Japanese Bank Failure?

Might a large Japanese bank fail in 2003? Quite possibly, say analysts, who point out that the government will be forced to step in to prevent a system- wide crisis of confidence. Pain is spread across a banking sector bowed under by bad debt and a stagnant economy, but the woe is most apparent at Mizuho Financial Group, the worlds largest bank, with $1.3 trillion of assets.

The end of March financial year-end is looming as crunch time. By then Mizuho and other banks must book losses on equity holdings. Moodys rates Mizuhos financial strength at just E, the lowest possible. Speculation that the government will have to step in at Mizuho and other leading banks has already periodically roiled Japans stock market. CEO Terunobo Maeda swung into action in December, unveiling a plan to slash costs across the board by around a fifth. Hes also likely to try to raise billions of capital to fill the gap in the banks creaking balance sheet.

Tokyo analysts say there is a chance Maeda may pull a rabbit out of the hat; others say the bank is running out of time. Expect this drama to quicken dramatically early in the year.

Competitive Currency Devaluation

Whats the biggest threat to the global economy this year? War in Iraq? Or a renewed dip in US economic activity? Maybe, but it might also just be a return to the beggar-thy-neighbor policies of the 1930s.While no one expects the infamous Smoot-Hawley Tariff Act to be re-enacted, countries and major trading blocks could be tempted to resort to competitive currency devaluation, a tactic that could have the same effect as higher tariffs by boosting exports and shutting out imports.

Word that President George W. Bush last month selected John Snow, CEO of railroad holding company CSX, to be treasury secretary sent the US dollar into a tailspin. Rightly or wrongly, market participants perceived Snow to be a mercantilist who could abandon the administrations support of a strong-dollar policy.

Analysts point out that not only does Snow come from an industrial background, but he also once headed the Business Roundtable, a lobbying group that last February called the overvalued dollar one of the most serious economic problems confronting the United States today.

This followed on the heels of some rather disturbing comments from Japanese finance minister Masajuro Shiokawa.At a time when the dollar was trading near 124, Shiokawa said that based on calculations of world value, the dollar should be around 150 to 160. The yen hasnt traded at such a weak level since 1990.

Devaluations often lead to trade wars. Cooler heads point out that a nations stock market and economy as a whole perform worst when that countrys currency is under attack.

Return of the Long Bond

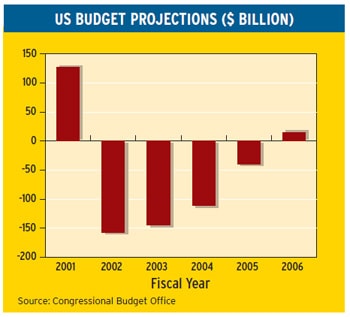

Look for the long bond to make a re-appearance later this year, in light of the new leadership at the US treasury and a federal spending spree that will widen the budget deficit.

With long-term interest rates at 30-year lows, the US government should be locking in current rates, reducing borrowing costs in the long run, credit-market analysts say. A reissued 30-year bond also would make it easier for insurance companies to match long-term investments with liabilities and for corporations to price their own long-term debt, they say.

The 30-year bond served for many years as a benchmark for long-term interest rates because of the good credit of Uncle Sam and the size and liquidity of the treasury market. But in October 2001 treasury undersecretary Peter Fisher came up with the idea of killing the revered long bond to bring down the back end of the yield curve.The government was running big budget surpluses at the time and had less need for the 30-year.

Analysts say Fishers idea worked, at least temporarily, but that the time has come to recognize changed realities and to bring back the old workhorse. Treasury secretary-designate John Snow could get off to a good start by demonstrating his savvy at debt management by bringing back the markets old friend.

Linux Grows Up

The Linux open-source operating system is likely to play a bigger role on the corporate desktop in 2003 on the strength of its attractive low price and recent strong gains in the server market.That could mean big trouble for software superpower Microsoft.

IBM gave Linux a big shot in the arm in early December by introducing its first stand-alone Linux-based server. Big Blue says it has seen strong demand for Linux from customers in government and the oil and automotive industries in particular.

A November 2002 survey conducted by Evans Data found 60% of companies using Linux on some servers, compared with just 43% six months earlier. But theres a lot of room for growth, as only 3% of companies are deploying Linux on more than half of their servers.

