MARKET REPORT | ISLAMIC TRADE FINANCE

Offering inventory financing to commodity traders brings much-needed liquidity to the Islamic trade finance market.

Domestic companies in rapid-growth markets such as Qatar, Indonesia, Saudi Arabia, Malaysia, UAE and Turkey are swiftly expanding beyond their domestic borders. According to EY’s April 2013 Rapid-Growth Markets Forecast, exports from these markets have doubled to 10% of world GDP, and by 2030 they are expected to double again. But who is going to finance increasing trade with high-growth countries in the Organization of Islamic Cooperation (OIC)?

The Asian Development Bank’s March 2013 Trade Finance Survey of more than one hundred banks found there was an increasing reluctance among conventional trade finance providers to extend financing, particularly in emerging markets. The survey revealed unmet demand for lending and guarantees to back $1.6 trillion in trade,

$425 billion of which was in developing Asia.

To help fill the gap, EY’s Global Islamic Banking Centre of Excellence (GIBC) expects Islamic trade finance will make strong inroads in rapid-growth countries, particularly given that Islamic finance already has strong trade links with what EY terms other “core” Islamic financial markets. “It makes business sense for global organizations that operate in and trade with many of these rapid-growth markets, especially those that are in the OIC or have strong links to the bloc, to seriously look at Islamic trade finance,” states Ashar Nazim, partner, GIBC, at EY.

In many cases Islamic financing may be the only form of financing available, as conventional banks are getting out of some business lines, asserts Michael Rainey, a financing partner working in Islamic finance and investment in the London office of international law firm King & Spalding. “Islamic banks may be able to come in and [finance trade] in a shariah-compliant manner.”

There are no concrete statistics available in terms of actual Islamic trade finance volumes, but such financing lends itself perfectly to trade as the focus is on real assets or commodities. “Commodities are very much the backbone of the Islamic finance industry,” says Paul Boots, director of the Dubai Multi Commodities Centre’s Tradeflow platform. The DMCC’s mandate is to facilitate the flow of commodities trade through Dubai. So it developed Tradeflow, an electronic platform that brings together banks, commodity traders and warehousing companies. “When we initially started developing Tradeflow, the focus was on a warehouse receipts financing platform where companies pledged ownership of commodities as collateral to the bank. But then we started talking to Islamic banks, and they said, ‘This is good for us to use, as physical commodities are part of our Islamic structures.’”

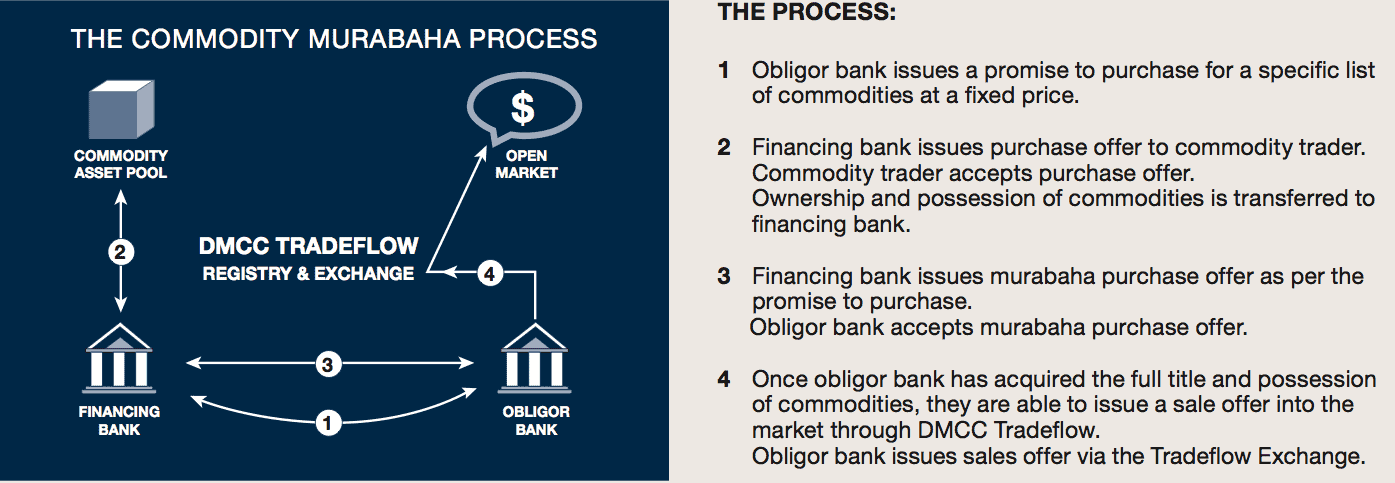

One of the most commonly used instruments in Islamic trade finance is murabaha, where the bank or financier buys the goods or commodities from the supplier and sells them to the customer on a cost-plus-profit basis. Rainey says a murabaha agreement stipulates the customer will buy the goods as the agent of the bank. The bank has legal title to the goods until it sells them to the customer. The bank does not pay the supplier of the goods until the customer or agent confirms he or she wants to buy them, although from a shariah perspective, Rainey says, the whole point is that the bank is supposed to share the risk. “More often than not,” he notes, “with Islamic finance you end up with something similar to conventional trade finance, but there are some additional steps you have to go through legally with Islamic finance. Once it is set up, however, it’s not very complicated.”

DMCC’s Tradeflow uses commodity murabaha. It works with independent third-party warehousing companies in the UAE, which store commodities on behalf of customers. The warehouse issues an electronic warrant of ownership, which is traded on Tradeflow. “Companies can start trading the warrant on our platform without the goods having to leave the warehouse,” Boots explains. “So an Islamic bank financing a company can take control of that commodity and sell it back to the customer with payment deferred over a period of time, which allows the customer to obtain funding up front. The bank has physical control of the commodity, which provides some surety if something goes wrong.”

