Despite political turmoil at home, many American Depository Receipts (ADRs) of Brazilian companies are doing well, thanks to strong liquidity in the United States. But volatility is also hurting many stocks.

The ADR issue actually had more demand, with total interest worth $1.9 billion, thanks to an ambitious road-show that included 110 meetings in the United States, Europe, Argentina and Brazil. Treiger believes part of the reason for the issues success was that the company rented a private jet to bring the executives to meet with investors. We were everywhere whenever possible, he says.

Braskems ADR (BAK) was among the five best-performing ADRs on the NYSE last year and the overall best performer in 2003. The Braskem ADR was officially listed in September 2003 after it replaced the ADR being held by Copene. Braskem is the result of the merger of various petrochemical companies, including Copene. Thanks to the capital raised last year, Braskem was able to reduce its debt, while raising its international profile. You can see how important the ADRs are to [that] success, Treiger says.

Alexandre Q. Fernandes is another keen supporter of ADRs. As disclosure manager of investor relations at Petrobras, Brazils largest company and the second-most traded Brazilian ADR, hes seen the companys depositary receipts (DRs), whose symbols are PBR (common) and PBRA (preferred), skyrocket from $25.25 and $12.74, respectively, to $52.80 and $46.51 on June 28. PBR is among the 10 most-NYSE-negotiated ADRs, and PBRA among the 20 most negotiated, he points out.

While volatility has affected some shares, overall Brazilian ADRs have gained in value and volume the past year. The Bank of New Yorks Brazil ADR Index went from $84.88 to $155.49 in the 52-week period ended on June 30. In the first six months of this year it gained 13%. The increase is due to a combination of factors, including significant revenue and earnings growth by the companies, increased confidence in Brazils macroeconomic policies and economic outlook and growing liquidity among US investors.

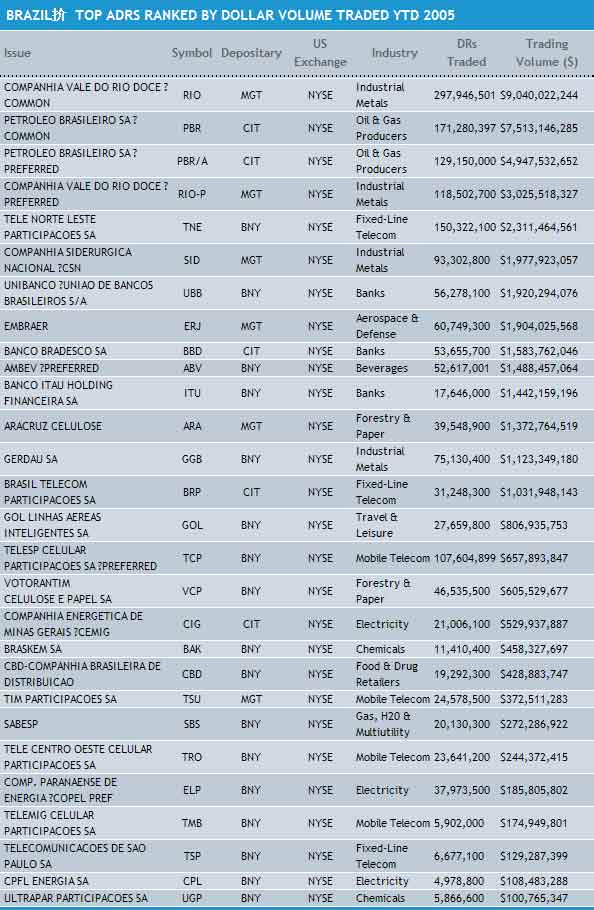

The index includes 34 Brazilian companies, all of which are listed on the NYSE. All but five posted gains in the 52-week period ended June 30. The strongest gain was registered by Perdigao (PGA), which saw a 135% increase in its ADR price. Banco Bradesco (BBD) followed at 126%. Other big winners include Cemig (CIG), Ultrapar (UGP), Banco Ita Holding (ITU), and the two companies with the most traded ADRsCompanhia Vale do Rio Doce (RIO and RIO-P) and Petrobras.

