After a long quiet spell in the global M&A; business, analysts and bankers are predicting that 2004 will be the year that activity really takes off again. But opinion is divided on whether this could be a record year.

For the long-dormant M&A; industry, 2004 could be the year when all the signs turned positive again.The consensus among bankers is that a healthy revival in corporate activity is likely to bump M&A; out of the stagnation it has endured over the past several years.The worst of the Iraq crisis is arguably in the past, stock markets are on the upswing and, according to Klaus Diederichs, JPMorgans head of European investment banking,the end is near in terms of the economic downturn.We go into the new year with pretty good confidence that momentum will hold through.

Hardly were the words out of Diederichs mouth when his employer fired off the first big salvo of the new year. JPMorgans $58 billion takeover bid for Bank One represents the largest merger in the US banking sector since the frothy bull market days of the 1990s, overshadowing Bank of Americas $47 billion deal with FleetBoston Financial last October. The transaction augurs well for further activity in this sector, which most analysts point to as a logical target for consolidation. However, the deal was sold to Wall Street solely on its merits, suggesting a lingering degree of caution in the market. Investors demand M&A; transactions that ensure value for shareholders.

Nevertheless, bullish sentiment abounds.The M&A; environment improved through 2003, and the outlook for activity in 2004 is looking good, says Philip Yates, head of investment banking for Merrill Lynch Europe, the Middle East and Africa. Yates points to a strong pipeline of transactions and the willingness of CEOs to do deals. CEO confidence picked up a little in 2003, with M&A; during the year characterized by big-ticket and increasingly interesting transactions, such as Telecom Italia/Olivetti and BP/TNK. Interestingly, there has been a higher proportion of European transactions within global M&A; during the year.

Philip Middleton, head of retail banking at Ernst & Young, agrees.There will be more transactions than in the past year, and these will go to a few high-quality and well-connected houses, he says.

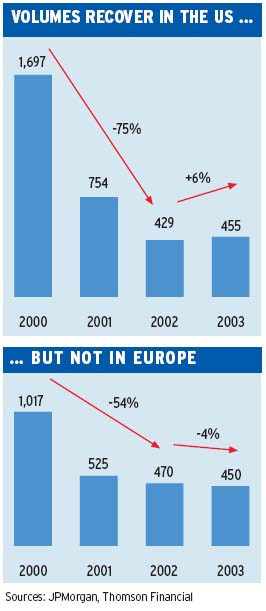

While these sentiments may seem relatively cautious, they reflect a degree of optimism that would have been unthinkable a year ago.There was never any doubt that 2003 was going to be another uphill slog for corporate finance bankers. Stock markets showed little signs of revival until well into the year, and the Iraq war loomed on the horizon, a destabilizing factor that was exacerbated by such unexpected hiccups as the SARS outbreak.The result in the M&A; market was largely flat volume in 2003 compared to 2002.The global M&A; volume for 2003 was $1.38 trilliona slight decline on the previous years $1.39 trillion, according to Dealogic. The pack was, as usual, led by the United States, which attracted 39% of global investment, up from 33% in 2002. Britain retained its secondplace position and with the rest of Europe accounted for another 39% of global volume. Asia once again showed itself to be the poor relation of M&A; business, with only Japan and Korea ranking in the top 15 target countries. Together they accounted for less than 10% of global volume.

There has been a big pick-up in activity since the fourth quarter of 2003, says Paul Gibbs, global head of M&A; research at JPMorgan. It has been a lot busier than last year, with volumes of very large deals coming out of the US. Going forward into the first half of this year,we see M&A; recovery a lot stronger in Europe and continued recovery in the US.

Not everyone is so optimistic. Heino Teschmacher, head of European M&A; at UBS, places himself in the ranks of the cautious with regard to this years outlook.We have good hopes and reasonable expectations that M&A; volumes will be higher this year than in 2003, but there are no indications that they will return to 1999 or 2000 levels,he says.Stock market valuations are higher than last year, so logically the same transaction today commands a higher price.There is also the important underlying factor that business confidence is higher at the boardroom level and also in the predictability of the future.

