Solid fundamentals and steady structural reform could be undercut by political chaos and global market turbulence.

Spain is in a sweet spot—for the moment. If, however, the cycle is topping out, the very factors behind the economic surge will reverse and more typical spending patterns are destined to resume. Perhaps most significant, oil prices threaten to rebound. Lower energy prices have been responsible for 0.7% of the nation’s disposable income growth, recently running at 3%.

“Spain is more dependent on energy imports than most EU countries,” says Stephen Brown, European economist at Capital Economics, who predicts that in 2017 energy effects will start detracting and that disposable income growth will fall to 2%.

The euro is no longer depreciating, to cite another driver in reverse. Trade underpins the Spanish economy, in particular exports of medium technology goods like chemicals and metals. In conjunction with currency weakness, lower interest rates and a smaller risk premium have supported general confidence and led to easier financing conditions. Private consumption also has been growing for 12 consecutive quarters, fostered by a stronger labor market, and has encouraged household spending. Consumers have been keen to satisfy pent-up demand and have been lured by bargain prices. In addition, several temporary factors have contributed a fillip, such as the tax cuts that were advanced by six months to July 2015 and the government’s reimbursement of one-quarter of salary payments to public-sector employees.

Fiscal Adjustment

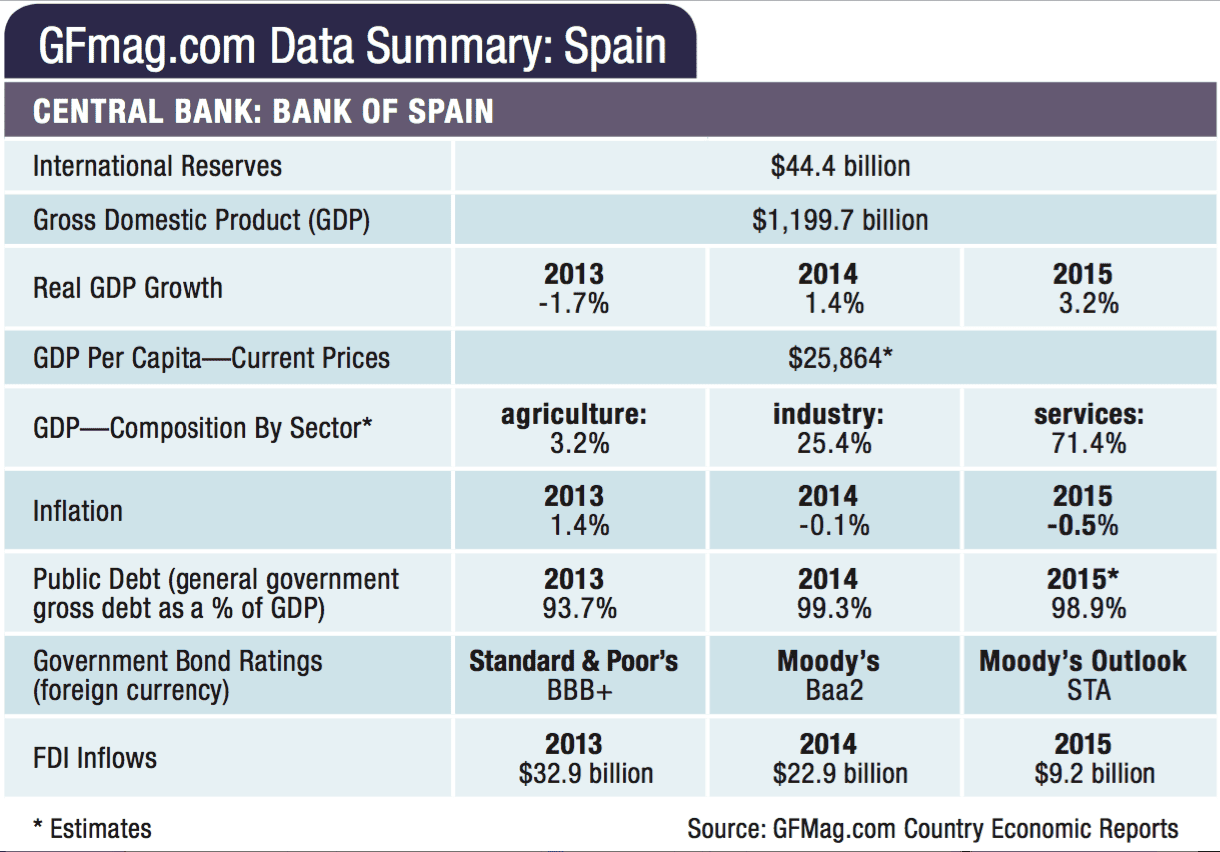

While the cycle runs its course, the government must tackle a set of necessary reforms. First, it must face up to a deficit that is the second-highest in the euro region. Economy and Competitiveness minister Luis de Guindos announced to parliament in April that Spain anticipates a fiscal shortfall of 3.6% of GDP in 2016, and 2.9% in 2017.

“No party would clearly admit to it, but the government missed fiscal targets last year and this year and must now return to the austerity table,” says Raj Badiani, senior principal economist at IHS Global Insight. Even robust growth has not narrowed the deficit as fast as hoped, because of headwinds: two sets of tax cuts, offered to win over voters; low-paid employment, mainly in the service sector; and a 20% unemployment rate. The resulting mix of low tax receipts, increased unemployment benefits and government interest costs “have made the debt pile much larger and will require more pain and effort to get back on the fiscal path,” Badiani concludes.

