federal Reserve a green light to keep pumping money into the markets. And by doing so, the Fed, under recession expert Ben Bernanke, staved off financial meltdown. “They learned well from the mistakes of the Great Depression,” observes Peter Hooper, chief economist at Deutsche Bank, “rapidly cutting interest rates and then moving aggressively into quantitative easing.” Pumping in liquidity to keep the markets from seizing up was, he says, “critical in preventing a bad situation from becoming much worse.”

Taking Risks to Minimize Risk

Using taxpayers’ money for bank bailouts has been deeply controversial, but given the very real risk of a financial meltdown, Hooper believes “the Treasury’s provision of public funds for the banking system was absolutely necessary to get things moving again.” The same applies to the scale of Obama’s fiscal stimulus.

As Dean Maki, head of US economic research and chief US economist at Barclays Capital, points out, this package is “bigger than all of the three previous stimulus packages put together.” Normally it would have taken time to steer it through Congress, but “Obama’s election mandate and personal popularity have been a significant advantage in securing its swift passage.”

The commitment of both the Fed and the administration to “do whatever is necessary,” says Subacchi, seems to have worked. “Both the speed and scale of policy response has resulted in the crisis not being as bad as many anticipated. From this side of the Atlantic,” she adds, “it looks like they managed to prevent the financial crisis from escalating.” Hooper agrees that the administration has acted “both aggressively and overall in an appropriate fashion” and that the current stimulus package “should move private sector demand in an upward direction.” Its effect on the real economy has yet to be seen because, as Green points out, “it takes time to have an impact on GDP and will probably not be felt until the third quarter.”

Maki points out that the bulk of the fiscal stimulus program has not yet had an effect on the economy. He expects “a big boost to household income this quarter,” while planned infrastructure spending will only be felt gradually over the next year.

More recently, Obama set out his plans to tackle one of the root causes of the financial crisis-namely, the failure of market regulators to identify and contain systemic risk. Again, it is a finely balanced package, avoiding unworkable suggestions such as reintroducing the Glass-Steagall Act. The Fed is to be given overarching powers to supervise all systemically important institutions, whether they are banks, insurance companies or industrial companies with major finance arms, such as GE. The White House also wants to set up a “resolution authority”-a government mechanism for “orderly resolution of any financial holding company whose failure might threaten the stability of the financial system”-and build in counter-cyclical capital requirements to reduce the chance of credit booms building up in the future. The administration also wants the huge over-the-counter swaps and derivatives markets to be traded on exchanges, thereby providing greater transparency and preventing an unseen buildup of “toxic” instruments.

If there is any weakness in these plans, it is that they do not go far enough. There has been little effort, for example, to coordinate regulatory reform in the US with even tighter restrictions proposed by the European Union and other major financial centers. If the plan goes through Congress relatively unscathed, it should produce greater confidence in financial markets. But the price of greater safety could well be higher funding costs for corporate borrowers.

Obama Sets the Pace

In tackling this crisis, the US authorities have led by example and, in some ways, made the work of other governments much easier. “Many of the Fed’s actions have been replicated by other central bankers,” observes Green, “while the scale of the administration’s stimulus has made it easier for other governments to push through their respective fiscal packages.”

But admiration of such an expansionary monetary policy is not universal. Germany’s chancellor, Angela Merkel, has voiced extraordinary criticisms of the Fed and other central banks that are pursuing such policies. Her comments have been echoed elsewhere in Europe, notably by Czech premier Jan Fischer. Meanwhile, the German parliament has voted to reduce the country’s fiscal deficit to zero. To ensure that there is no backsliding, politicians took the unusual measure of embedding this law within the constitution.

This represents a diametrically opposite move to that of the Fed, the Bank of England and many other central banks. According to Wolfgang Munchau of consultant Eurointelligence, Germany’s stand has less to do with economics than with ideology. “Most Germans have an aversion to debt and see the crisis as the result of Anglo-Saxon profligacy,” he says. However, as over-indebted consumers in the US and other deficit countries such as Spain have stopped buying automobiles and other “big-ticket” manufactured goods, Germany’s exports have plummeted, and its current account surplus, which last year stood at $235 billion, is set to do likewise.

Ironically, this and Obama’s willingness to flood the economy with money may cause other countries to develop protectionist tendencies. Many Germans, for example, fear that the euro’s appreciation against the US dollar, other dollar-linked currencies and the renminbi will price their exports out of the market. “My main worry about protectionist pressures stems from exchange rates,” says Subacchi. “Some voices in the euro area are asking why they should carry the burden of a stronger currency, especially as that could well lengthen their recessions. With elections coming up in Germany, there might be a temptation to protectionist rhetoric.”

A round of beggar-thy-neighbor protectionism could stall what many still see as an extremely fragile recovery. Leading indicators of a revival in industrial activity, such as crude oil and industrial metals prices, have bounced back strongly from the depths plumbed earlier this year. So, too, has the Baltic Dry Index, which tracks the shipping costs of bulk cargoes. Government bond yields have likewise been edging upward as investors switch to riskier assets. Emerging markets have outperformed. “The flight to safety,” Hooper observes, “is now being reversed.”

