After the Revolution

With the shockwaves from last years election debacle subsiding, Ukraine is poised to embark on a phase of explosiveand potentially traumaticgrowth.

|

In the space of just six months, the worlds view of Ukraine has changed beyond recognition. Before November 2004 few people knew much about the country, and those who did saw it as a politically corrupt backwater that was too close to Moscow for comfort. But the Orange Revolution has put an end to such characterization. Now the talk is of eventual membership in the EU and of financial reform.

The man at the heart of this transformation is Viktor Yushchenko, a former governor of the central bank of Ukraine, who received an award from Global Finance in 1997 as one of the six best-performing central bankers in the worlda fact he cited in his official presidential campaign biography. Yushchenko is no stranger to power. In addition to his stint as central bank governor, he was Prime Minister from 1999 to 2000 and was widely credited with laying the foundations of Ukraines current economic success.

However, it is his most recent actions that have inspired the world. Having been denied power in the almost-universally condemned November 2004 presidential election, Yushchenko galvanized the people into action. Thus, more than a decade after the fall of communism, Ukraine was once again protesting for its freedom. In a re-run of the election in December, Yushchenko won and, despite being deliberately poisoned during the campaign, took office to global applause.

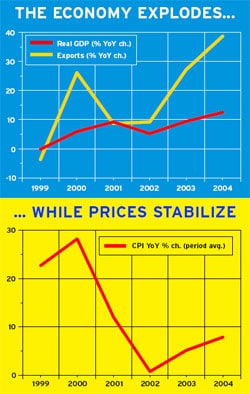

Of course, Yushchenkos election is not a panacea. According to RZB, the investment banking arm of Raiffeisen Bank, economic growth slowed considerably in late 2004 and early 2005. The country remains vulnerable to a fiscal deficit of 6%-7%not least as a result of last-minute election-related increases in pensions and minimum salariesunless serious action is taken to stem it.

But the problems should also not be overstated. In 2004 Ukraines GDP grew by 12%, and it is likely to grow by 8% this year, according to RZB. German investment bank WestLB more conservatively estimates growth of 6.5%still impressive by European standards. Similarly, the government has promised to accelerate its privatization program, which should bring the budget deficit down to 2%. Inflation is expected to fall from 12.3% in 2004 to 9.5% in 2005 and 5.5% in 2006, according to WestLB.

On May 11 Standard & Poors raised its long-term foreign currency sovereign credit rating on Ukraine to BB- from B+, reflecting improved creditworthiness and an enhanced political and policy environment, according to credit analyst Helena Hessel. She notes that Yushchenko advocates transparency, the rule of law and democratic values, which over time should lead to the implementation of political, institutional and structural reforms that are necessary to transform Ukraine into a country with an open, democratic political system and a market-based economy.

Tomasz Balamut, economist in the treasury department at WestLB, says there are a number of explanations for Ukraines growth. Part of the reason is because the country experienced a deeper recession than most other post-Communist countries, and when the stabilization of the late-1990s arrived, there was further to climb. In addition, Ukraine has also benefited from the strong market for steel, which is the countrys main industry.

|

Opportunities and Problems |

|

Despite a slowdown, Balamut remains optimistic about prospects for GDP growth and says the broad growth of both the export and domestic consumption markets bodes well for the future. This is certainly a great place to invest in terms of accessing growth, he says. The wages are around $120 a month, making it comparable with China but with the German market on the doorstep. Already we are seeing Polish manufacturers moving factories to the Ukraine to take advantage of wage rates. Its not an easy step for everyone though; you would need to be confident of being able to cope with Soviet-style bureaucracy, he adds.