Revenues are not balancing expenditures. Antonio Barroso, senior vice president at Teneo Intelligence, explains that for the past year, the administration has been tapping funds reserved for pensions. “If the government continues to draw on the funds at the current rate, experts estimate they might dry out by the end of 2017,” he warns. The government would need to pay out of the budget, adding to the deficit.

On a brighter note, unemployment is gradually receding, with the overall rate dropping from 23.8% in the first quarter of 2015 to 21.0% in the same period this year. (Dismal levels of youth joblessness, nonetheless, remain stubbornly north of 40%.) The labor force itself has soared over the past decade, “fueled by a steady inflow of migrants and rising female labor participation,” according to Badiani. Even as recovery has taken hold, firms still gravitate toward short-term contracts, because “firing workers on permanent contracts remains too costly and laborious,” Badiani says. Penny-pinching contract workers tend to be more cautious spenders and are excluded from the mortgage market.

Some of the structural reforms implemented in the past few years have dampened labor’s bargaining power, giving employers flexibility. “Companies can now opt out from collective agreements, so working conditions for each firm reflect more accurately that particular company’s own situation,” says Enric Fernández, chief economist at CaixaBank. He expects unemployment to dip below 20% this year, with a further 1.5% lopped off each year thereafter.

At the same time, Spain’s regional states, which are mainly run by left-wing coalitions, are all struggling with budget deficits. Local politicians gain power by promising not to cut healthcare, education or other social benefits. That tension between promises and revenue shortfalls creates “potential at the state level to be fighting with the weak right-wing government at the federal level,” Brown notes. For those reasons, Spain missed its overall deficit target last year and may find itself confronting a similar scenario again.

Unpredictable Politics

Election results in June put a government in place again, but it is horribly splintered. The elections produced no party majority, and subsequent negotiations failed to reach a stable governing coalition. How badly did the fragmentation actually affect the economy over the past year? Political paralysis may have been manageable in the short term, according to Barroso: “The civil service functions, and people continue to pay taxes—unlike, say, in Greece—even if they hold off investments when they lack political clarity.” Still, a wobbly balance of power makes policy even more unpredictable than usual.

The former two-party system, dominated by the conservative Partido Popular (PP) and the socialist PSOE, has evolved into a four-party structure that includes left-wing Podemos and centrist Citizens. “Parliament has become so fragmented that it is hard for parties to reach workable agreements,” says Barroso. “The system now is in flux, without incentives to cut deals.” The minority PP party must try to govern without a majority coalition.

Every single policy measure will need to be negotiated in parliament. “Nobody would have been happy to go into a third election” says Fernández. The negotiation required to pass major legislation may stall progress, since important reforms demand consensus. He hopes a culture of inclusive negotiation, like, for instance, that in Germany, evolves. “People will be forced to talk to each other,” he says. “We are in new waters.” Some, however, are simply hoping for better results from the next election.

Needed reforms extend to soft infrastructure. In education, for example, the government has been changing the system every four years, creating instability. Public-sector and pension reforms are costly to implement, but “if everyone buys in, the political cost is spread out,” Fernández observes. Labor market rules especially need fine-tuning to encourage hiring on permanent contracts.

A thorough overhaul of the banking system has already paid off, but work remains. The number of banks has shrunk dramatically, with restructuring, consolidation, lay-offs and reduced capacity. “Those reforms offer a lesson for other countries to draw on—and help explain some of the growth differentials,” suggests Fernando Navarrete, chief financial officer at Instituto de Crédito Oficial.

Global Outlook

After the financial crisis, many Spanish companies turned to cultivating global markets and, having invested fixed costs, will continue to reap the fruits. Exports rose 5.5% last year and should advance another 4% in this year’s more muted global environment. “With gains in competitiveness, Spain has recovered its losses from the post-crisis years,” Fernandez reports. Navarrete attributes much of that success to breadth both in the reach of external markets and the range of products. Export destinations have widened, not just in Latin America, but also in North Africa, Europe and the US. Along with diversifying its products and services, the country has achieved preeminence in supply chains and global finance. “By 2013, Spain realized that not enough growth could be generated domestically, so they must grab it from outside,” Navarrete says.

With reliance on exports comes the risk of backlash. If trends against globalization transform into active political agendas (such as isolationism in the US, nationalism in the UK and various extreme left- and right-wing movements elsewhere), open economies like those of Spain or Germany will suffer. “We will all lose, but especially an economy like ours,” Navarrete predicts.

Britain’s choice to leave the European Union offers a case in point. Britain and Spain have long enjoyed close financial ties, extending far beyond tourism, Badiani notes. A weaker pound sterling discourages British tourists, who account for 25% of Spanish visitors; the Brexit vote might also dampen British residents’ enthusiasm for Spanish real estate, which may impinge on the ongoing recovery in the construction industry. Conversely, Spain has considerable foreign direct investment in Britain, built on the traditional economic links between the two nations. Firms such as Banco Santander, Ferrovial, Iberdrola and Telefónica own substantial UK assets.

From the other direction, a number of UK multinationals are exposed in Spain to the risk of upheaval. Burberry, in the retail sector has five stores there; Diageo, maker of Smirnoff and Baileys, estate agent Savills and British Telecom have all significant Spanish operations. In the energy sector, BP owns multiple assets there, including the Castellon refinery and a retail network of 670 service stations, and commands a 9% share of the Spanish oil market.

Despite uncertainties unleashed by the Brexit referendum, Spain will pursue its new, balanced model. “You can’t point to any single element as the source of growth,” says Navarrete. “It no longer depends just on real estate and construction, but now all engines are firing and working in harmony.”