The Investment Institute at Wells Fargo offers investors a handful of key themes to keep an eye on this year.

If there’s one lesson high-net-worth investors can take from 2016, it’s that they need to look past short-term market volatility when measuring portfolio performance.

2016 was an eventful year. It started off with concerns about the restructuring of the Chinese economy and culminated with one of the most controversial US presidential elections in recent memory, with the shock of Brexit in the interim. But, as Darrell Cronk, president of Wells Fargo Investment Institute (WFII) points out, investors who let themselves get distracted by “negative” geopolitical events risked missing what was happening in the markets, where nearly all asset classes moved higher.

So what should investors expect in 2017?

A report released by WFII in December highlights four themes that the institute’s analysts believe will influence the global economy over the coming twelve months.

The first is what WFII refers to as “the divided recovery,” highlighted by the rise of populist politics in 2016. In the case of the US, president-elect Trump stormed into the White House, promising to make America great again. While some of his campaign promises might boost economic growth, they also risk ushering in an era of inflation and rising interest rates. Trade restrictions could protect some US industries, but hurt others that rely on international supply chains.

The key for investors is to stay diversified so they can benefit regardless of the outcome. If growth accelerates, equities may thrive; if political uncertainty continues, bonds could do well. Sentiment might falter even in the face of stable economic fundamentals, so investors should be prepared to rebalance their portfolios accordingly. And if inflation picks up, as it is universally expected to if Trump’s fiscal policies become a reality, then WFII recommends focusing on quality, medium-term US corporate debt.

The next theme addresses economic growth, and one of the issues the report highlights is the balance between monetary and fiscal policy. Central bank intervention seems to be coming to an end as politicians accept they must bear some of the responsibility for stimulating growth. Trump tapped into this argument during his campaign by promising to spend $1 trillion on infrastructure—even if fiscal stimulus risks expanding the deficit.

More jobs and increasing wages bode well for consumer discretionaries, WFII believes, while infrastructure investment should boost the industrial and IT sectors. On the other hand, WFII anticipates a greater risk of recession in 2017 due to rising debt and inflation.

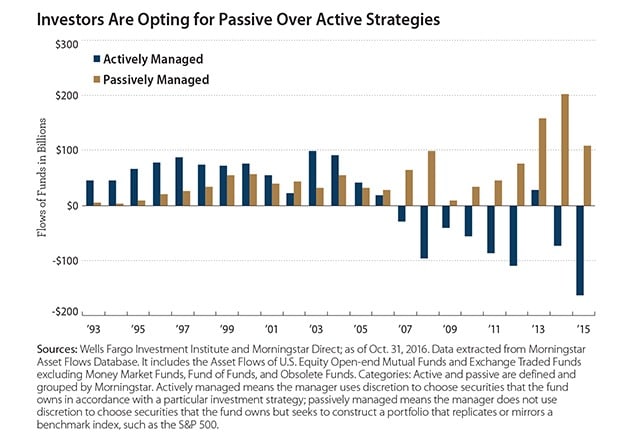

The third theme the report covers is what WFII calls “the agile investor.” The report claims that the main asset classes—fixed income, equities and commodities—could exploit trends such as new technologies, alternative energy or expanding populations. This may present active fund managers with an opportunity to reclaim some ground lost to passive funds over the last few years (see chart). WFII suggests holding a mix of active and passive investments. They also advise keeping a portion of assets in cash or cash equivalents to capitalize on opportunities when they arise.

The final theme WFII sees emerging in 2017 is the demographic shift in the workforce as baby boomers retire. According to the report, this will lead to a massive transfer of wealth—an estimated $30 trillion over the next 30 to 40 years.

“As money flows from an older to a younger generation, we would expect to see some reallocation away from bonds and into growth assets like stocks. This demand could help support stock prices in the coming years. But bonds should also have healthy demand as aging populations around the world continue to invest in income-generating assets,” says Tracie McMillion, head of Global Asset Management at WFII. “Industries that might do well are housing and consumer discretionary, as inheritances may be spent by younger generations with pent-up demand driven by years of student loan repayments.”

The next generation of wealth managers may be at risk, however: Millennials are more inclined to use online investing platforms such as robo advisors than their baby boomer parents, who prefer working with a traditional (human) investment advisor.