A Goldman Sachs survey of 100 IT managers at large US-based multinational companies found that 39% of respondents had implemented Linux in some capacity, including Web servers, desktop PCs, mainframes, data centers, application servers and databases.

Analysts say that Linux has the potential to capture a huge share of the corporate desktop market because of its low cost of deploying and other benefits. Linux backers say that it provides users with better security, flexibility and opportunity for innovation than the Windows operating system because the underlying code for programs is open to sharing, modification, evaluation and scrutiny. Microsofts proprietary software cannot be copied or modified freely, and its source code is available only on a limited basis to approved partners and educational institutions.

Microsoft, of course, is vehemently fighting to hold back the Linux tide. The company recently commissioned an IDC study that found Microsoft-based servers are cheaper to run and maintain than those running on Linux.

Wi-Fi Revolution

In a bleak tech landscape, theres at least one technology that has the capacity to recreate some of the excitement of the early Internet.Wi-Fior Wireless Fidelitynetworks are booming, and as telcos and tech companies realize just how big this technology can become,theyll spend much of 2003 maneuvering for position.

In late 2002, AT&T;, IBM and Intel announced they were backing Cometa Network, a New York start-up that aimed to string together Wi-Fi hotspots into a nationwide broadband wireless network that it could sell on to retailers such as phone companies and Internet service providers.

Wi-Fi is a classic bedroom-to-boardroom play.At the end of the 1990s techies across America discovered that using a new wireless standard called 802.11b allowed them to transmit their existing broadband access across radio waves. Rigging up an antenna to a laptop allowed fellow users to cruise the Internet for free when in range of a socalled hotspot.

Realizing the threat this poses to conventional, paidfor services such as cell phones, companies are moving to capture this business. Bell Canada, for example, is trialing free access at seven payphones located in highdensity areas such as Torontos Union Station. But this technology still reads like a replay of the cattle barons versus homesteaders battles of the late 19th century. While broadband providers write strict no re-transmission clauses into their contracts with customers, Wi-Fi warriors are pushing an alternative, free-to-all model, chalking up markers for hotspots on busy city-center sidewalks, for example.

There are other concernssecurity and spectrum interference rank highbut theres little doubt this technology has transforming power.

Euro Decision Time for UK

Thats because a decision on the euro has to be taken in the light of a five-item checklist, with questions ranging from How will entry affect the position of the City of London? to Does monetary union have sufficient flexibility to deal with a crisis?

The last question has acquired particular poignancy as some of the European politicians most closely associated with forging monetary union have admitted its weaknesses in the past year.

Branded stupid by European Commission president Romano Prodi, Europes stability and growth pact is now certain to be amended.To stop complete unraveling of the pact, the commission has had to introduce more flexibility toward countries with sound finances wanting to borrow to help them endure economic slowdowns. Thats a mantra that chancellor Brown has been pounding out in recent years. (Just as well: In November he had to announce that UK government borrowing was set to balloon by an extra 20 billion over the next two years because of falling tax receipts.)

The European Central Bank will probably come closer to adopting a yet more cyclical approach to economic management. European laws might change, or a moratorium may be put on chasing up the hefty fines to which breaches should lead. Portugal, already an offender, is unlikely to be punished. It may be joined in the sin bin by Germany, France and Italy.

Relaxing constraints on budgetary policy wont turn Gordon Brown into a europhile, but it will disarm him of a key argument against joining the single currency.

A Single Capital Market?

New year, same old disappointments. Europes legislators have until the end of 2003 to put in place laws to ensure that by 2005 the continent has a single capital market to rival that enjoyed in the United States. It was always going to be tight, but now that timetable looks woefully optimistic after months of bickering between different parties.

Thats important: The European Union Commission estimates that the network of conflicting national requirements can add up to half a percentage point to the cost of capital for a European company. Introducing harmonizations such as a single passport for selling an equity offering in all 15 EU countries could add over 1% to the continents GDP, according to the same calculations.

The process has so far been anything but smooth, despite a streamlined drafting procedure set up on the recommendation of the former Belgian central bank head Baron Alexandre Lamfalussy. In March last year the European parliament voted to exempt small companies three quarters of the total from new listing requirements. A common code on takeovers was also thrown out.

