Ethiopia actively courts and sincerely welcomes foreign direct investment, but its early stage of development presents challenges.

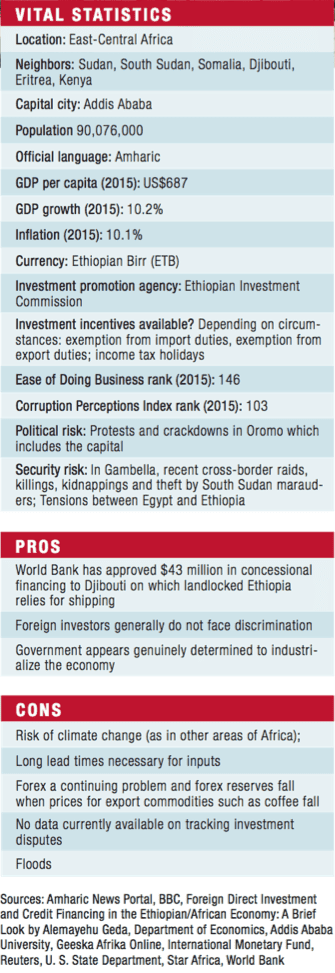

Although dwarfed as a destination for foreign direct investment by its African neighbors South Africa, Egypt and Nigeria, Ethiopia has attracted increasing levels of FDI, according to data from the United Nations Conference on Trade and Development (UNCTAD): $2.2 billion in 2015 from $279 million in 2012. In 1999, Ethiopia attracted a mere $12 million.

Undertaking a project in Ethiopia means recognizing its differences from other African nations. History heads the list. Many former colonies have a legacy, mentality, administrative structure or set of ownership structures from their colonial eras, but Ethiopia has no such traditions, according to Melissa Cook, managing director of African Sunrise Partners and a member of president Obama’s Advisory Council on Doing Business in Africa. By comparison, she explains, “If you go to Gabon or Congo Republic, you can very much feel the French influence.”

Although Ethiopia is resource-poor, its location on the Horn of Africa, relatively stable political environment and government leadership, and generous incentives explain its attraction for foreign investors, Alemayehu Geda, economics professor at Addis Ababa University, asserted in March. The path to this expansion started in 1991, with the downfall of the Derg regime and its centralized command system and the rise of the Ethiopian People’s Revolutionary Democratic Front. The Front leans toward a free market philosophy.

Moreover, in its second Growth and Transformation Plan, which runs to 2020, the government maintains a tight focus on bringing its people out of poverty. This aim makes its priorities and approach to attracting investors different from other countries.

“It’s very focused on bringing a lot of people out of poverty and taking a much more egalitarian approach,” Cook says. FDI priorities include projects that will provide large numbers of jobs, affordable products for low-income individuals and exports to generate foreign currency. Thus, areas of focus include agribusiness and consumer goods, infrastructure, leather, textiles, engineering, tea, coffee and manufacturing.

Above all, the plan is not a mere doorstop but a blueprint for decision-making. “You have to follow [the plan] very closely,” says Cook. “Ethiopia is not just a free-for-all (where) you go in and see an opportunity and decide you want to do it.”

Although the Ethiopian government has a very large welcome mat out for some industries, it keeps others closed to foreign investors, including banking, telecommunications, retailing, aviation and logistics. Foreign banks cannot participate directly in Ethiopia’s financial sector, but can open representative offices to support clients who have obtained financing internationally, explains Taitu Wondwosen, head of Johannesburg, South Africa-based Standard Bank’s representative office in Addis Ababa. Standard chose to enter the market, even with just a representative office, because the market was open to various clients, Wondwosen says. Standard Bank hopes to receive clearance to graduate to full-service-bank status, but that appears unlikely until the next growth and transformation plan—at least five years in the future.

In the meantime, clients based in South Africa, South America and Asia, operating in sectors such as power and infrastructure, obtain all or part of their financing for a project in Ethiopia through Standard’s head office or one of its branches, and the representative office helps them understand the lay of the land.

In the future the bank might plant its flag in Djibouti, with its shipping and port facilities on which Ethiopian exporters rely heavily. Ecobank, Commerzbank and Kenya Commercial Bank have representative offices there, and other banks are studying the possibility.

Meanwhile, Ethiopia remains a magnet for funds from the Gulf region from three major sources, according to Zin Bekkali, chief executive officer of Silk Invest, an investment firm specializing in frontier markets, and as of mid-June, falling oil prices had not substantially dampened the flow. Large amounts of investment capital come from major individual investors such as Mohammed Al Amoudi, born to a Saudi father and Ethiopian mother and a strong supporter of Ethiopian growth. His businesses within Ethiopia alone include Sheraton Hotels, the local bottler of Pepsi Cola, and cement, steel and oil plants.

“Then you have the remittance side and the intergovernmental investment,” Bekkali says. Remittances come from Ethiopians working outside the country, who are increasing within the Gulf, in many cases replacing Filipino workers. During 2015, such remittances from all countries topped $3.5 billion, and much of this money goes into housing and education. “It has a lot of positive impact on the economy,” Bekkali says.

Ethiopia has other challenges, including a relative lack of sophistication with respect to business infrastructure. “Ethiopia is a developing environment,” Bekkali says. “The legal structure is still in development, and the rules of business are not fully developed.”

Also underdeveloped is the capital market, meaning that an investor has little chance of raising capital within the country. “They had better have all their financing, because they are not going to get any there,” Cook says. “It’s not just capital expenditures. It’s operations funding.”

Ethiopian law does not have currency restrictions, but the shortage of foreign currency makes repatriation of profits extremely difficult. Converting funds from the Ethiopian birr to the American greenback can take up to several months for one transaction.

“It’s not a policy issue,” Cook explains. “It’s a separate issue, because they are not generating enough exports to generate the forex.” This causes problems in paying for imported inputs in manufacturing a product, such as when the syrup for a bottled beverage has to be imported and paid in another currency. Investors may well face this problem until the capital investment programs that absorb foreign currency are completed and government strategies for boosting exports take hold.