ANNUAL SURVEY AND AWARDS

By Michael Shari

Counterparty risk trumps pricing as criteria for picking derivative providers. Wall Street is retaking market share from European rivals

Never underestimate the sleight of hand with which the fast-paced derivatives industry can change directions. The past year saw the stunning reversal of a trend that took root in the financial crisis of 2008, when the collapses of Lehman Brothers and Bear Stearns proved that counterparty credit risk could not be taken for granted. Then the pricing of options, futures, swaps and other products became the most important criterion in picking a derivative provider. Clients of Wall Street banks flocked in droves to European rivals that lured them in with lower commissions and narrower spreads. Among the biggest beneficiaries were Credit Suisse, Deutsche Bank and BNP Paribas.

But this year, two unforeseen trends have conspired to turn the clock back toward a familiar status quo that favors Wall Street icons, according to hedge fund traders, risk managers at financial institutions, corporate treasurers, securities analysts and data gatherers who provided information to Global Finance in our annual derivatives awards.

First, end users of derivative are now placing more emphasis on counterparty credit risk than they did last year. Europe’s sovereign debt crisis has cast the continent’s financial supermarkets in an unfavorable light. Forgotten are the days when panic-stricken American banks rebuilt their balance sheets by selling their own equity to sovereign wealth funds. Now traders believe it would be easier to bail out an American bank than a French or even a German one. As a result, traders and risk managers are saying that they will not open any new counterparty relationships with European banks. Rather, they are trading with the same American banks that they once complained were gouging them.

Second, Wall Street is playing to the prominence of pricing as a criterion in selecting derivative providers. The sales departments of American banks are winning back clients by improving pricing, particularly in equities, commodities and foreign exchange (FX).

In separate interviews, derivatives sales managers at Goldman and JPMorgan Chase admitted that they had tightened pricing to gain market share. Goldman has seen so many clients return to the fold—and new ones climb aboard—that it edged out Credit Suisse as last year’s preferred provider of equity derivatives in North America.

RISING STAKES

As providers continue to compete for market share, the stakes are rising with confidence deteriorating in the global economic recovery. Competition is expected to become particularly brutal in the equity markets of the US and Europe, where there are simply fewer investors to sell to. Capital has evaporated from stock markets since they went into freefall last summer. “If you are not investing period, then you are not going to say, ‘Let’s hedge this out’,” says Jay Bennett, a consultant at Greenwich Associates, which ranks derivative providers annually based on client surveys. This decline follows a gradual tapering off in the use of derivatives in general. According to banks in the 43 countries that report to the Bank for International Settlements, notional amounts outstanding in derivative contracts across all asset classes fell slightly from $603.90 billion in December 2009 to $601.05 billon in December 2010.

“There has been a retreat from equity markets,” admits Peter Selman, co-head of global equity derivative trading at Goldman Sachs. “But generally speaking, the people who now hold equities are more active in derivatives.” That reduced pool of clients may well find itself one of the most contested battlegrounds between derivative providers in the year to come.

REGULATORY OVERHAUL

But the overriding source of distraction in 2012 will not be one of market volatility. Rather, it will be regulatory. Derivative providers are spending inordinate amounts of time assessing the potential impact of rules that are at various murky stages of formulation on both sides of the Atlantic.

“There has been a retreat from equity markets. But generally speaking, the people who now hold equities are more active in derivatives”

—Peter Selman, Goldman Sachs

Regulators are determined to make derivatives transactions more transparent in an effort to prevent banks from accumulating exposure to undisclosed risks that become apparent only after it’s too late—which is what happened with US mortgage-backed securities in 2007 and with sovereign debt in the peripheral nations of the Eurozone this year. And providers want greater clarity around the sprawling 848-page Dodd-Frank Wall Street Reform and Consumer Protection Act, on the basis of which the Securities and Exchange Commission and the Commodity and Futures Trade Commission have proposed rules on how derivatives transactions should be reported, executed and cleared.

A similarly fraught rule-making process is underway in the European Parliament. Among the most contentious issues is the extent to which the new rules will force trades that are now executed in the privacy of the over-the-counter market (OTC) onto exchanges and swap execution facilities where pricing will be completely transparent. Providers are lobbying hard to keep the pricing of large block trades out of public view on grounds that it would impair their ability to make markets in certain products. Another issue is that it’s still unclear how large a trade would have to be to be considered a block trade under the new rules.