The worst decline was posted by wireless operator Telesp Celular Participaes, which saw its preferred ADR (TCP) decline by 44%, followed by long-distance telephone operator Embratel (EMT), with a 23% decline, according to data from the Bank of New York.

Geraldo Soares, investor relations manager at Banco Ita, agrees. The ADR initiative aims to give Banco Ita Holding Financeira greater visibility and to encourage share trading in international capital markets, since investors the world over can now trade our shares in dollars, he says. This increases the liquidity and the upside potential of Banco Ita Holding Financeiras shares.

But not everyone sees the ADRs as a panacea. For Luiz Gonzaga Murat, chief financial officer of Brazilian food producer Sadia, having an ADR is a double-edged sword. Our program was launched in order to access the American equity market and open the possibility of Sadia participating in the most developed worldwide market, he says. While that is clearly an advantage, information disclosed in relation to the ADR can reach the companys competitors. Sadia also has to bear extra costs simply to have an ADR, although it has not participated in any equity calls in the past 10 years, Murat says.

Nevertheless, the Sadia executive is pleased with the result. Sadias Level II ADR (SDA) has traded a daily average of $679,672 in the first quarter of this year. Thats more than twice the average for all of 2004. However, its value declined from $66.05 at the start of this year to $19.54 in early trading on July 1.

The ADRs provide access to significantly larger markets than local stock exchanges such as the So Paulo Stock Exchange (Bovespa), Brazilian executives and independent analysts point out. The stock exchanges in Brazil have small volumes compared to the big financial centers, says Pedro Roberto Galdi, a So Paulo-based analyst with ABN AMRO. That was a major driver behind the decision by Companhia Vale do Rio Doce (CVRD) to launch an ADR. The company wanted to reach a large pool of investors and increase the companys shareholder base, says Fatima Cristina, CVRDs international spokesperson.

Investors are also sometimes wary of putting their money into the local exchanges because they are concerned about regulation or other issues like currency differences, while some funds are not permitted to trade in stocks not listed on US exchanges. Bovespa, for example, is weakened by questions around minority rights, although there are reform proposals to make the exchange more efficient, says Christopher Garman, a So Paulo-based analyst with the Eurasia Group. Unfortunately, [local] capital markets are not sufficiently developed, he says.

Soares from Banco Ita agrees. Entering in the ADRs market, Banco Ita had to fulfill the rules of US law that is different from Brazilian, and then we made it an opportunity to improve our controls in advance of any Brazilian legal imposition, he says. Last year the bank created an audit committee, formed by three councilors (two independents and one external). The companys corporate governance standards are now in line with Sarbanes-Oxley requirements. The disclosure and the expansion of controls shouldnt be treated as an obligation but always like an opportunity to improve all the inside process, Soares says.

Rene Boettcher, vice president at the Bank of New York and head of Latin America marketing for ADRs, points out that Brazilian companiesas well as public regulationshave made significant progress the past few years. Overall, in the corporate governance landscape, Brazil has made huge strides to become more transparent. Corporate governance has been a huge topic the last two years, he says.

Brazil is the top ADR market in Latin America, with 96 ADR programs, compared with 82 for Mexico. Worldwide, it ranked third last year measured by trading value and fourth in trading volume, according to the Bank of New York. Eight new Brazilian ADR transactions raised $1.1 billion last yearalmost three times as much as the capital raised in 2003. Among the most successful was the ADR launch of airline Gol Linhas Areas Inteligentes (GOL).

|

Breadth Trumps Volume |

|

While some other countries may have larger ADR volume than Brazil, the South American country is unique in that it offers such a broad spectrum of companies. If you look at the breadth of Brazil, then its even more important. Finland has one or two [ADRs] or Taiwan has a huge volume out of three or four names, says Boettcher. That is why I think Brazil is a huge force and will continue to be.

