With new EU regulations on financial intermediaries (MIFID II) looming, wealth managers and private banks face a busy 2017. A new report highlights some of the biggest opportunities and challenges.

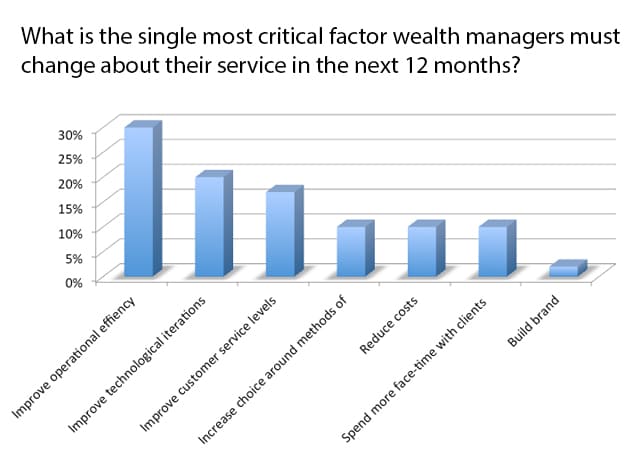

The most critical issue facing the UK’s wealth managers and private banks in 2017 is the need to improve operational efficiency. That’s according to a recent survey carried out by securities consultancy Goodacre UK exploring how the wealth sector plans to deal with a host of regulatory requirements and market reforms coming into force in the new year.

Nearly 70% of respondents believed using a single custodian and fund processing provider would help them add value. While reducing operating costs was the priority, enhanced customer security and risk management were also cited as ways to function more effectively. Some wealth managers reported unnecessary levels of risk in their current provider’s infrastructure, so there was a bias towards bigger industry players filling this role, as they offer deeper expertise and greater security for customer assets.

A third of those surveyed thought an integrated execution, settlement and custody solution would benefit their firm (a third already use such a service). Again, cost savings, for example lower fixed overheads as a result of fewer support staff, was mentioned as the main reason.

“What we found is that firms used different custodians in different areas in the past,” explained Stephen Pinner, Goodacre’s managing director. “Lots of these arrangements have stayed in place, even though you can now use global custodians. With time running out to implement changes ahead of MIFID II, integrated solutions are increasingly in demand.”

The remaining third of respondents were reluctant to outsource due to concerns about loss of control and the quality of the service providers. Nonetheless, the report predicts that outsourced post- trade settlement will eventually replace back office operations at most wealth managers.

Meanwhile, 29% of respondents considered new product development to be one of the biggest opportunities facing the sector over the next three years. These new products are expected to focus mainly on enhancing the client’s user experience by providing better customer reports and improving access on mobile devices. Technology was also seen as an opportunity, particularly the way it could help wealth managers meet compliance requirements and monitor risk.

Among the obstacles mentioned, regulatory issues (chiefly MIFID II) were the leading concerns. Respondents reported that keeping up with new regulations was the greatest challenge, followed closely by the associated costs—some wealth managers still rely on manual fund processing due to a historic lack of investment. The report suggests firms will address these concerns by automating their processes.

Other obstacles brought up by respondents included greater competition (13%) from the likes of robo advisors, and cybersecurity threats (9%), highlighted by the attacks on prominent financial institutions such as HSBC.

The report also draws attention to a trend towards consolidation in the UK wealth management sector. It argues that firms with less than £8 billion AUM are likely to become acquisition targets in 2017 for bigger players seeking to expand. This could suit smaller companies which may prefer to sell out rather than invest in updating their infrastructure.

“What we think is going to happen in the next year or so is the number of firms will fall but the size of the firms will increase,” said Pinner. “Unless you’ve got a pretty strong balance sheet, you’re going to struggle to participate in this market. Even some of the older wealth managers might be up for grabs in the next 12 to 18 months.”

Indeed, this trend has emerged over the last couple of years—124 firms were involved in M&A activity in 2015, compared to 83 in 2014.