With the renminbi growing in strength, FX trading pivots to Asia at the expense of Europe.

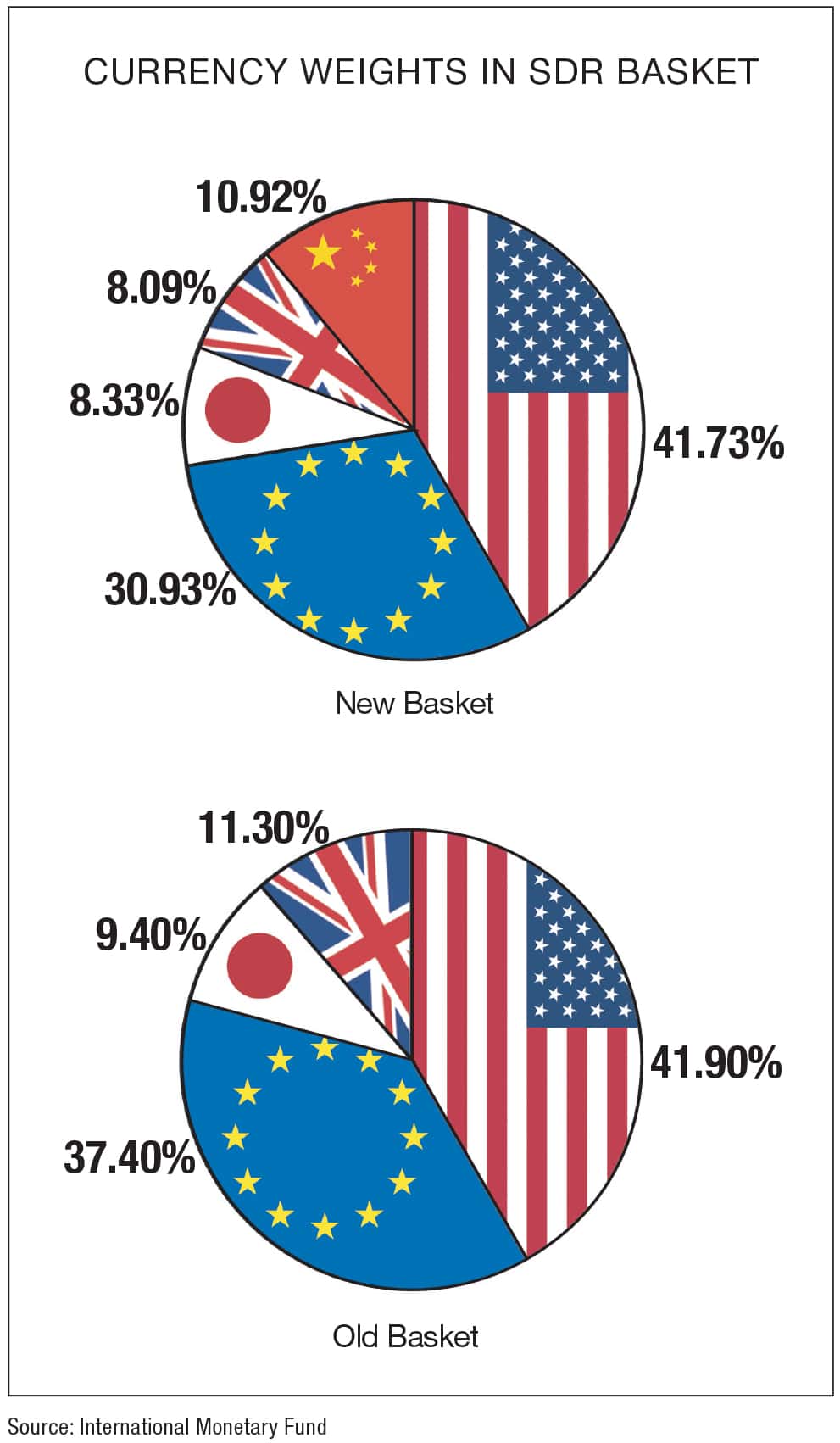

The US dollar remains king in the world’s biggest market, as the rise of Asia’s share in foreign exchange trading, led by China, is coming at the expense of Europe rather than the US, analysts say. When the renminbi joined the International Monetary Fund’s special drawing rights (SDR) currency basket on October 1, becoming the world’s fifth reserve currency, the weightings of the euro and the British pound were reduced significantly, while the dollar’s weighting was little changed.

“Joining the SDR is a momentous occasion for China and the world,” says Marc Chandler, global head of currency strategy at Brown Brothers Harriman. “It is a sign of the rise of China, and the West’s recognition of this. It is also a sign of good housekeeping by the IMF, which is recognizing the strides that China has made.”