Companies who have no physical requirement for commodities, in manufacturing, for example, can sell them to raise financing or working capital. “We have market makers who are able to purchase these commodities,” says Boots. Islamic banks can purchase commodities via Tradeflow to sell to other banks for treasury management purposes, as Noor Bank and the Commercial Bank of Dubai did in the inaugural commodity murabaha transaction on Tradeflow in March last year. Noor Bank also uses DMCC Tradeflow to provide settlement for commodity murabaha financing, which it extends to small and medium-size enterprises and large corporates. “Broadly speaking, SMEs have a financing need,” says Ehsaan Ahmed, head of global transaction services and corporate strategy at Noor Bank, a leading Islamic financial services provider based in Dubai. “Largely, their requirements are for short-term trade finance and working capital, but a need for longer-term funding also exists where SMEs are looking to finance projects involving capital expenditure for initial setup or expansion of existing operating infrastructure.” According to Ahmed, most SMEs in the UAE are agnostic in terms of whether it is a conventional or Islamic bank that provides the financing: “But if an Islamic bank is able to help them address that need better, they will bank with them.”

The size of transactions conducted on DMCC Tradeflow depends on the physical availability of commodities at the time of the transaction. “For our initial launch period, and considering our focus on the SME market, which does not require handling extremely high-value individual transactions, we have worked with commodity suppliers to ensure we can facilitate individual transaction values of up to $400 million per transaction,” says Boots.

The DMCC has also created what it calls a robust legal infrastructure to facilitate proof of ownership of physical commodities. “If banks are going to be financing commodities, they want to ensure they are where they are meant to be,”

“More often than not, with Islamic finance you end up with something similar to conventional trade finance, but there are some additional steps you have to go through legally with Islamic finance. Once it is set up, however, it’s not very complicated.”

~ Michael Rainey, King & Spalding

Boots explains. Shariah scholars had previously voiced concerns regarding the underlying title transfer mechanisms and certifying the existence of goods in a commodity murabaha transaction. “We’ve addressed the concerns that were out there,” Boots insists. “We offer full certification of third-party warehouses, and shariah scholars from banks can physically inspect the commodities in the warehouse.”

Ahmed of Noor Bank believes ensuring that the physical assets being traded are available, as well as issuing electronic warrants to reflect the bank’s title to the goods, is important, particularly from the perspective of adherence to shariah principles. Boots says Tradeflow automatically checks whether the commodities to be traded in a murabaha transaction are on its shariah board’s list of halal (permissible) goods and are stored in a dedicated, DMCC, halal-rated independent warehouse. The majority of commodities that are used for murabaha transactions include foodstuffs, such as rice and grain, along with oil, copper and other metals.

Sofian Shiyab, business and corporate adviser at London-based UMEX Trade Bridge (UTB), an affiliate of UMEX Capital Markets Group, which provides financing technology and specialized screening solutions with a focus on ethical and shariah-compliant investments, says murabaha is less risky for the economy, as in the case of a default the bank or lender already holds the assets and there is no interest to be paid—riba [usury] being forbidden in Islamic finance. Shiyab says he is seeing increased demand for ethical financial instruments. UTB aims to provide the full range of trade finance solutions, including Islamic trade finance, to SMEs governed by corporate social responsibility and ethical principles.

But EY’s Global Islamic Banking Centre states that the conversion to Islamic trade finance will not succeed without a clear framework that gives businesses a good reason to make the switch from conventional to Islamic. Islamic banks need to build international connectivity and scalable trade finance platforms, EY adds, that can connect with businesses and financial institutions beyond borders. Doing so will be challenging, it states, given the smaller scale and localized nature of most Islamic banks.

DMCC Tradeflow is already delivering operational efficiencies and cost savings to Islamic banks by automating warrants of ownership. “The digitization of the platform means banks can cut down processing times, which allows them to reduce cost,” says Boots. “These transactions used to be done by fax, which took hours. Now we can do them in minutes. Our platform has also allowed Islamic banks to do smaller-size transactions, which is good for SMEs looking to access financing.”

Noor Bank’s Ahmed says any Islamic bank servicing SMEs, whose transactions are typically smaller in value but higher in volume, needs an efficient back-end settlement platform like Tradeflow. “Using Tradeflow, we are able to turn around customer requests for disbursement of funds under commodity murabaha much faster, which results in higher customer satisfaction and better capacity utilization on the back end.” Before Tradeflow was launched, Ahmed says, the settlement of the underlying commodity murabaha was conducted on the London Metal Exchange, and because of the time zone difference, settlement cutoffs were restrictive. “If we’re able to improve our delivery because of DMCC’s Tradeflow, then it certainly helps us in securing more business,” he adds.

In early September international banking association SWIFT, in collaboration with the Association of Islamic Banking Institutions Malaysia and the Malaysian Islamic financial community, announced the launch of a new rulebook for the use of SWIFT MT (Message Type) messages (including payments, securities, and trade finance) for Islamic finance. The rulebook is designed to provide greater clarity around SWIFT MT message usage based on Islamic principles, in order to enable straight-through processing, thereby improving efficiency as well as reducing risk and cost.

All of these developments in back-end processing efficiencies will no doubt help make Islamic trade finance more affordable, but if it is to truly carve a niche for itself, Rainey of King & Spalding believes Islamic banks will need to compete in areas where the larger conventional banks are not present or have retreated. “It is just finding the customers and the exporters and the banks who have the appetite,” he says.