Indeed, the slow pace of reform at the grassroots level remains a problem. The Ukraine has a big challenge in order to make conditions more attractive for investors. It is at the bottom of FDI per capita tables, says Balamut. There is a real need for better administration and decision-making procedures in government. Similarly, while the tax code and legal structure of Ukraine appear attractive to foreign investors, there continue to be problems with implementation and government organization. A further disincentive to investment is the fact that the local currency, the hryvnia, is not fully convertible. Gerhard Lechner, country analyst at RZB, says that although the government has yet to make full convertibility a pledge, it is generally accepted to be a long-term objective. In the meantime, investors must cope with a steadily appreciating currency and the prospect of a change in policy in the future. The currency has appreciated in recent years primarily because ferrous and non-ferrous metals account for a huge percentage of Ukraines economic product. As a result of the strong demand for metals, the countrys current account surplus has ballooned from around 4% of GDP in 2000 to 9% last year. That has had a predictable effect on the hryvnia currency, which has appreciated from around 5.44 to the dollar in 2000 to 5.33 last year to around 5.20 this year. WestLB is predicting a rate of 5.15 by the end of the year, but some commentators say an official change to a 5.10 rate is possible. If the currency is revalued, there is likely to be a decline in the rate of growth, according to Lechner. There is a great need to revalue in order to slow inflation, but it would affect growth, which in a country as poor as Ukraine is desperately needed, he says. Its a tough trade-off. Ukraine does have an attractive tax environment for investors, however. The country has recently followed the trend across Central & Eastern Europe in introducing flat taxes for both individuals (13%) and corporates (25%). Balamut says that there is no question that either would change in the future. |

Industry and Privatization

|

Privatization is likely to remain cautious, and efforts will focus instead on re-negotiating deals struck under the previous government. The government plans to raise $1.4 billion through the revision of prior privatizations, which are tainted by the corruptionof the previous government.

While this policy played well during the presidential election, it is fraught with danger. Not only could the proceedswhich the government requires to lower its deficitbe limited as a result of court actions, but the policy could undermine confidence in investing in the country. There is certainly a risk with regard to foreign investors, says Lechner, but the risk should not be overestimated. For example, there is far more need to be concerned about inflation than re-negotiated privatizations.

A test case currently going through the courts involves the privatization of the giant Kryvorizhstal steel mill in 2004. In April the court gave an initial verdict that the privatization was illegal because the price paid for the assets by Metallurgical Union Corporation, part-owned by the son-in-law of former President Leonid Kuchma, who has been widely discredited as corrupt, was lower than other bids from international companies. Yushchenko had made the recovery of the mill an election issue in November.

At the beginning of May the court reversed its decision in the case, which had been brought by a group of private investors. However, the government is also bringing a lawsuit against the current owners that has yet to be heard and could result in myriad re-negotiations of earlier privatizations. As the lawyers for the Metallurgical Union Corporation note, the case could have implications for more than 3,000 privatizations.

Unsurprisingly, Sergiy Vlasenko, one of the lawyers, notes that particularly after the Orange Revolution, it is very important not to take decisions in haste which could seriously undermine the stability of the economy by weakening foreign investors who already have a presence in Ukraine or by frightening foreign investors who are looking to invest in Ukraine in the coming months. Whichever way the case eventually goes, the uncertainty could have an impact on investment.

The wild card with regard to Ukraine is the EU. Officially, the country is not a potential candidate for entry, but already there have been numerous calls for the long process of accession to begin. Certainly, many feel the promise of membership could help entrench economic and political reform. Even before the Orange Revolution, the EU was working with Ukraine on its bid to join the World Trade Organization (WTO), and Ukraine has agreed to ensure that new company law, competition rules and environmental and consumer protection are similar to those in the EU. The EU is expected to grant Ukraine market economy status by June.

But at the same time there is considerable concern among many Europeans about expanding the EU to the borders of Russiaand the union is still getting to grips with the last wave of enlargement and the process of introducing a constitution to streamline its operation. In addition, Russia itselflong used to getting its way in Ukraineis resisting attempts to bring Ukraine under the wing of the EU. Despite supporting the fraudulently elected rival to Yushchenko in the November election and being the leader of one of the few countries to accept the validity of the election, President Vladimir Putin has since visited Yushchenko in a bid to shore up the influence of Russia in Ukraine.

For investors, EU entry could present a huge opportunity. The potential for profits to be made from convergence as the countrys economy moves into line with Europe are arguably greater than that of any of the 10 countries that joined the union in 2004not least because the country is so poor at the moment. But as with all potentially great rewards, there is risk attached. While Ukraine, having experienced its Orange Revolution, now looks politically stable, the revolution demonstrates the potential for upset. And the government of Yushchenko will need to make significant organizational and financial advances before any EU talks begin.

Laurence Neville