CORPORATE FINANCING NEWS / CORPORATE DEBT

by Gordon Platt

The high-yield bond market felt the spillover effects in early June from a steep decline in prices of bonds backed by subprime mortgages, but US-based companies continue to tap the below-investment-grade market with relative ease. Although weak economic data and the end of the Federal Reserve’s second round of quantitative easing have dampened the investment outlook for stocks, the low-inflation and low-default environment makes corporate debt relatively attractive, says Benjamin Garber, assistant director and economist at Moody’s Capital Markets Research.

“Limiting any substantial setback for bond prices is the mild outlook for inflation,” Garber says. “The yields on US corporate debt have steadily fallen over the past 30 years, following the downtrend in consumer prices.”

Falling Home Prices

Renewed home price declines are a major drag on overall inflation readings, Garber says. “We believe that the housing overhang limits the risk of a pickup in inflation for several years,” he says. Housing costs account for 54% of core consumer price inflation. Weaker job growth extends the horizon for clearing the heavy inventory of distressed properties, Garber says.

The high-yield spread in mid-June was 509 basis points above comparable-maturity US treasuries. The spread was 92 basis points above the 2011 low, but the yield of 6.96% was up only 34 basis points. This contrasts with last summer, when both speculative-grade yields and spreads were quick to jump from their April 2010 lows, Garber says.

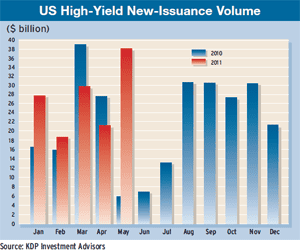

“The market’s ability to absorb the record $61 billion of global high-yield issuance in May shows that liquidity remains robust,” Garber says.

Low Default Rate

|

The 2.7% US high-yield default rate in May was well below the historical average of 4%. The default rate may fall below 2% by the end of this year if economic growth holds at a subpar—but positive—rate, Garber says.

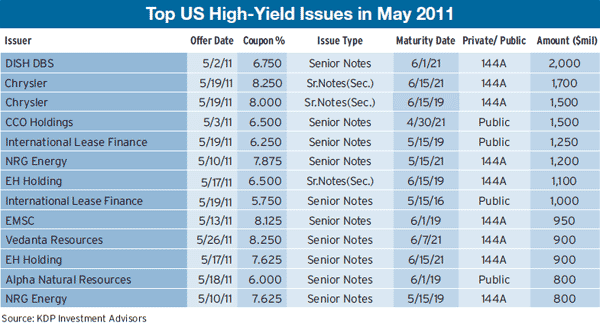

A total of $38.1 billion of new high-yield bonds were issued in the US market in May, an increase from $21.2 billion in April, and the highest monthly total so far this year, according to Montpelier, Vermont–based KDP Investment Advisors. The biggest single issue in May was a $2 billion offering of 10-year senior notes by DISH DBS, a subsidiary of the DISH Network, which provides satellite TV services to more than 14 million customers.

Englewood, Colorado–based DISH initially planned to issue $1 billion of notes in its first bond offering since September 2009. It increased the size of the offering to $1.75 billion in the face of strong investor demand, and later raised it again to $2 billion. Deutsche Bank was the sole bookrunner for the issue, which was placed in the private market at a yield of 360 basis points over treasuries.

Auburn Hills, Michigan–based Chrysler repaid the balance of its debts to the US and Canadian governments on May 24, after raising $7.5 billion with a refinancing plan. The automaker issued $3.2 billion in notes and took on $4.3 billion in new loans from banks. The notes were issued in two parts: $1.5 billion of 8% secured senior notes due in 2019 and $1.7 billion of 8.25% secured senior notes due in 2021.

|