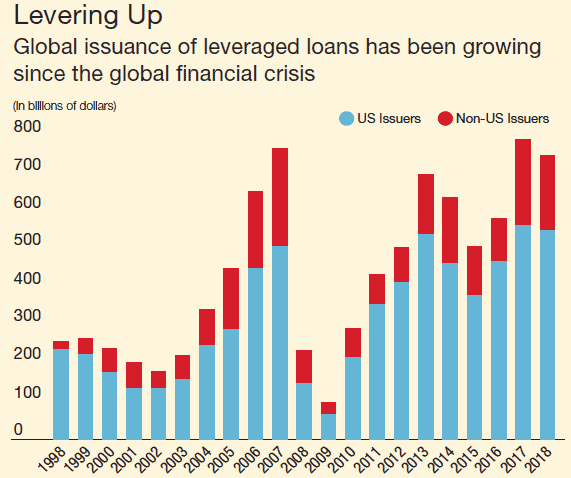

Leveraged loans are hitting highs not seen since 2008.

Coveted by yield-hungry investors when interest rates were still hitting record lows, non-financial corporate loans reached a worrying peak of $1.3 trillion at the end of the third quarter, according to the International Monetary Fund. Speculative-grade companies have been eager to increase their debt; globally, the volume of leveraged loans reached a record $788 billion in 2017, exceeding the pre-crisis high of $762 billion in 2007—and are now nearly double that figure.

U.S. Senator Elizabeth Warren (D-MA) is comparing the plethora of these leveraged loans to the subprime mortgage boom that triggered the 2008 financial crisis. The IMF warns that the trend amounts to a dangerous deterioration in lending standards

“This growing segment of the financial world involves loans, usually arranged by a syndicate of banks, to companies that are heavily indebted or have weak credit ratings,” wrote Tobias Adrian, Fabio Natalucci, and Thomas Piontek of the fund’s Monetary and Capital Markets Department in November IMF web post titled “Sounding the alarm on Leveraged Lending.” “These loans are called ‘leveraged’ because the ratio of the borrower’s debt to assets or earnings significantly exceeds industry norms.”

The U.S. dominates the market, with $564 billion of new loans last year, the bloggers noted, citing Standard& Poor’s and IMF calculations. Most recently, it received a boost from a wave of M&A deals involving a number of well-known companies, including AT&T, Bayer, British American Tobacco, and Campbell Soup Company that have accessed non-financial corporate loans to fund their acquisitions of, respectively, Time Warner, Monsanto, Reynolds American, and Snyder’s Lance. The worry now is that there are so many groups under pressure to reduce their debt level at a time when interest rates are on the raise.

“I am concerned that the large leveraged lending market exhibits many of the characteristics of the pre-2008 subprime mortgage market,” Warren wrote in a letter to U.S. regulators. “These loans are generally poorly underwritten and include few protections for lenders and investors. Many of the loans are securitized and sold to investors, spreading the risk of default throughout the system and allowing the loan originators to pass the risk of poor underwriting on to investors.”