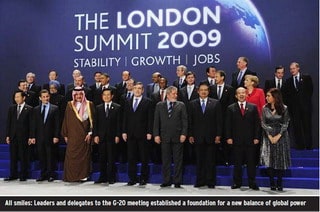

More generally, it can now be definitively claimed that the G-20, which includes Brazil along with Argentina, China, India, Indonesia, Mexico, South Africa, South Korea and Turkey, is now the center of global power rather than the G-8. There is recognition by the leaders of the global economy since World War II—Canada, France, Germany, Italy, Japan, the UK and the US—that they cannot dictate how worldwide trade and finance operates.

More generally, it can now be definitively claimed that the G-20, which includes Brazil along with Argentina, China, India, Indonesia, Mexico, South Africa, South Korea and Turkey, is now the center of global power rather than the G-8. There is recognition by the leaders of the global economy since World War II—Canada, France, Germany, Italy, Japan, the UK and the US—that they cannot dictate how worldwide trade and finance operates.

A new G-20-based Financial Stability Board will replace the Financial Stability Forum, which is run by 12 mostly Western countries. The G-20 also agreed to give developing countries more of a role in the operation of the World Bank and the IMF, and voting reform at these institutions is certain in the coming years.

The most important new actors in the G-20—China and Russia—have already flexed their muscles. Although they made little headway at the G-20 with their suggestion that the dollar be replaced as a global reserve currency by a currency based on the IMF’s Special Drawing Rights, the fact that such a suggestion was even made indicates both countries’ determination to become more assertive.

As renowned hedge fund manager George Soros declared in his latest book, The New Paradigm for Financial Markets, a permanent shift is occurring in the global economy that will end the West’s pre-eminence. Ultimately, developing nations—in particular, those in Asia, Soros believes—will become nothing less than “the center of the world economy.” What is equally certain is that greater economic power will be translated, sooner rather than later, into greater political power. The five permanent members of the UN security council—China, France, Russia, the UK and the US—are certain to be joined by Brazil and possibly South Africa in the coming years.

—Laurence Neville