Brazilian companies are using ADRs to receive exposure and visibility in the US market, broaden shareholder base, get more sell-side coverage, increase interest in the country through the big companies, and use ADRs as M&A; currency, says Candice Teruszkin, regional head of Latin America for ADRs at JPMorgan. Because of their flexibility and liquidity, they form a useful addition to a companys financial toolbox. Apart from ADRs, Brazilian companies typically use the Bovespa or even European stock exchanges to raise funds. Telesp, for example, lists two shares on Bovespa (ordinary and preferred) and has a program of bonds (through national and international markets) and some loans from local development banks, Allen says. Were glad to have many sources, including the NYSE, Bovespa or other markets, he says. Allen believes the key to using ADRs successfully as part of a companys capital-raising toolbox is to be adaptable. Its not static; its something that changes, he says of the capital markets. Its difficult to say, Yes, I prefer Bovespa or Yes, I prefer ADRs. Its simply a question of when you need it and how conditions are. Brazilian companies Braskem, Sadia and pulp-and-paper-producer Suzano Bahia Sul Papel e Celulose are also listed on Latibex, a market in Madrid on which individual Latin American companies may list their shares. Braskem was first out, with a listing on October 8, 2003, while Sadia was the latest addition from Brazil, with a listing on November 15 of last year. The demand for existing Brazilian ADRs is high and has helped offset the relatively low number of new issues the past few years. Last year there were only six new issues, and the year before that, only one. That compares with an average of 10 during each of the previous four years. So far this year, two companies have issues two ADRs eachtransportation company ALL- Amrica Latina Logistica and online retailer Submarino in March and April. The current state of the Brazilian market is positive, Teruszkin says. Currently, there is ample liquidity in the US market and local market as well. There is a favorable appetite for Brazil. Of todays 10 most popular ADRs, six were launched in 2000 or later. In terms of sectors, electric utility accounts for most of the ADRs (with 21), followed by telecommunications (13) and metal production and distribution (8). Despite the recent volatility, executives like Sadias Muzat and CVRDs Cristina are optimistic about their ADRs. CVRD sees an increasing interest in the companys shares not only from institutional investors but also by other countries individuals, says Cristina. So the outlook for ADRs remains very positive. ABN AMROs Galdi believes more Brazilian companies will issue ADRs in the future. The companies have a need, and this is a way to follow, he says. There is currently a cycle of new IPOs in Brazil with the expectation that they will also be listed internationally. Some analysts, however, are less optimistic. I see a large trend of local IPOs and less issuance of ADRs Level II or III, due to Sarbanes-Oxley and other requirements, warns Teruszkin. There could likely be a better chance of future Level IIIs due to the need to raise cash and a better comfort level on the regulatory front. But independent of the continued growth or not, Brazil has reason to be proud of its ADR record, Boettcher points out. If you look at the past 13 years1992 was the first year when a Brazilian company made its Level III global public offeringfrom that moment onwards it has been only growth, every year, he says. In 13 years, youve gone from one ADR program to now almost 100. That is huge growth. |

Political Scandal Shakes ADR Market

|

|

|

In early June Brazilian legislator Roberto Jefferson from the Labor Party claimed that President Luiz Incio Lula da Silvas Workers Party (PT) paid lawmakers money to support the coalition government. Lula has denied wrongdoing, but four of his top aides resigned by mid July: chief of staff Jos Dirceu, PT secretary general Silvio Pereira, party head Jos Genoino and PT treasurer Delbio Soares.

Brazilian ADRs had, in fact, rallied on the news of Dirceus resignation and the fact that Jefferson had been unable to present concrete evidence for his accusations.

Political turmoil at home isnt the only factor that can weaken ADRs, though. Its a bigger financial market with a lot of demand, but riskier at times with very high interest rates, big surplus due to exports and currency benefits, says Candice Teruszkin, JPMorgans ADR regional head of Latin America. Globally, its a very attractive markethigh-risk though, which can be very volatile at times with big political and economic influences on the course of the market. Not all Brazilian companies view volatility as a disadvantage of the ADR program, though. Volatility [is] part of the game, says Charles Allen, investor relations director at Telesp. We would have that anyway. All stock exchanges are somehow connected, so I wouldnt say additional volatility is bad or good.

Joachim Bamrud