London, Europes most important financial center, is emerging as a focus for opposition to harmonization. Howard Davies, outgoing head of UK market regulator Financial Services Authority, argues that the common rules on listings, for example, will undermine existing, high standards for the London market.

Chris Huhne, a British MEP closely associated with reform of financial regulations, says the new rules will ensure minimum standards, not maximums.

Russian Pension Reform

Dramatic pension reform in Russia designed to provide for millions of impoverished workers will trigger a flood of billions of dollars into the countrys debt and equity markets and stimulate competition in the financial industry.

The new legislation that comes into effect this month will free a portion of pension contributions currently managed by state-run funds to be invested by independent asset managers. Later, it will also oblige employers to provide professional pension plans for their workforce. Employees not satisfied with company plans will be free to shop around for a better deal.With little or no experience in investing money, its expected many companies will choose to farm out the work to industry professionals.

That prospect has asset managers rubbing their hands in anticipation.The potential impact on the markets is huge, says Bernie Sucher of Alfa Asset Management in Moscow. By 2010 Russias GDP is likely to grow from $350 billion to $520 billion, but we estimate that funds under management will rocket from just $3 billion today to $50 billion over the same period, and pension reform will be part of that process.

Despite the reforms, theres little chance of an overnight bonanza. Access to potential clients and distribution will remain a significant hurdle in a country that spans 11 time zones.

And educating people to buy financial products will prove difficult. Most people in Russia are still more used to stashing savings under the mattress than taking them to the bank, and after a series of scandals and crises over the past decade the financial industry is still badly mistrusted.

Russia Restructures

In whats being described as the third wave of asset reshuffling in post-communist Russia, following voucher privatization and rigged auctions in the 1990s, cash-rich companies have been snapping up a wide range of assets at bargain prices following the disastrous financial crisis of 1998.

Now that the Russian economy has stabilized, valuations are rising once again.For those that bought at the bottom of the market, the returns will prove spectacular: Factories picked up for as little as $60,000 are now selling for more than $1 million.

Some industrial holding groups, however, will instead be looking to rationalize their portfolios, which may now include everything from dairy plants to metal mines, and look to strengthen their position in some sectors and sell out others.

We expect to see a pick-up of M&A; activity over 2003, particularly in the oil sector and among the big industrial groups as companies tidy up their loose asset portfolios, says Christopher Weafer, chief strategist at Alfa Bank in Moscow.The impact on the capital markets and banking may still be some way off as a lot of companies will be swapping assets between each other.

The trend is set to accelerate. Many holdings have already planned early IPO exit strategies from their forays into non-core sectors, and greater FDI flows are expected after presidential elections in 2004, when Russia is expected to win investment-grade status.

Chapter 11 Stress

As more US firms troop through the bankruptcy courts in 2003, expect attention to focus ever more strongly on the restructuring process itself. Until now Chapter 11the legal framework by which troubled companies hold off creditors while they reorganize themselveshas been viewed as essential a part of American life as cheap gasoline, an embodiment of the home-grown desire to have a second bite at the cherry.

Critics have struggled to get a hearing. This time around, the relentless thud of legal and advisory bills on companies doorsteps might just combine with shareholder distaste for reckless managers to produce a head of steam for reform.

The figures dont make easy reading.Advisory fees for bankrupt energy trader Enron climbed so highto $280 million by the end of October,according to one report that the New York bankruptcy court appointed a retired judge to review them.The Enron case may be a particularly trappy one, but with companies such as United Airlines going under owing more than $21 billion, advisers are sitting on a gold mine.

The problem is, its not at all clear that creditors and shareholders are getting a good deal for what is effectively their money. The airline industry is a serial recidivist: Continental Airlines, for example, has filed for bankruptcy twice, making it part of a growing band of so-called Chapter 22 companies. Others have failed to emerge from bankruptcy at all. Its the spotty record of Chapter 11plus the beanfeast it provides for advisersthat has fueled growing discontent.

Alternatives are thin on the ground, but expect backers of schemes such as controlled auctions to gain a bigger hearing.

Rating Focus

Thats music to the ears of issuers and investors alike. Sellers of bonds often complain that agencies dont truly gauge their financial strength, while fixed-income investors have been roiled in recent months as companies such as Enron crashed from investment-grade ratings through junk and then into default.