Fears Prove Unfounded

Traditionally, a poor end to the year is less worrisome than a sluggish start, since the first and third quarters are usually weak periods for completed M&A; transactions, whereas the second and fourth quarters tend to be comparatively strong. A major fear last year was that after the seasonally weak finish to 2002, the dismal trend would continue in 2003.

Philip Isherwood, global sector strategist at Dresdner Kleinwort Wasserstein, points to the upturn in the volume of activity in Q4 of last year, despite the unexciting fullyear outcome.The ugly economic and geopolitical backdrop of a year ago was reversed, and, most especially, the equity market direction changed in March, he notes.The fourth-quarter rebound came primarily on the back of some mega-deals in the US totaling $97.9 billion.Some of the most eye-catching transactions of that period were Anthems $16.4 billion acquisition of WellPoint Health Networks and Bank of Americas $47 billion deal with FleetBoston Financial.

Isherwood says that global M&A; is showing signs of coming out of its post-2000 slump, but he cautions that a debt-fueled M&A; binge is not in the cards, mainly because world economies are in the midst of a mini-cycle. US growth is expected to slow from the second quarter, and the early signs of economic and earnings momentum reversing are expected to be negative for equity markets, he says.

One of the factors fueling the recovery is that many companies have completed their internal restructuring programs that were begun around the end of 2000, says UBSs Teschmacher. CEOs now have more time available. In many ways, M&A; is a function of time availability,and it can be a very time-consuming activity at board level, he adds.

Confidence Matters

As Monica Insoll, head of European industrials at Fitch Ratings, points out, some companies are in a better position to be more adventurous in 2004. After the rapid consolidation that took place in many industrial sectors in the late 1990s, a lot of companies have managed to successfully restore their balance sheets, she says.However, many of those acquisitions are now looking overpriced, she adds,and this may be a constraint on future activity. On the other hand, there is an ever-increasing demand to deliver shareholder value, and in mature markets M&A; is one way to create growth.

Insoll believes that emerging markets, primarily in Eastern Europe, will be fertile ground for cost-conscious Western companies. The emerging markets are a key area of focus, she says. Western companies are increasingly looking for lower cost bases, and Eastern Europe is one region they have turned to in order to achieve that. In some of these countries the cost base is gradually rising with the improvement in living standards, so corporates are moving down the curve.Turkey is a very interesting market, with its greater level of stability and low labor and production costs,she notes.

Banks Ripe for a Shakeout

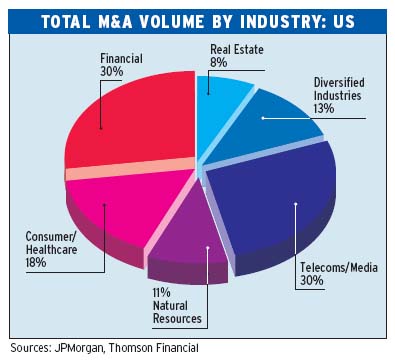

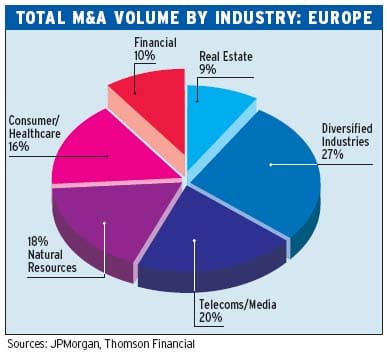

On a sectoral basis, financial services companies are likely to be in the forefront of consolidation plays in the coming months and beyond. Some analysts believe that banking and finance deals, which often foreshadow broader M&A; activity, may account for 25% to 30% of this years overall merger activity, given the several thousand large banks operating in the US, where more than a dozen finance-related deals last year were in the $2 billion- plus range.