“Regardless of how it’s traded, you would not necessarily want to have the pricing disclosed very soon after a trade is done, so getting the block trade levels right is going to be a real challenge,” says Robert Pickel, CEO of the International Swaps and Derivatives Association (ISDA). Whatever the impact of the new rules may be, derivative desks that invest heavily in the infrastructure required to trade over exchanges could find a more regulated OTC market to be highly lucrative.

In recent months, Goldman Sachs has found that investors who have never invested in OTC derivatives are becoming first-time users of Goldman-branded equity derivatives on exchanges, where they’re more comfortable with transparent pricing and the elimination of counterparty risk. Small wonder JPMorgan Chase’s FX derivatives business is making IT investments that are intended to prepare for a variety of possible regulatory outcomes. As competition heats up, such investments could become essential to a winning strategy.

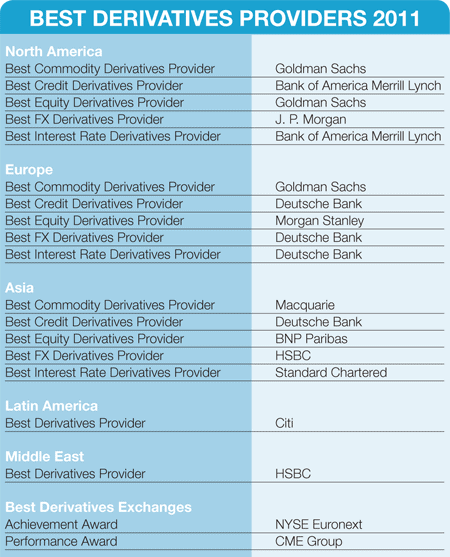

NORTH AMERICA

BEST COMMODITY DERIVATIVES PROVIDER

Goldman Sachs

Goldman Sachs’ dominance of the North American commodity derivatives market has solidified while violent fluctuations in commodities prices—notably in oil, gold and cotton—are making it harder than ever for commodities producers to predict revenues and for corporates to plan their expenses.

Unlike many banks that have expanded and contracted their commodities desks over the past decade, Goldman has consistently built up its derivatives business. A Greenwich Associates survey of 124 US corporations in June gave Goldman high marks for service quality in over-the-counter (OTC) energy derivatives.

Goldman does not emphasize product innovation in commodity derivatives, however. “Beyond the institutional relationship, it is important to recognize that the customer is a human being on the other end of the phone,” says Peter O’Hagan, global head of commodity sales at Goldman.

BEST CREDIT DERIVATIVES PROVIDER

Bank of America Merrill Lynch

The credit derivatives business of Bank of America and Merrill Lynch is enefiting from a perception among clients that the megamerger that created this financial supermarket in January 2009 was actually well managed despite the political controversy that surrounded it. The bank’s advantage, clients say, lies in the strength of the legacy BofA brand in the credit derivatives space.

In a survey of investment firms by Orion Consultants measuring numbers of clients and transaction volumes, Bank of America Merrill Lynch ranked first in investment-grade credit default swaps during the 12 months through July this year. The bank ranked second in high-yield credit default swaps (CDSs).

Traders and risk managers interviewed for this article said they preferred BofA Merrill Lynch over its competitors because it has a broader product line than some of its closest competitors, particularly in mortgage derivatives.

BEST EQUITY DERIVATIVES PROVIDER

Goldman Sachs

Goldman Sachs was a prime beneficiary of a stark reversal in perceptions of counterparty risk that is framing Wall Street banks in a far more favorable light than European ones. In addition, Goldman has improved pricing on equity derivatives transactions to compete with European banks that had taken away some of its market share—and hedge fund traders say it’s working.

Goldman is also profiting from a concerted effort by its corporate clients to cut costs and hoard cash. As corporations examined ways to spend that cash and found their own stock trading to bargain-basement prices in a bearish market, they flocked to Goldman for a structured buyback product that the bank had built from scratch in 2003. It allows clients to buy their own stock through Goldman, which acts as a counterparty, below a volume-weighted average discount.

Now Goldman is investing heavily in the electronic trading of equity derivatives on exchanges, where first-time users of such products are starting to trade actively with the bank, according to Peter Seccia, who supervises North America equity derivatives sales for Goldman.

BEST FX DERIVATIVES PROVIDER

J.P. Morgan

J.P. Morgan took market share in FX derivatives away from some of its more aggressive European competitors in North America in the second half of the year after it tightened pricing, started managing relationships with clients better and improved its risk management. In general, the bank has benefited from a perception of superior counterparty credit risk, compared with European banks.

Spending more time managing the expectations of corporate clients and hedge funds makes all the difference for J.P. Morgan’s FX options traders and salespeople. Gone are the days when clients had 15 minutes to ponder a quote on an FX option. This summer prices were known to move several bid-offer spreads in that period of time.

