CORPORATE FINANCING NEWS

By Gordon Platt

The volume of emerging-markets corporate debt offerings declined 6.2% in 2013 from a year earlier, even as global high-yield debt issuance set new records, according to Thomson Reuters. Issuers in just three countries—Russia, India and Mexico—accounted for nearly half of last year’s EM corporate debt total of $297 billion.

Corporations from emerging markets economies have increasingly turned to offshore financial centers to issue debt securities, the Bank for International Settlements (BIS) says. EM corporates have overtaken companies based in developed economies as the largest group of issuers in offshore centers.

The surge in offshore issuance is largely owing to issuers in Brazil and China. Chinese companies’ borrowings in offshore centers increased from less than $1 billion in 2002 to $51 billion in the 12 months through midyear 2013, the BIS says. Brazilian companies have a much longer history of borrowing abroad. After borrowing between $2 billion and $6 billion a year in offshore centers between 2001 and 2005, Brazilian companies borrowed almost $20 billion between July 2012 and June 2013.

AVOIDING CAPITAL CONTROLS

Issuing international bonds through controlled entities in offshore centers allows Chinese and Brazilian firms to reach investors that would find it difficult to invest in their local markets, the BIS says. Many institutional investors do not have the mandates or technical capacity to invest in EM domestic bond markets, it says. What’s more, buying bonds in offshore centers lowers their administrative burden and makes investors less likely to be affected by capital controls than if they buy domestic securities.

Chinese companies have traditionally financed themselves domestically. However, the sustained growth of China’s economy has increased the demand of international investors for Chinese financial assets. This has made it cheaper for Chinese companies to raise funds abroad, particularly for securities denominated in renminbi, the BIS says.

Bonds denominated in renminbi in the Hong Kong market, known as CNH bonds, outperformed dollar-denominated and other local currency bonds in Asia last year, with a more than 6% total return in dollar terms, as investors sought stability in the resilience of the Chinese currency, according to a report by HSBC.

RENMINBI EXPECTED TO APPRECIATE

“We are optimistic about CNH credits going into 2014 and expect a total return of 3% to 4% in dollar terms,” HSBC analysts say. “Of course, the expected reduction in US monetary easing and the potential outflow from emerging markets are a concern. But we are confident that the renminbi will continue to appreciate, thanks to capital-account liberalization.”

HSBC predicts more international participation from both issuers and investors in the CNH market. “The players will benefit from China’s capital-account deregulation, while enjoying flexibility,” HSBC analysts note. The development of the Shanghai Free-Trade Zone has become a benchmark for monitoring renminbi liberalization and internationalization, it says.

John Stopford, portfolio manager of the Investec GSF Global Strategic Income Fund and co-head of the Investec multi-asset team, says 2014 may be a difficult year for corporate credit and a modest one for emerging markets debt, “but there may be an attractive long-term buying opportunity later in the year.”

CREDIT UPGRADES LESS LIKELY

While yields on government bonds remain unattractive, according to Stopford, investment-grade corporate bonds offer a modest pickup in yield—and high-yield bonds, a more significant advantage.

“However, the additional yield offered by credit is unlikely to be sufficient to compensate for a rise in government bond yields,” Stopford says. “The opportunity for credit upgrades is diminishing as companies with the potential to improve balance sheets have mostly done so.”

“However, the additional yield offered by credit is unlikely to be sufficient to compensate for a rise in government bond yields,” Stopford says. “The opportunity for credit upgrades is diminishing as companies with the potential to improve balance sheets have mostly done so.”

Credit may be a disappointing investment until government bonds have adjusted, Stopford says. “The opportunity in emerging market debt looks better, with many currencies having weakened significantly,” he adds. “Yield spreads over developed market bonds are reasonable, and the opportunities for adding value are more extensive, although emerging market currencies may need to weaken further in the short term.”

In the US in 2014, the swing away from fiscal tightening will be bigger than the tightening seen in 2013, Stopford says. Along with improving capital spending and consumer spending, helped by lower gasoline prices, the diminishing fiscal headwinds should allow the US economy to grow much more strongly than for a number of years, he adds. “This should cause markets to rethink the speed of policy normalization pursued by the Federal Reserve,” Stopford says. “It may still be gradual, but not perhaps quite as gradual as suggested by forward market pricing.”

FISCAL POLICY DRAG LESSENING

Former Fed chairman Ben Bernanke, in a speech to the American Economic Association in January, said that “excessively tight near-term fiscal policies have likely been counterproductive” by weakening the recovery, especially when monetary policy has less room to maneuver. But Bernanke also said he believes the headwinds to growth are diminishing, as the drag from fiscal policy is lessening.

Søren Willemann, head of European fixed-income strategy at Barclays, says: “To date, the market’s reaction to Fed tapering has been comforting, supporting our strategic view that tapering alone should not lead to market weakness. In the very short term, we believe markets will remain firm. However, in the medium term, spread stability (or moderate tightening) will be predicated on sustained strong economic data.”

There have been plenty of “tapering fire drills” since last May, Willemann says. “We would argue that a lot of the adverse impact from rising rates has already been absorbed.” Willemann adds that the tapering announcement in December came amid generally improving economic data, reducing the perceived risk of a policy mistake.

European high-yield bonds were the best-performing fixed-income asset class in 2013, according to Barclays. December was another solid month for European high-yield debt, with Barclays’s benchmark cash index tightening by 40 basis points, ending the year at a new post-crisis low.

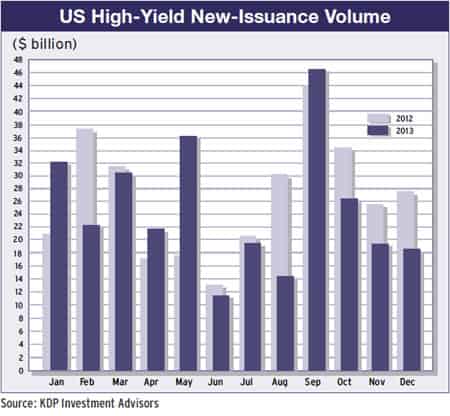

The volume of global high-yield corporate debt rose 19% to $462 billion in 2013, the strongest volume since record keeping began in 1980, according to Thomson Reuters. Issuance from European issuers more than doubled, compared with 2012. US issuers accounted for 56% of last year’s total, down from 72% in 2012.