Both issuers and investors have increasingly argued that greater competition may force agencies to up their game, increasing transparency and acting in a more timely fashion. Between them, Moodys and S&P; issue almost four in five debt ratings globally, a franchise that has proved ever more lucrative as bond market volumes have swelled. Experience and expertise gives the established agencies heft,of courseS&P; traces its history back to 1860 and now boasts more than 1,250 analysts in 30 countriesbut its the SEC that effectively holds the key to the industry. Since 1975 it has dubbed S&P;, Moodys and Fitch Ratings as nationally recognized statistical ratings organizations.

But Fitchs difficulties in breaking into the big league underline just how strong a stranglehold on the industry Moodys and S&P; have. An attempt to create a European alternativeEuroratingsfailed in the late 1980s.

Whatever the SEC rules, its likely to be the big boys that the denizens of world bond markets will be dealing with for years to come.

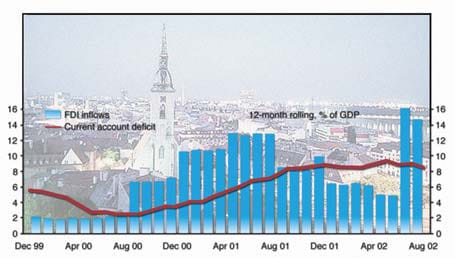

Finding Slovakia

Looking for a central European country set to benefit from last months historic agreement on European Union enlargement? You could do worse than trying Slovakia, a small, land-locked country historically overshadowed by its neighbors. British Prime Minister Lloyd George famously couldnt quite locate Slovakia in the peace conference after the First World War, and its been a backwater more or less ever since.

Foreign direct investment has been pouring into the Czech Republic at more than twice the rate of its former co-national in recent years as Western companies balked at the air of old-style East bloc that still hung over Slovakia. But with a new reform-minded government voted in in September 2002,that might be about to change.Estimates put last years economic growth at around 4% and a little less in 2003.EU membership is now slated for 2004, and the euro may replace the Slovak crown by the end of the decade.

To be sure, Slovakias transformation hasnt gone entirely unnoticed by foreign companies:Volkswagen, US Steel and Deutsche Telekom have all set up shop there,and FDI in 2002 hit a high of 12% of GDP. Much of that investment has been in the form of privatization. Thats likely to remain the main route into the country in 2003, with Mikulas Dzurindas government hinting that it might sell non-controlling stakes in the telephone,gas and railway monopolies.

Modernizing those industries has sucked in capital imports and helped worsen the current account deficitat 10.3% of GDP a worrying gap to set alongside the budget deficit. A climbing currency might also choke exports, but with reform in the air Bratislava is set to regain its place on the map in coming years.

Could Germany Lose Triple-A Rating?

Could Germany lose its triple-A rating this year? It may be unlikely, but the fact that the previously unthinkable could even be worthy of consideration is evidence of just how serious that countrys problems are being taken. In mid- December the rating agencies Standard & Poors and Moodys Investors Service reaffirmed their stable outlook on the countrys topflight ratings but sounded some chilling warning notes for the future.

Hanging over the whole debate is the specter of Japananother model economy that failed to adapt and is now in the trough of a decadelong deflation. Japan, of course, has long since lost its coveted triple-A rating. But if Germany and Japan share some problems, theres a crucial difference: Japans debt stands at 157% of GDP compared to just 59% for Germany.

Budget woes may have forced Chancellor Schroders government to increase borrowing while tax cuts have been unveiled to kick-start the stagnant economy, but Germanys finances are on a much sounder long-term footing. Moodys analyst Alexander Kockerbeck points out that key debt ratios are no higher in 2002 than in 1996. Moreover,these measures are at levels equal to, or below, those of some other Aaa-rated governments, such as the United States, he says.

Bundesbank president Ernst Weltke says that Germany will remain the eurozone benchmark. Still, the credit default markets were among the most effective signalers of risk last year.

Bank credit analysts are typically more gloomy than the raters, and the premium demanded on swaps for German risk have been creeping up. Its now more expensive to buy insurance on Europes largest economy than it is for France.Watch this one carefully.

Hedge Fund Plays

Hedge funds arent set to disappear any time soon; theyre just learning new tricks. Among the big plays for 2003,say industry analysts,will be trading a companys debt against its stock in order to make a turn.