Banking is a highly fragmented business globally, and especially in Europe, despite efforts to dismantle international barriers. Logically this should make the banking industry ripe for consolidation, but it remains very much a domestic market. Most of the consolidation we are likely to see in Europe will be in-market, and most probably in Germany and Italy, says Gerry Rawcliffe,managing director, financial institutions, at Fitch Ratings.

In the UK, says Rawcliffe, Lloyds TSBs attempt to take over Abbey National was blocked on competition grounds. But Lloyds is under pressure to grow and could look further afield for international M&A; activity. Barclays takeover of Banco Zaragozano is considered indicative of the route it will take, and Royal Bank of Scotland has built up a successful US franchise, which is where some M&A; activity is thought likely to take place.

Some major European financial institutions such as Spains BBVA have indicated the time is ripe to grow through acquisition abroad. But most bankers dont see a strong business rationale for such a move. Mergers are driven by revenue and cost synergies, and it is difficult to see benefits there, says Rawcliffe. There are also significant legal and cultural differences in Europe, and with the exception of the UK, banking regulators are pretty unwilling to see their banks fall into the hands of foreigners. There were rumors of US banks looking to come into Europe. But it is instructive that Bank of America went down the FleetBoston route rather than make a move in the UK. There was also talk of Citigroup buying Deutsche Bank, but that looks pretty unlikely, he adds.

Insoll singles out steel as another key area for restructuring. A lot is expected to happen in that area,she says. US Steel has been the main consolidator in the East European steel industry.There is still a lot of over-capacity in some Western industries, such as autos, steel and chemicals. Some consolidation has been taking place, but it is unappetizing for competitors to add to this overcapacity through mergers, so we may be looking at plants shutting down.

Teschmacher says that another area ripe for M&A; activity is the telecom sector. They have been repairing their balance sheets for the past couple of years, and quite a few feel significantly better now on a financial level, he says.Affordability is no longer necessarily the prime restricting factor in M&A; strategy, and they are starting to take a serious look at things they perhaps didnt want to do a couple of years ago.

Private Equity Deals Grow

Another big driver of M&A; this year will be private-equity- led deals, which in Europe alone have soared 43% since 2000, according to JPMorgan. Private equity firms are now among the biggest corporate buyers. Dealogic estimates that they account for 35% of all M&A; volume in Britain, the worlds second-biggest market after the US.

A significant factor of 2003 was the growth of privateequity- related deals, including Scottish & Newcastle, Debenhams, Gala and Selfridges, says Merrill Lynchs Yates. Private equity companies will continue to play a vital role in European M&A;, with companies such as Baxi and Grhe already set to keep the ball rolling into 2004.

Teschmacher highlights the fact that these financial sponsors are very active and many have large amounts of funds to be invested, despite the higher stock market valuations. Targets have become more transparent, and more company information is available to potential investors, he says.There is a lot of equity and debt capital available, and quite a few of these financial sponsors are looking to raise new funds, which brings pressure to realize existing investments.

A lot of corporates still have more work to do to reduce their debt.This provides a bonanza for liquidity-rich venture capital funds that are ready buyers of these companies. Globally the proportion of private equity deals is rising and in terms of value now accounts for 10% of all completed transactions, compared with 2% four years ago.

Last year, private equity firms closed 928 deals worth $101 billion across the world, according to Russell Florence, a partner at KPMG in charge of corporate finance. However, Florence injects a note of caution as to the sustainability of the private equity jamboree. The private equity community has taken advantage of a weakened economy, but as CEO confidence increases, how long can they steal a march over the trade buyer? he says. The operational synergies available to trade purchasers are likely to put pressure on the private equity buyer as the economic climate improves.

The resurgence of M&A; activity may be much in evidence this year, but not so the mega-transactions that characterized the boom times of four or five years ago. For M&A; to fire up properly, the return of the mega-deal is required, says Dresdners Isherwood.

Ernst & Youngs Middleton sums up the general mood in the market: Im a little suspicious of people who are claiming that happy days are here again and that deals are going to start falling out of the trees, he says.M&A; deals will not return to the heady days of the late 1990s, and corporate bankers had better get used to that fact.

Jules Stewart reports