J.P. Morgan’s traders now keep margins razor-thin thanks to a risk management and trading system, Athena—which weaned them off outmoded Excel spreadsheets.

BEST INTEREST RATE DERIVATIVES PROVIDER

Bank of America Merrill Lynch

Just as it has in credit derivatives, Bank of America Merrill Lynch has outshined many of its competitors in interest rate derivatives since this monolithic institution was created in a historic merger nearly three years ago. Building on the strength of Bank of America’s legacy interest-rate derivatives business and the unparalleled reach of Merrill Lynch’s derivatives sales teams, the bank has wooed new clients and kept old ones loyal with a combination of competitive pricing, superior market-making and first-rate service. “They do a better job,” says a trader at a hedge fund.

The bank’s interest-rate derivatives business is also demonstrating a penchant for innovation. Earlier this year, BofA Merrill Lynch launched an E-Sea index product with a long-short forward rate bias, in both funded and unfunded forms, for retail distribution.

The bank is preparing for OTC interest-rate derivatives to be cleared on exchanges, which is a costly trend that regulators on both sides of the Atlantic are strongly encouraging.

EUROPE

BEST COMMODITY DERIVATIVES PROVIDER

Goldman Sachs

Goldman has brought the same consistent approach to Europe’s commodity derivatives market, along with a trademark focus on customer service, that has given the bank an advantage over its competitors in the US in a year of extremely wide fluctuations in commodity prices.

Goldman has used Europe’s sovereign debt crisis to its advantage in taking market share from its local competitors. The bank is reaching out to corporate clients in Greece, Portugal and other peripheral European nations where the pressure on sovereign ratings is placing unprecedented strains on the ability of even well-managed companies to finance themselves. More than ever before, corporate clients are in the market for risk management solutions, and in a stark reversal of perceptions of the counterparty risk of Wall Street banks a year or two ago, Goldman now has a distinct advantage over European banks that are scrambling to take risk off their balance sheets in response to the crisis. Clients are placing a premium on Goldman’s willingness to put its own capital at risk to provide liquidity, as well as the quality of the market intelligence that its traders impart over the phone.

BEST CREDIT DERIVATIVES PROVIDER

Deutsche Bank

Deutsche Bank remains the preferred credit derivatives provider in Europe, even though low volumes and widening credit spreads caused what Deutsche chief financial officer Stefan Krause gingerly describes as “substantially lower revenues in flow credit” for the quarter ended September 30. Yet for clients who are using derivatives to hedge against the risks of investing in a bond market that is being violently shaken by Europe’s sovereign debt crisis, Deutsche stood out by continuing to execute even the toughest of trades while maintaining its characteristically mpetitive pricing.

The bank dedicated entire research teams to the pursuit of tail-risk hedges that allowed clients to secure credit protection without having to pay punitive up-front costs. During the quarter, Deutsche executed nearly a quarter of all trades in CDSs. “We differentiate ourselves by executing for clients in tough markets,” says Antoine Cornut, European head of credit trading at Deutsche.Earlier this year the bank expanded the range of contracts it trades electronically.

BEST EQUITY DERIVATIVES PROVIDER

Morgan Stanley

Morgan Stanley has built a highly competitive equity derivatives business from the client relationships of its equity cash and prime brokerage operations in Europe. It has expanded aggressively by serving a wide variety of clients, from hedge funds to manufacturers, with a full spectrum of products, from plain-vanilla listed derivatives to OTC contracts and structured products.

“By combining all the flows, you are better positioned to provide good pricing, good ideas and market intelligence,” says Luc Francois, Morgan Stanley’s global head of equity derivatives in London. He says that the bank has gained market share over the past year mainly with consistent pricing even when the equity markets turned volatile this summer.

Morgan Stanley is also selling new products through European private banks that cater to demand for yield among high-net-worth individuals. In March, for example, it launched Accento, a structured equity derivative with a targeted return of as much as 8% annualized over its five-year maturity.

BEST FX DERIVATIVES PROVIDER

Deutsche Bank

Deutsche Bank is still the favored FX derivatives provider in Europe, where the capacity of FX houses to meet the needs of their clients to hedge against currency risk in the embattled eurozone is being stretched beyond tested limits. Deutsche was better equipped to cope with these market conditions thanks to the global scale of its FX derivatives business, which processes more than 1.2 million client requests electronically per year. Deutsche was thus better positioned to offset risk internally by matching up clients with opposing views instead of relying on the interdealer market.