Arbitraging different parts of a companys capital structure is not entirely new, of course.During 2002 a number of vulture funds tried to short the debt of distressed companies such as Marconi while going long on their bonds, for example. Rather, the convergence between the worlds of debt and equity has been gathering steam for some years and was thrown into sharp highlight by the unprecedented turmoil of last year.

As companies hit the buffers, stock prices slumped and credit spreads widened, rudely awakening investors to the interconnectedness of once-separate asset classes. Whats different now is that bond and equity buyers have models that attempt to map those links and throw off signals when one side of the equation goes out of kilter. And investors now have the instruments to trade on those go signs: Hedge funds can sell stock short, while credit default swaps allow fixed-income investors to flip to the other side of a bond trade.

A number of banks have set up desks that combine debt and equity trading, aiming to serve the growing number of hedge funds seeking to find replacements for more playedout arbitrage strategies such as convertibles.

Not everyone is convinced that debt/equity plays are the future. Gary Jenkins, head of European credit research at Barclays Capital in London, thinks the two markets will de-link in 2003. But corporate treasurers, never fans of hedge funds, will likely have to keep a weather eye on pesky arbitrageurs.

Vaccines Flourish

The pharmaceutical industry lived on its nerves in 2002, with shares slumping as old product lines went off-patent while newer businesses struggled to fill the gap. But this year it might just be an unlikely bit of the business that provides some cheer. Humble vaccines may outshine glitzier business lines, say analysts. Some of that newfound attention is a reaction to fears over bioterrorism, of course: Congress is ordering $3.6 billion of drugs next year against anthrax attacks and the like.

But translating public spending into private profit isnt always a straightforward task, as elements of the US defense industry can well testify. Instead, its changes in the industry itself that are transforming prospects. In November, US drug group Merck caused a flurry of excitement on the news that a vaccine it had in development was effective in combating most forms of cervical cancer.

The growing body of evidence that infections by viruses and bacteria can lead to more complex conditions such as cancers is opening new vistas for vaccines. Runof- the-mill vaccines for childhood diseases such as measles had proved so uneconomic that the industry shrank dramatically. News of Mercks success coincided with a report from Unicef and the World Health Organization that there was a shortfall of up to one quarter in the amounts required to vaccinate children against the diseases tetanus and diphtheria.

New high-end vaccines wont help there, but shareholders are betting that a swelling product pipeline might revive company fortunes.

To translate that sort of promise into a revenue-generating reality,big pharmaceutical companies need to get right the relationship with the smaller biotech operations that come up with most of the new products. Cooperation is the buzz word, but sector leaders such as PowderJect Pharmaceuticals are likely to continue to attract the attention of would-be buyers.

Selling Emissions

Last months greenhouse gas (GHG) emissions sale by the Slovak government to an undisclosed Japanese trading house is the first deal in whats set to be an increasingly important market in 2003. The central European state, acting on the basis of GHG caps that will come in with the likely enforcement of the Kyoto Protocol this spring, sold 200,000 metric tons of carbon dioxide emissions. That added a governmental presence to an emissions trading market already gathering momentum between large energy companies.

While governments have been negotiating whether and how they will reduce GHG emissions, groups including Cantor Fitzgerald (through its subsidiaries CO2e and Cantor Fitzgerald Environmental Brokerage Services) and the World Bank (through its Prototype Carbon Fund) have already developed ways of applying commodity-style trading concepts to the right to pollute. Spot transactions, forward and various options mechanisms are just some of the ways in which large companies can shift emission credits.

The amount of GHG that the Slovak government sold is said to be worth some $1 million in pre-Kyoto trading. How much will it be worth later? Thats anybodys guess, but its clear that a market more talked about than traded in until now is at last gathering a head of steam.

Energy Trading

Whisper it quietly in California, but energy trading is set to stage a comeback in 2003. Justly reviled as an industry fueled by bombast and sharp practice, energy trading suffered a perfect storm in 2002, as fraud and overweening ambition brought the market to the verge of collapse.

Dont expect to see traders with $2,000 lunch habits back any time soon, however. Instead, energy trading is attracting new players to a different marketone where there are real players on either side of a trade. Deregulation is here to stay, and in that market energy companies need mechanisms to hedge and manage risk. The global power-and-gas industry is more exposed than ever before to economic uncertainty and other problems, says Fred Cohen at PricewaterhouseCoopers. Its that need that has already encouraged banks and other financial companies such as UBS and AIG to step in where others exited.