The closest comparison may be China’s entry into the World Trade Organization at the end of 2001, Chandler says. “The conditions to join the WTO encouraged China to pursue a reform agenda and gave the domestic modernizers more gravitas,” he says.

For the past 25 years or longer, more goods have crossed the Pacific Ocean than the Atlantic, he adds. Although trading in the renminbi has almost doubled in the past three years, the dollar continues to be used on one side of 88% of all FX spot market trades and 95% of renminbi transactions, according to the Bank for International Settlements (BIS) in Basel, Switzerland. The BIS recently released updated data on the size and structure of the FX market, as it does every three years.

CHINA’S MARKET SHARE SURGES

The latest BIS survey of central banks around the world showed that London’s strong lead in global foreign exchange trading is being eroded. The UK’s market share has fallen to 37% of the global market from 41% in 2013. The euro has also slipped steadily since the beginning of the euro-area sovereign debt crisis in 2010, and the euro is now used on one side of 31% of FX trades, versus 39% in 2010.

London’s share of the FX market could fall further as a result of Britain’s vote to leave the European Union. London faces the potential loss of euro clearing, if France and other EU countries get their way. They want such transactions to be done in the euro area once Britain exits.

Overall, the FX business is pivoting to Asia, with its deep pools of capital, Chandler says. This is reflected in the rise of the renminbi, which overtook the Mexican peso this year to become the world’s eighth most actively traded currency. The emerging markets’ share of global turnover rose to a record 21.1% this year from 18.9% in 2013.

The renminbi now has an average daily trading volume of $202 billion, versus $120 billion in 2013. The Mexican peso’s current volume of $112 billion daily is down from $135 billion in 2013. Singapore, Hong Kong and South Korea follow with the next most actively traded emerging markets currencies.

DOLLAR TO RETAIN DOMINANT ROLE

“Over time, the Asian centers will continue to pick up more activity,” Chandler says. But the renminbi accounts for about 1% of world currency reserves (Canada and Australia have bigger shares) and the Chinese currency is unlikely to become a major reserve currency anytime soon. “Central banks move at glacial speeds,” Chandler says. The dollar has been the leading global reserve currency for many years and likely will remain a safe haven for many years to come, owing to the depth of US financial markets and its well-developed legal framework and public institutions, he says.

Still, China continues to push for greater international use of its currency, which the IMF has deemed to be “freely usable,” meaning that it is widely traded and used to make payments for international transactions. “When countries borrow from the IMF, they will receive renminbi, as part of the SDR,” Siddharth Tiwari, director of strategy, policy and review at the IMF, said in a conference call. He said the internationalization of the renminbi would continue, “together with responsibilities that come with it.” He said a review of the SDR basket is conducted every five years by the IMF’s executive board, or earlier if warranted by developments.

Bringing the renminbi into the SDR has been a long-term goal of China, which has been irritated, along with much of the developing world, by the significant role the dollar plays in the world economy. At the height of the global financial crisis in 2009, China backed Russia’s call for a discussion at the G20 on replacing the dollar as the world’s primary reserve currency. More recently, China has continued to seek an expanded role for the SDR.

Tiwari says the IMF will publish a white paper in 2017 on the evolving role of the SDR, including “market SDRs,” or M-SDRs, which are financial instruments denominated in SDRs. Some M-SDRs were introduced in the 1970s and early 1980s, but they never caught on, because of the lack of a private market in SDRs.

China Construction Bank has forecast that the SDR bond market in China will grow to $7 billion in the next few years. Chinese officials have waived quota restrictions for foreign central banks and sovereign wealth funds.The World Bank recently issued $700 million of three-year landmark bonds denominated in SDRs in China’s interbank market. The so-called “Mulan bonds” will settle in renminbi but will be tied to the performance of the SDR. Priced to yield 0.49%, the bonds were oversubscribed. Similar US Treasuries yield 0.85%, and Chinese three-year notes yield 2.4%.In the case of China, “M-SDRs issued in the onshore market could potentially reduce demand for foreign currency and reduce capital outflows by allowing domestic market participants to diversify their foreign exchange risk,” the IMF said in a staff note for the G20 issued in July. Issuers of such instruments would, in effect, be assuming foreign exchange risk by indexing their liabilities to a foreign currency basket instead of issuing directly in renminbi.

USING SDRS AS UNITS OF ACCOUNT

The IMF staff says there are also potential benefits to using the SDR as a unit of account, and that publishing economic statistics and financial statements in SDR terms could help users identify valuation changes. It says that Suez Canal fees and damages paid by air carriers for lost baggage are examples of SDR-based pricing. China publishes its international reserves data in SDR terms.

