The junk market is hurting. Experts predict the pain will continue, with defaults peaking a couple of years from now.

Is corporate credit the new subprime? While mortgage lenders have tightened their wallets since 2008, corporations have been borrowing with abandon, abetted by trillions of dollars in central bank liquidity and investors searching for yield they can no longer find in government bonds or money markets. “Nonfinancial corporate credit is at the nexus of the excesses in this cycle, unlike 20072008, which centered on the US housing sector and banking system,” writes Matthew Mish, senior credit analyst for UBS Investment Bank, in his 2016 forecast.

The average yield on BB paper is 6.4% now. That’s still a pretty low rate, historically.

~ Martin Fridson, Lehmann Livian Fridson Advisors

The public market in high-yield bonds—also known as junk, for their inability to earn an investment-grade credit rating—offers a clear view of those excesses. Investors in junk signaled increasing distress through the second half of 2015. Bloomberg’s High Yield Corporate Bond Index slid by nearly 8% between June 1 and January 1, with most of that loss coming in the last two months of 2015. In mid-December, New Yorkbased Third Avenue Management barred redemptions from a $1 billion junk-bond mutual fund, sending shudders across Wall Street.

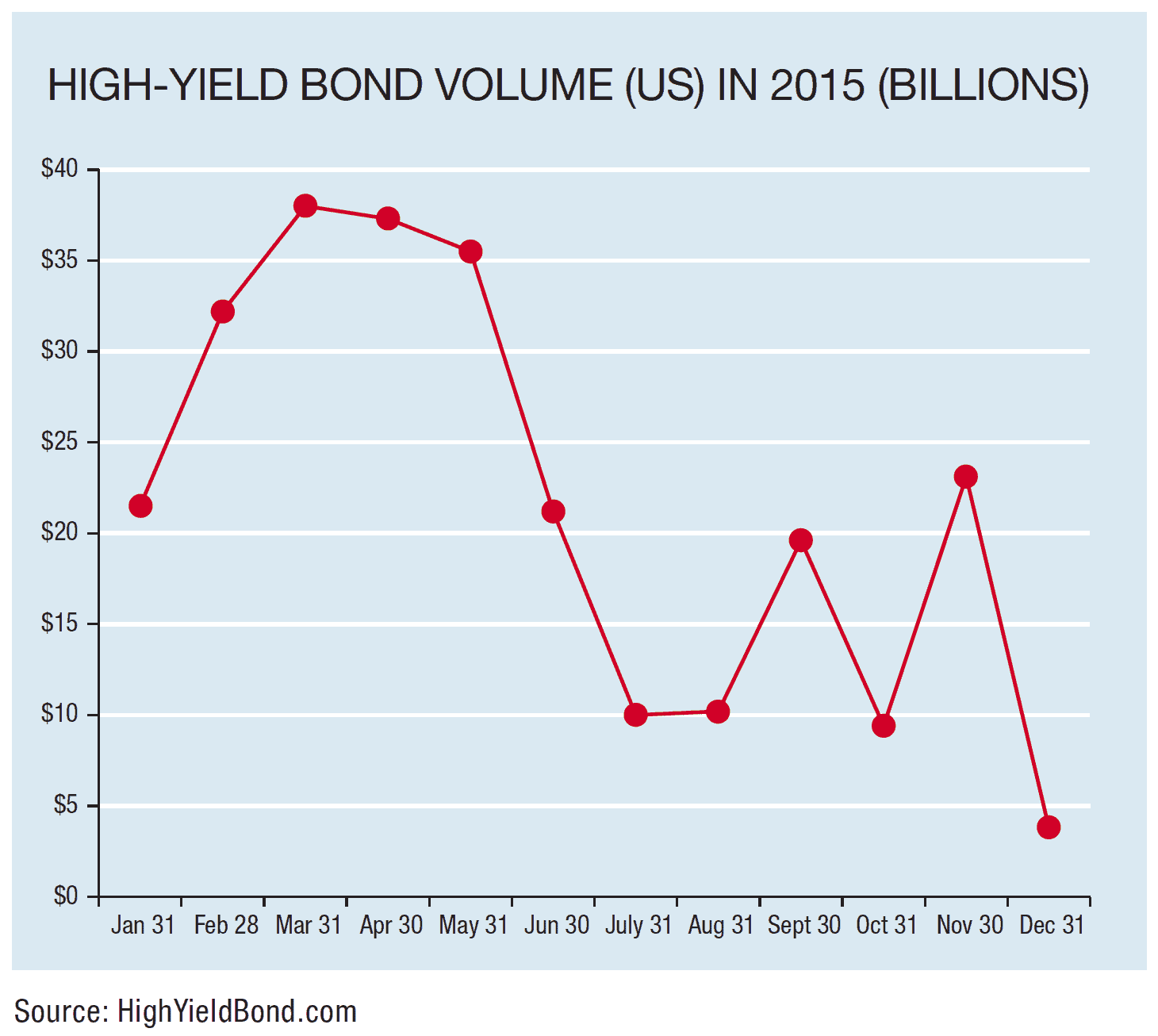

For corporates, nervous investors mean less opportunity to issue high-yield debt and higher interest rates if they do. On average, US companies raised some $12 billion a month in the second half of last year, compared with more than $30 billion in the first half, according to HighYieldBond.com (see chart on page 41). Average yields have jumped by more than 200 basis points for BB-rated issuers, and by 400 basis points for weaker B-rated companies, from their 2014 lows.