Deutsche’s FX derivatives business continued to innovate in 2011. Deutsche overhauled its back-office infrastructure and redesigned its electronic trading platform, which was relaunched in September as Autobahn 2.0. Sales teams were reorganized.

Earlier the bank launched dbOverlay, a new product designed to allow asset managers and corporate investors to significantly reduce the time and cost of hedging FX risk on their international portfolios and share classes. “Since volatility looks set to become an entrenched feature of the FX market for years to come, we expect continued demand for this popular product,” says Kevin Rodgers, global head of FX spot, e-trading and derivatives.

BEST INTEREST RATE DERIVATIVES PROVIDER

Deutsche Bank

Deutsche Bank was early to predict that Greece’s sovereign debt woes would eventually reshape Europe’s markets, and its structured credit desk has stayed open to focus on bespoke, or custom-made, solutions for clients. Deutsche has faced the challenge of an increasingly one-sided market where the vast majority of its clients are now sellers of peripheral European sovereign credits by providing them with at least some degree of liquidity or hedging services.

The bank has continued to solidify its position as Europe’s interest-rate derivatives market leader thanks largely to risk management and product innovation, and has also expanded a couple of derivative franchises—one in inflation options and another in Treasury inflation-protected securities. In February, Deutsche was early in clearing transactions designed to conform with Dodd-Frank regulations.

“As the industry adjusts to the new regulatory environment, Deutsche Bank expects to continue leading new developments on that front,” says Wayne Felson, head of European rates at Deutsche Bank.

ASIA

BEST COMMODITY DERIVATIVES PROVIDER

Macquarie

Australia’s Macquarie Group retains its position as the preferred commodity derivatives provider in Asia, where it has continued to expand aggressively this year. Founded in 1969, the bank grew up with Australian mining and energy companies by financing their exploration and production projects across the region.

They became the client base for Macquarie’s commodity derivatives business, which expanded from metals and energy into agricultural commodities and grew to include other corporate and financial investors.

Macquarie’s derivatives business is fundamentals-driven, not product-driven, according to Walter Pye, senior managing director for fixed income, currencies and commodities at Macquarie in New York. Unlike their counterparts at some other banks, Macquarie’s traders work with clients to identify the projects they need to finance—or risks they need to hedge—before offering them a derivatives product.

BEST CREDIT DERIVATIVES PROVIDER

Deutsche Bank

Deutsche Bank built its Asian credit derivatives business from its cash and bank loan operations in China, Hong Kong, India, Singapore and Taiwan. With some loans it has made to companies that have issued bonds, Deutsche Bank packages the exposure through CDSs on the underlying bank guarantees.

Demand for such products helped drive up Deutsche Bank’s credit derivative volumes by 25% this year over 2010. In addition, investors sold CDSs—notably Chinese sovereign CDSs—to add risk during the volatile months of August, September and October.

Another opportunity came this year with a new offshore market for renminbi, China’s currency. Deutsche Bank was quick to launch index products for the new market in Hong Kong. Then it became active in renminbi credit risk hedges, akin to CDSs, in November. Now the bank is gearing up for the launch of India’s first onshore CDS market.

“We have markets starting to take off in a few of the larger economies like China and India,” says Sanjay Garodia, head of flow credit trading for Asia at Deutsche Bank in Singapore.

BEST EQUITY DERIVATIVES PROVIDER

BNP Paribas

BNP Paribas has grown from strength to strength in equity derivatives in the Asia-Pacific region since 2008, when the French bank grew market share by keeping its pricing consistent. BNP Paribas also launched several new products, becoming the first bank in Asia to launch single-stock volatility swaps, which are forward contracts on the future realized price volatility of those stocks. That innovation led the bank to launch dispersion swaps, which are packages of single-stock volatility swaps that BNP Paribas sells in Hong Kong, Japan and Australia.

Then came a range of “light exotic” derivatives, such as options on variance and dividends. BNP Paribas even offers swaptions on volatility and dividends in Asia.

The light exotics were particularly in demand in August and September, when equity markets roiled around the world. “People in the investment community appreciate that these products allow them to benefit from different dislocations in the markets,” says Valery Bloud, head of flow equity derivatives sales for Asia Pacific at BNP in Hong Kong.

BEST FX DERIVATIVES PROVIDER

HSBC

Hongkong and Shanghai Banking Corp. dominates the FX derivatives market in 19 Asian countries, where its diverse client base ranges from hedge funds to corporations of all sizes. The result is a vast internal pool of Asian currencies that it can offer its customers even when liquidity appears to be drying up. “This is what really gives us an advantage over everybody else,” says Hossein Zaimi, head of FX and precious metal derivatives for Asia-Pacific at HSBC.