The renminbi is unlikely to suddenly become a major reserve asset, however, just because it is now part of the SDR. China’s financial markets need further development, and its institutions, both political and legal, are alien to the West. “In some ways, joining the SDR is a distraction,” says Chandler of Brown Brothers Harriman. “Putting vanity plates on your car doesn’t make it drive faster.” Esperanto may have seemed like a good idea, Chandler says, “but you can’t force it on people.” Central banks have a habit of taking their time, he says, so they probably won’t rush to build up their renminbi reserves.

When is the renminbi likely to join the CLS (continuous linked settlement) network, which could further enhance its international use? “The trajectory for the next phase of renminbi internationalization is primarily driven by China’s reform agenda,” says David Puth, CEO of CLS, the world’s largest multicurrency cash settlement system. “CLS continues to work with market participants and the Chinese authorities with the objective of bringing payment-versus-payment settlement to the Chinese market to mitigate settlement risk.”

Cross-currency settlement risk—also known as “Herstatt risk” after a German bank that failed in 1974—is widely recognized as the most significant systemic risk to participants in the FX market. However, the counter-currency to any renminbi trade (mostly US dollar) will continue to be settled using existing practices bilaterally through correspondent banking. “Therefore, the amount of FX settlement risk in the market overall remains unchanged,” Puth says. “The risk is most effectively mitigated through payment-versus-payment settlement.”

CLS TO EXPAND PAYMENT-NETTING

CLS announced in late September it would develop a payment-netting service for banks’ FX trades that are settled outside the CLS settlement service. The global FX market lacks a standardized payment-netting process for trades not settled within CLS. The existing capability of CLS, combined with its position as a trusted posttrade partner, means that it is ideally placed to deliver a service that will standardize and expand bilateral payment-netting capabilities for the entire FX market, Puth says.

CLS will build a platform using distributed ledger technology for CLS Netting using Hyperledger Fabric, an open-source technology. It is collaborating with IBM to help ensure that the platform meets the requirements needed to deliver a resilient, secure and scalable service.

In the meantime, Asian actors, most especially China’s, will continue to draw interest and drive change in systems worldwide. “We respect the lead of local authorities in setting the agenda and timing for the introduction of their currency in CLS,” Puth says. “[We] are committed to doing everything possible to bring the renminbi into the CLS network of currencies as soon as possible.”

Who Shrank The FX Market?

Turnover in the foreign exchange market has fallen for the first time in 15 years, although more than $5.1 trillion is still traded on an average daily basis. That makes FX the largest market in the world by far.

Spot market FX trading fell to $1.7 trillion in April 2016 from $2.0 trillion in April 2013, according to the Bank for International Settlements trienniel survey. One reason for the 19% decline is that banks have pulled back from the market, since the US’s Volcker rule—which is aimed at US markets but has international ramifications—bans banks from trading currencies on their own behalf.

Regulatory changes in the wake of the global financial crisis of 2008–2009 and the more recent FX market-rigging scandal have transformed the industry. Chat rooms have gone silent, and traders are less willing to take risks.

Risks remain in the market, however, as demonstrated by the collapse of the British pound following the UK vote to leave the EU. Corporations worldwide have awakened to the need to protect themselves from such events.

In a survey of 133 global corporations, consulting firm Deloitte found that corporate hedging strategies are mainly focused on protecting cash and minimizing volatility in income statements. The biggest challenge, cited by 56% of corporate treasurers, was “lack of visibility of FX exposure and reliability of forecasts.”

Swift: Bitcoin Won’t Crowd Out Fiat Currencies

Virtual currencies such as bitcoin are unlikely to crowd out fiat currencies, according to research by the Swift Institute. The price impact of speculators in virtual currencies adversely affects their value as a medium of exchange, says the paper by researchers in South Korea and Australia.

Bitcoin is mainly used as a speculative investment, and there is no correlation between bitcoin and traditional asset classes, the paper says. The design and size of the bitcoin market deprives the currency of its intended use, it says. However, if bitcoin were to catch on globally, the paper says, it could affect the implementation of monetary policy, “as its decentralized and independent nature makes regulatory oversight difficult.”

Meanwhile, Goldman Sachs wants to use blockchain technology to trade foreign exchange. The investment bank filed for a US patent for a real-time FX trading system that uses authentication techniques for electronic signatures. Goldman says there is a need for a system that can process transactions quickly without sacrificing the privacy of the parties involved.