After the summers rash of widespread electricity outages, companies are looking to manage their energy risk. Derivatives may provide an answer.

The danger of such outages is that their effect is instant, explains David Bucknall, CEO of energy risk management systems provider KWI. Other commodities, such as oil, dont have the immediacy of the delivery issue; its fairly well stocked as a supply chain, he adds.

In the US in particular, the poor state of the electricity transmission infrastructure means such outages could easily occur again, with serious effects for businesses. As a recent report by Standard & Poors notes: Widespread blackouts are costly. They disrupt commerce. They shut down communications and water supplies. And they invite litigation in the aftermath. Estimates of the cost of the US blackout range from $6 billion to $10 billion.

While broad-brush statements make good headlines, drilling down into the numbers is not easy. Mark Tawney, managing director at Swiss Re Financial products, says, It is very difficult to quantify the cost for an individual corporate of events such as the recent power outages.

Indeed, financial institutions have yet to develop a financial hedging instrument for these rare events. As the cost that is represented by energy is so low for corporates in non-energy-intensive industries such as banking and publishing, it is not in their interests to allocate capital to what is considered to be a low-frequency occurrence.

However, says Marc Watton, senior utilities analyst at BNP Paribas, For more energy-intensive industries, such as pulp and paper, aluminum, chemicals and so on, it becomes a question of having an operational contingency in the form of their own combined heat and power plants or auto-generation plants. Chemical giant ICI, for example, has a modest plant that produces enough energy to meet its own requirements. Any excess is sold into the national grid.

Generating power is not a cheap option, though. A typical combined cycle gas turbine plant would probably cost 200 million to 400 million ($335 to $637 million), while you could get a smaller plant, like a combined heat and power plant, off the ground for 100 million to 150 million. Its an awful lot of money to spend just for the occasional blackout if energy isnt vital to your business, says Watton. For those corporates where energy isnt vital in terms of risk, its an insurable risk rather than a hedgeable risk.

Businesses Confront Energy Risks

While power outages may not ultimately be hedgeable, the fallout from the recent blackouts has brought other energy-related risks to the forefront of firms minds. Shannon Burchett, president of energy consultancy Risk Limited, headquartered in Dallas, says, The power outage is the most severe incident out of many in the last few years that has highlighted to corporate users their exposure to a range of risks

|

|

|

related to energy supply. According to Burchett, it is not just event risk, such as the blackout, that companies are concerned about. They are also anxious about, say, credit risk with regard to their suppliers, as well as price risk and regulatory risks. Counterparty risk assessment is critically important in corporates positions as energy consumers because they have significant credit and performance risks to consider, over and above the grid melting down.

In addition, price risk in energy remains high and, particularly for corporations with heavy energy consumption, is a considerable risk component going forward. Market watchers warn there wont be price stability for a long time to come. Price levels for corporate users will continue to fluctuate widely in deregulated markets; this is the consequence of moving away from a regulated, fixed-price, government-controlled energy market, comments Burchett. The same could be said for natural gas prices; many corporates had quite a shock in the first part of this year when natural gas prices doubled, which made a significant difference to their bottom lines, he adds.

As a result, companies need to consider the way in which they use energy and hedge its consumption. While there is always the option of simply buying energy at a fixed price and using as much of it whenever they like, thereby mirroring the average consumer, Bucknall says that corporates should have a planned profile of their energy purchases from the network.

A companys energy purchasing habits clearly should depend on how significant energy is as part of the cost of running its business. An energy-intensive business, such as aluminum smelting, would be foolish to take energy at a fixed price b ecause there is a huge amount of risk placed on their supplier to cope with the demand. Even so, the company has a number of variables to consider when planning its profile: how reactive it wants its energy supply to be, what happens if it wants to use more in a certain situation, what happens if its plant breaks down and stops using the energy it is contracted to use. It is therefore necessary for corporates to have contingency plans in place from a trading perspective to be able to react to the change in requirements they have as a consumer of the energy.