This year HSBC emerged as a pioneer in a new market that China created for an offshore deliverable version of its currency, the renminbi, which foreign investors can buy in Hong Kong and spend on the mainland. HSBC is already the largest issuer of offshore renminbi-denominated dim sum bonds. It also issues structured notes in renminbi that pay a return linked to a basket of emerging-markets currencies instead of a fixed yield.

BEST INTEREST RATE DERIVATIVES PROVIDER

Standard Chartered

Standard Chartered Bank’s interest rate derivatives business stands out among its competitors for putting its own balance sheet at risk in countries where Asians are emerging as the most active foreign investors. Plain-vanilla flow swaps are in great demand and the bank’s corporate clients are extending loan tenors. As a result, the bank’s interest rate derivatives business grew six-fold between 2008 and 2010. During the first half of this year, volumes grew another 25% to 30%.

In Hong Kong the bank issued the first-ever interest rate swap denominated in renminbi for an onshore corporate client. In Pakistan the bank issued a cross-currency swap for a state-owned shipping company for less than half the loan spread of a foreign-currency loan.

“We are onshore in all of these places, and this is a sign of our commitment in resources, including our balance sheet, to our footprint markets,” says Nitin Gulabani, global head of rates & FX at Standard Chartered in Singapore.

LATIN AMERICA

BEST DERIVATIVES PROVIDER

Citi

Citigroup has had a presence for more than a century in Latin America, and it has built up the region’s largest derivatives business with its broader relationship clients. Citi’s largest markets for derivatives are Brazil, Mexico and Colombia, in that order.

But Citi’s advantage is the global connectivity that gives its clients in Latin America access to its derivatives solutions hub in New York and local derivatives teams in countries around the world. About half of Citi’s clients are multinationals that need to hedge their foreign-exchange exposure in Latin America. The other half are Latin corporations that are growing fast, becoming global and now requiring the same derivatives solutions as the multinationals.

“It’s a two-way road,” says Flavio Figueiredo, Citi’s head of corporate derivatives sales for the Americas. “We can connect global clients with local markets, and we can customize global products and adapt them for local clients.”

MIDDLE EAST

BEST DERIVATIVES PROVIDER

HSBC

With more than 40 people in 11 dealing centers across the Middle East and North Africa, HSBC’s derivatives business thrived in the wake of the global financial crisis by keeping commissions low, keeping spreads narrow and generally taking business away from arch-rival Standard Chartered Bank.

This year HSBC got another boost from the political uprisings that swept North Africa and the resulting spike in oil prices. Much of the region’s derivatives business that wasn’t already being done in the United Arab Emirates migrated to this safe haven, where virtually no unrest had occurred. Now 75% of HSBC’s regional derivatives business is done in the UAE, where the bank has its regional headquarters. “High oil prices have been very good for us this year,” says Praveen Gupta, regional head of corporate sales for the Middle East and North Africa at HSBC.

EXCHANGES

ACHIEVEMENT AWARD

NYSE Euronext

In the short span of four years since it was created through a transatlantic merger in April 2007, NYSE Euronext now sets the global standard for trading securities of all asset classes, including a full range of derivatives, on a single universal platform. “The architecture of the technology for all of our markets is the same, be they cash or derivatives,” says Garry Jones, EVP and head of global derivatives at NYSE Euronext in London.

This achievement is driving the growth of trading over the group’s derivatives exchanges, which now make up about 36% of revenue and about 50% of the company’s profit. The group was trading about 9.5 million derivatives contracts a day in late October, up about 7% from 12 months earlier—making it the largest after CME Group, says Jones. The proposed merger with Deutsche Börse will only increase its clout.

PERFORMANCE AWARD

CME Group

When the world’s capital markets went haywire in late August, corporate and financial investors alike rushed to hedge their risk in the relative predictability of centralized exchanges. CME Group, the global giant created through the mergers of the Chicago Mercantile Exchange, the Chicago Board of Trade and the New York Mercantile Exchange, saw a record level of interest in all asset classes, from agriculture and energy to interest rates and FX.

From January 1 to October 26, 2011, CME’s average daily volume rose by 14% to 13.87 million options and futures contracts, and total volume reached 2.87 billion contracts. Technology enhancements and new products are driving the growth of derivatives trading and clearing at CME—such as weekly US Treasury contracts, launched in January, and Euribor contracts based on short-term European interest rates, launched in October.