Last year, more than half (52%) of the average daily share volume in US equities was from high-frequency traders, according to the TABB Group. Today’s markets move at lightning speeds, but this wasn’t always the case.

“When you look at the speed of trading in the financial markets, it’s been constantly improving over the last 40 years or so,” says Marti Subrahmanyam, professor of finance, economics and international business at New York University’s Stern School of Business. “Before that, the technology was essentially constant for well over a century.”

Market makers used to track trades on paper and match orders by hand. Traders stood in the pit, with specialists communicating through hand signals and by yelling. A key competitive advantage was a voice that pierced the noise. Today’s high-frequency traders entered the scene in earnest only 10 to 15 years ago.

“There is no definitive date on which high-frequency trading was born, but the general view is that HFT in the US equity market is an outcome of Regulation NMS, adopted in 2005 and fully implemented in 2007,” says Haoxiang Zhu, assistant professor of finance at MIT’s Sloan School of Management.

High-frequency traders typically begin and end the day with almost no inventory and execute trades at a very fast speed because of technology like field-programmable gate array (FPGA) cards, microwave links and co-located servers. In the blink of an eye, a high-frequency trader can execute hundreds of trades, earning a fraction of a penny on each.

Why does speed matter? “First, because they are trying to take advantage of discrepancies in the price of essentially the same asset in two different markets (arbitrage),” Subrahmanyam explains. “Second, to take advantage of information that’s revealed by the actions of others. You watch everyone else’s prices, and you change your behavior.”

The first high-frequency traders arbitraged futures contracts on stock indexes like the S&P 500 and the Dow Jones Industrial Average against the basket of underlying stocks, by calculating the indexes faster than the exchanges or predicting where futures prices would move. Traders looked at both sides simultaneously. With the arrival of the new information, the futures price might move immediately, but that might not be immediately reflected in all the underlying stocks or vice versa—that price difference is where the arbitrage occurs.

Technology has made the process more efficient and cheaper, but also more complex. “What HFT has done is automate the marketplace and move trading to machine-based strategies that pit one algorithm against the other,” says Larry Tabb, founder and research chairman of the TABB Group. “The algorithms are moving at such high velocity that it’s very difficult for humans to understand what happens to their order.”

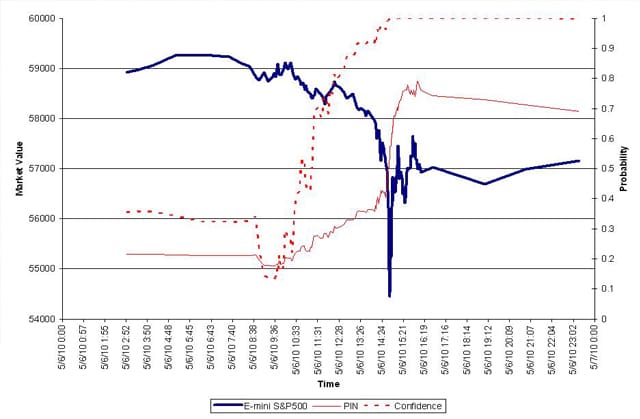

Increased volumes and tighter prices are some of the positive effects. Stock prices have tighter bid/ask spreads and smaller trade sizes now. Price discovery is also generally improved because of HFT activity. Occasionally though, an avalanche of orders pushes the price in one direction with no countervailing force. “The faster the speed, the more it moves away, because you have so much power in your trading and there’s no one on the other side—it could accentuate the volatility of the market,” says Subrahmanyam. “Liquidity is enhanced, price discovery is improved, but it could lead to a flash crash.”