Derivatives Provide a Solution

|

|

|

One of the ways to hedge energy price risk is to buy protection by entering into derivatives contracts with gas or electricity as their underlying asset, in the same way as would be done for, say, interest rate risk. There is a range of such futures and options available on numerous exchanges around the world, such as the New York Mercantile Exchange (Nymex) or IntercontinentalExchange (ICE). However, for most corporates an over-the-counter (OTC) transaction, such as an electricity or gas swap or option, could be more suitable as they can be tailor-made to a firms exposure, whereas exchange-traded derivatives cannot.

The OTC energy market had suffered a drop in volume following the demise of Enron and the exit from the market of a number of key players, but this now appears to be changing. Burchett believes this gradual return of some liquidity to the energy financial hedging market is a result of counterparties entering the market, such as banks and insurers, that are perceived to be more creditworthy than some of their predecessors.

The situation is improving slowly, although the possibilities for longer-term hedging are still limited. It depends very much on what the commodity is, says Burchett. In the US, for example, electricity is still relatively illiquid because of current regulatory uncertainty about the transmission regime. There wont be a full return to liquidity until there is additional political and regulatory certainty. But at least we are at a stage where the economy is gradually improving and a lot of the shake-out in the energy sector has now occurred.

|

risk management in practice |

|

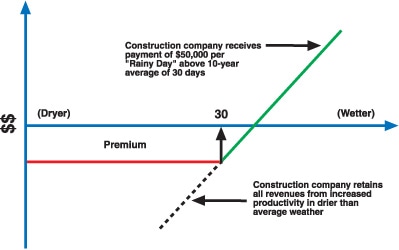

The diagram below illustrates the payout structure of an option designed for a construction company that estimates a loss of $50,000 per day each time daily precipitation reaches a tenth of an inch or above, beyond the cumulative 10-year average number of such days during the period from November 1 to April 30.

The financial protection provided by a weather derivative suppresses profit fluctuations by guaranteeing a minimum level of income. By removing the weather exposure, the benefits of reduced earnings volatility can be passed on to clients and the corporate reputation enhanced as financial compensatory payments could be offered for failing to meet project deadlines as a result of poor weather.

|

Changing With the Weather

|

|

|

More electricity is used when it is hot because of the increased use of air conditioners, for example, which has a knock-on effect on price. However, there are more wide-ranging weather-related effects on businesses than just energy price. Awareness of this, and the consequent utilization of the weather derivatives market, is increasing.

Part of the reason for this is that the financial community is looking for stability, predictability and quality of earnings. Weather risk has a significant impact on this, on both the equity and debt side. Equity analysts and rating agencies are increasingly touting the benefit of mitigating this risk but leaving it up to the corporate to decide on the best route to achieve it. Analysts do ask what corporates are doing about the weather, and if they cant answer clearly, they will face even more questions. This isnt new, but its increasing, says Windle. Corporates perhaps havent been held accountable for the impact of the weather on their business in the past, and they are now able to mitigate the risk. Although we cant determine the weather, we can manage its impact on a corporates bottom line.

|

|

|

The types of weather protection required vary across industry sectors, but one thing is clear with respect to the weather: It has a significant impact on the demand for products. There are few industries that are not affected, but those that are most weather-dependent include entertainment, agriculture, shipping, energy, food and transportation. According to Windle, Swiss Res approach is to view weather as a commodity. We can structure mitigation programs like any other liquid commodity, he explains. As a result, our products can be very complex or very simple, depending on what is most appropriate for a particular corporate. (See box.)

Like the energy markets, the nature of weather market participants has changed since the demise of Enron. For a short time the number of participantsand the volume of activitydecreased. As the market has recovered, however, its make-up has changed. The participants that have replaced these partiesthe investment banks, insurance companies and hedge fundsare more sophisticated and have better credit quality, so the market is much healthier now, Windle says.

In addition, there is an increasingly viable exchange-traded weather derivatives market listed on the Chicago Mercantile Exchange (CME). Swiss Res Tawney concludes: There are 13 US cities that trade on CME in terms of weather, and very shortly some European cities will be added. The exchanges volumes are growing exponentially, helped by greater awareness of credit issues and the benefits in that respect that a cleared exchange product can provide.

Investors will be hoping that this sort of awareness can only lead to better risk management all around.

Mark Pelham