Energy trading may be duller in the future, but at least the lights will still be on.

Insurance Mergers

Expect a wave of consolidation in the global insurance industry as companies battered by disasters and stumbling stock holdings face the need to reshape their businesses before premiums head south again.

Those woes have already prompted companies across the globe to slash jobs and shutter business lines. Germanys Gerling has pulled out of reinsurance while Zurich Financial Services said its Center unit would no longer write credit enhancement.

That probably wont be enough for many, though. Industry watchers expect a flurry of transactions in the industry. Companies have already attempted to gobble othersManulife Financial made a till-now-rebuffed $4.1 billion hostile bid for compatriot Canada Life Financial in mid-Decemberbut thats likely to be just the start. Insurers may seek to strengthen balance sheets by making calls on investors during 2003, but that wont be easy, as companies such as reinsurer SCOR of France found out. But even if the For Sale signs are put out, the buyers may still not appear. The strongest companies may choose to grow their businesses organically, while focusing on reshaping a robust business model.

Still, for deal-starved investment bankers, any pick-up in mergers and acquisitions activity among their insurance cousins will be sweet news indeed.

Asian Hedge Funds

Hedge funds were once dirty words in Asia, but expect more of the regions investors to take their first steps in the market in 2003, as traditional mutual funds languish. In December,Hong Kong regulator the Securities and Futures Commission allowed three hedge funds to market themselves directly to retail investors in the territory. The funds will be run by JP Morgan and HSBC and are the first of a number set to be given the green light by the regulator this year. Hedge funds were seized upon as the chosen tools of international speculators that many Asian politicians blamed for the regions financial crisis. Mindful of that, and their sometimes high-risk profiles, the Commission is making a determined guide to educate the Hong Kong public. Among the tools: a hedge fund ABC on the regulators Web site.The regulator is also setting great store by reporting requirements: Hedge funds will have to send investors annual, semi-annual and quarterly reports.Our disclosure requirements are the first of its kind in the world, says Alexa Lam, an executive director at the Commission.

And hedge funds have already received a stamp of approval in the territoryeven if an unofficial one. In March last year, the Hong Kong Jockey Club confirmed it was to place $100 million with two US-based funds after months of rumor. The Jockey Club, which runs horse racing in the terrority, is famously conservative in its investments.

The move is part of Hong Kongs attempt to hold onto its crown as Asias premier financial center. Singapore already allows hedge funds, and some $20 billion is already under management in Asia.

The region is already beginning to sprout the apparatus of hedge funds investmentincluding competing indexes with which would-be investors can track their funds performance.

Public Sector Finances

After Enron went under at the end of the preceding year, the spotlight during 2002 remained firmly on corporate Americaand there was no shortage of commentators queuing up to say,I told you so. That queue was longest in Europe,where many commentators viewed the relentless unveiling of US corporate misdoings as overdue comeuppance for a decade of private sector triumphalism.

They had a point, but in 2003 the boot may be on the other foot, as the spotlight turns to the public sector. Economists say that government accounting practices are particularly ripe for reappraisal.

Indeed, there are signs that crumbling public finances and swelling deficits are already renewing the focus on how public bodies count their numbers. The incoming French government found plenty of skeletons crammed into the public sector cupboard, while Novembers SPD election triumph soon turned sour as German finance minister Hans Eichel had to hike borrowing by 13.5 billion this year to plug gaping holes in the federal accounts.

Eurostat, the official European Union statistics agency, is rapidly emerging as chief public sector accounting cop on the Old Continent.It ruled that subsidies to loss-making Greek companies had to come back on the public sector balance sheet, turning a projected 2002 surplus of 0.4% of GDP into a 1.1% deficit.

Savvy investment bankers may no longer be able to shuffle debts off the governments balance sheet: Eurostat has ruled that one-off securitizations of public sector cashflows, such as Italian pension receipts or Greek lottery money, can no longer be used to pay down debt.

Thats unlikely to stop public sector financial engineering altogether, but its clear theres no monopoly on sharp practice with numbers.

Mark Johnson, Benjamin Beasley-Murray, James Schofield, Gordon Platt and Adam Rombel