Conditions should get tougher still over the next few years, junk watchers say. The corporate borrowing binge that started in 2009 has pushed leverage to a 12-year high for BB-rated companies and to levels not seen since 1999 for the single-B world, UBS reports. Single-B borrowers, on average, owe an intimidating six times annual Ebitda. This overextension will drive defaults from a current 3.5% of the junk bond universe to as much as 6% by the end of 2016, the bank predicts.

Debt-burdened American corporates (and, to a lesser extent, European companies) are sailing into headwinds from the US Federal Reserve, which finally started hiking interest rates last December. The borrowing party has reached its climax, concludes David Riley, head of credit strategy for London-based BlueBay Asset Management, which runs some $60 billion in fixed income funds. “The period when everyone could come to market and have a lark has come to an end,” he declares. “The cost of borrowing for corporate America started rising even before the Fed acted.”

OVERLEVERAGED GIANTS?

Credit distress is rampant among energy companies, which borrowed heavily against the promise of shale oil and gas extraction and are now reeling from what looks like a prolonged price crash. But energy is hardly the only sector that overindulged. Martin Fridson, chief investment officer of New Yorkbased Lehmann Livian Fridson Advisors and a well-known blogger on high yield, offers a list of firms whose bond spreads have ballooned to more than 1,000 basis points over US treasury bills, pricing that indicates a one-third chance of default within a year, he says. Just the first three letters of the alphabet include beauty products icon Avon, Canadian aircraft maker Bombardier and casino owner Caesars Entertainment—a diverse mass of misery.

After oil and gas, retail is the second-most-profligate industry. Eleven retailers defaulted on debts last year, their brick-and-mortar investments insupportable in the online age, and a number of household names like J. Crew and 99 Cents Only Stores were on the ropes as 2016 dawned. Telecommunications and media companies, also frequent users of high-yield finance, are holding up better for the moment. But the worse the market gets, the less bond buyers will discern between good and bad apples, Fridson predicts. “Looking at a long-term average, defaults should peak at about 10%, and you will see very little issuance at that point,” he says.

The good news for CFOs is that the calamity should come to pass gradually. Under the extreme stress of 2008, bonds behaved like equities, with a sudden spike in yields and recovery within a year. But that was an historical anomaly. Previous tightening cycles—for instance, the mid-1980s energy bust and the bursting dot-com bubble in the late-1990s—rolled through the economy over five years or so. The current retraction won’t reach its nadir of 10% junk-bond defaults and virtually closed markets until 2018, Fridson predicts. (He also expects the broader economy to be in recession by then.)

That timeline matches the maturity curve of existing high-yield issues. The remainder of 2016 looks relatively benign on the repayment front, with some $40 billion due from borrowers with a B rating or lower, according to UBS. But that figure jumps to more than $100 billion by 2018 and $150 billion in 2020, when sub-investment-grade borrowers could scramble for financing of any kind.

Deutsche Bank, too, posits a scenario of gradual retreat, in a 2016 outlook written by US credit strategist Oleg Melentyev. “The current credit cycle is old enough and extended itself far enough to be falling right in line with three cycles that came before it in the past 30 years,” he concludes. Deutsche projects a substantial but not crippling 23% decrease in junk-bond issuance across all developed markets this year, to $210 billion. Leveraged loans will contract by 21% to $245 billion, the bank predicts. “This is a taper, not a cliff,” BlueBay’s Riley agrees. “Despite volatility, primary markets have remained open.”

Meanwhile, US investment-grade bonds have come somewhat into vogue among European and Asian investors seeking exposure to the seemingly unstoppable dollar and respite from their own fragile economies, Deutsche Bank reports. “Starting in late 2014, overseas buyers began a US corporate bond shopping spree, adding $11.5 billion a month, on average, over 13 consecutive months, taking down roughly 35% of net supply of US issuer paper,” Melentyev writes.

The bank expects foreigners’ appetite to help steady the investment-grade market after a rough 2015. Bloomberg’s Global Investment Grade Corporate Bond Index sank by 4% last year to a trough in early November, then stabilized as high-yield cratered further. Deutsche Bank expects an increase of 4.5% in US issuance this year to $1.34 trillion, while yields nudge up a mere 10 basis points. The takeaway for borrowers may be to lock in financing at attractive rates now, while they still can. “The average yield on BB paper is 6.4% now,” says Fridson. “That’s still a pretty low rate, historically.”

The only developments that might stop the natural credit-tightening cycle in its tracks are interrelated, experts say. If China rebounds to its former tigerish growth rates, it could drive commodity prices back up. That in turn would ease the finances of the commodity producers that are weighing heavily on bond and loan markets. Absent this unlikely scenario, borrowers will pay the price for the open spigots of the past and the Fed’s path to rate normalization. But when the bottom comes, it shouldn’t come as a surprise.