But, as Green notes, “while capital flows to emerging markets have picked up recently, FDI [foreign direct investment] tends to feed through much more slowly over the economic cycle.”

| Obama’s initiatives present a range of opportunities-as well as some key challenges-to global businesses. |

| Fiscal stimulus: Pro-growth policies give a short-term boost to all US-based companies, especially construction. The downside is higher taxes and borrowing costs in the future. Foreign relations: The shift to dialogue should facilitate trade and make it easier for multinationals doing business in “problematic” regions like the Middle East and Latin America. An Iraq pullout will adversely affect defense and civil contractors operating there. Trade policy: All competitive companies should benefit from Obama’s efforts to prevent trade wars. Leaving Nafta alone and allowing free trade agreements with Panama, Korea and Colombia to move forward is a bonus to corporations operating or trading in these areas. Many US-based producers could face tougher competition. Healthcare reform: If the system is streamlined, it should lower costs for both companies and employees. Healthcare, insurance and drug companies could lose out. The environment: Government plans to pump billions of taxpayers’ dollars into green energy and transportation. Companies in sectors such as wind and solar power, electric car manufacture, energy efficiency and battery technology will benefit, while traditional carbon-energy producers may suffer. |

Serious Concerns Remain

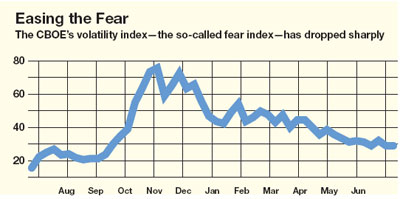

Six months after Obama took office, the world economy is still on a knife-edge. The stock market rally took a breather in mid-June, and what many consider the most sensitive “fear gauge,” the VIX index of US market volatility, began creeping up again. The US housing market-which arguably was the bellwether for the global crisis-is finally showing some signs of life. The latest figures for pending and new home sales both showed an improvement as buyers took advantage of government incentives and lower prices.

But these are very tentative green shoots. “There may be some bad news on the labor market,” says Subacchi, “as companies are still struggling.” This is a view borne out by a White House spokesperson who suggested the unemployment rate was likely to climb to 10% over the next two months.

These are scarcely benign conditions for a revival of consumer spending. “Part of the problem is behavioral, says Subacchi. “People save because they are uncertain and can see higher taxes down the road.”

“Corporations have been cutting back on investment and jobs in response to lower consumer spending since last fall,” says Maki, adding that “their response is slightly lagged, and the second quarter will see the largest decline in inventory levels ever.” However, he believes “we are at the end of the worst part of the inventory cycle, and if the economy stabilizes and turns to growth later this year, then the impetus for further cutbacks will weaken.”

Inflation fears, one of the drivers behind rising government bond yields, eased after the US Labor Department’s consumer price index (CPI) showed that during May “core” inflation ticked up by just 0.1 percentage points. Together with other data, such as the sharp fall during the first quarter in US imports, which reduced the current account deficit to its lowest level since 2001, this suggests that there is still plenty of slack in the economy.

“The rise in bond yields from such a low base is not entirely unwelcome,” says Green, though adding that “there is concern that their feeding through into higher mortgage rates might threaten the recovery.” With bond yields now flattening out, the Fed should be able to maintain its accommodative monetary policy for longer than many thought possible.

What if the spring rally peters out and the longed-for recovery proves to be no more than a dead-cat bounce? “The Fed has expended almost all of its ammo,” admits Hooper. “They could buy treasuries more aggressively, though I think they will hold off for now.” On the other hand, he does not believe the Fed will raise interest rates until absolutely convinced that a sustainable recovery is under way. “We’ll have to wait longer than the market is expecting,” he predicts. “And if unemployment continues to rise, there will be more fiscal stimulus.” That will delay any discussion of exit strategies. “While it is necessary to plan exit strategies well ahead,” says Maki, “we are not going to be there any time soon.”

Green believes that over the next six to 12 months “the US and other debtor nations will have to make more commitments to stabilize their deficits, through spending cuts or tax increases. That will pose a challenge to politicians. Austerity is unpopular, even though it may be necessary.”

While the animal spirits fueling the recent rally might have gotten ahead of themselves, “there is still ample scope for both business and consumer confidence to recover further from very depressed levels,” according to Green. “The consensus is that we might have touched bottom,” says Subacchi. “Some indicators, particularly in the US, UK and emerging markets, are beginning to point to an upturn. But conditions in other regional economies, most importantly the eurozone and emerging Europe, are still deteriorating and creating negative feedback effects.”

If the mood remains cautious, it is one of cautious optimism. “There are signs of the economy turning a corner,” says Hooper. “It will not be a booming economy, but it does look like growth.”

Given how things stood back in January, that would be a signal success, not to mention a stunning endorsement of Obama and the Fed’s approach of doing “whatever it takes.”