Commercial real estate is being reshaped by the health crisis, offering both risk and opportunity.

Covid-driven lockdowns have wreaked economic havoc everywhere, and commercial real estate is no exception, with prices registering dramatic swings amid few actual transactions. Various efforts around the world to get back to business have led to resurging infections and the reimposition of social restrictions, calling into question any return to “normal.” Months into the pandemic, it remains unclear how all the mostly empty spaces where economic life used to bustle will be used—let alone how they will be priced.

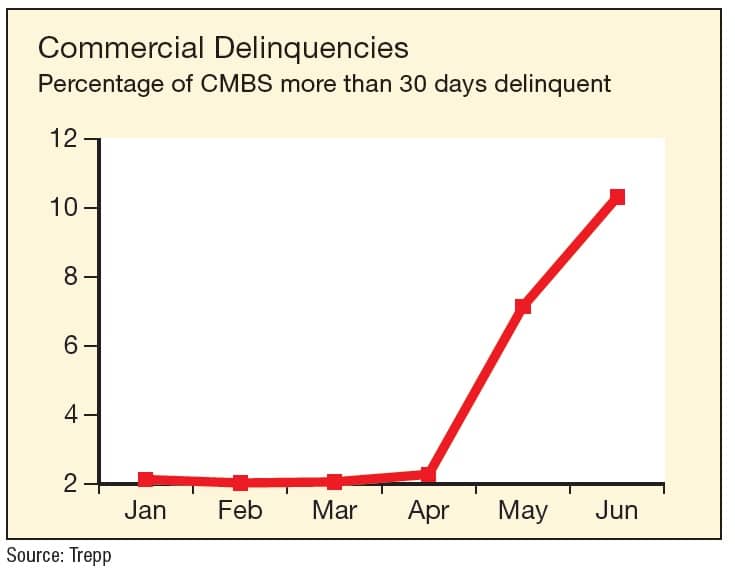

At present, real estate looks pretty bleak. In the market for commercial mortgage-backed securities (CMBS), one benchmark for the health of the sector, “Delinquency and watchlist numbers are horrible, and the fundamentals are awful as well,” says Gunter Seeger, senior portfolio manager at PineBridge. “Industrials, multifamily, offices, hotels and malls—all are doing badly.”

An increase in CMBS delinquencies in May was anticipated, but the size of the jump was still surprising—the largest increase in the Trepp securitized mortgage database since the metric was started in 2009. Then it shot up again in June. It is difficult to say what will happen next and how businesses can bring shoppers back to malls and travelers back to hotels.

Still, history gives cause for optimism. After the 9/11 attacks on the Twin Towers in Manhattan, many New Yorkers said they would never work in a skyscraper again, notes Jonathan Woloshin, real estate and lodging analyst, Americas, at UBS Financial Services. People forget. Ultimately, real estate doesn’t go anywhere, and people have to live and work somewhere. Many investors sense opportunity on the horizon, and real estate hedge funds have been piling up “dry powder” reserves to be able to snap up bargains.

Overall, there is a looming sense that this pandemic will bring substantive change to the ways we live and work, with specific impacts on commercial real estate. “The health crisis has made us look at commercial real estate in a totally different way,” says Nicholas Brooke, chairman of Hong Kong–based real estate consultancy Professional Property Services Group, and also chairman of the Asia Pacific region of the Urban Land Institute (ULI). “We are thinking again about how we use and occupy spaces for working, living, learning and enjoying ourselves.”

Varying Fates

The fate of commercial real estate after the pandemic isn’t one story, but many stories, varying by property type. “Industrials is going to be the biggest net winner and retail the biggest net loser,” Woloshin predicts. He points to two nontraditional real estate assets—data centers and wireless towers—as winners as well. The future is harder to read in some other categories, such as medical, multifamily, office.

In Europe, “even some retailers you would expect could weather the storm stopped paying rents,” says Lisette Van Doorn, CEO of ULI Europe. French luxury brand LVMH, Swedish megaretailer H&M and German sporting brand Adidas were among the high-class names that suspended rent payments. “[It] wasn’t always well received,” says Van Doorn, pointing to systemic economic links. “Landlords often are pension funds, and they also have their financial obligations.” Adidas subsequently apologized and pledged to pay up.Many businesses passed some of the pain to their landlords, and rental payment patterns show the uneven impact. Nonessential consumer-facing businesses as diverse as AMC Theaters, Bath & Body Works, Victoria’s Secret, Century 21 Stores and LA Fitness dropped rent payments by more than 90% compared to a year ago, according to data on mid- to large-capacity corporate renters from Datex Property Solutions’ Tenant Track (Who’s Paying Rent and Who’s Not).

The impact hit everywhere. In mid-July, S&P lowered its ratings on Dubai’s Emaar Properties and Emaar Malls, citing weak expectations for business overall and especially tourist-reliant retail.In retail, right now there is much pain. The world’s economies one by one ground to a snail’s pace as citizens started to avoid retail shops, hotels, restaurants, gyms and entertainment venues—often not waiting for official lockdown. Office workers were sent home, diminishing the customer base for city centers. Businesses began to delay payments. Companies in both Mexico and Canada saw average invoice duration rise by 17 days, according to Atradius’ Payment Practices Barometer report in June. B2B defaults in Canada soared 86% over the prior year; for Mexico, defaults were up 45%.

For some companies, the pandemic was a final crushing blow. In North America, iconic groups that were already lagging, such as CMX Cinemas and Montreal-based shoe chain Aldo, filed for bankruptcy. Century-old retailer JC Penney paid 100% of its rent obligations for April, according to Datex; in May it filed for bankruptcy. Van Doorn says cultural differences emerged in Europe, with tenants and landlords collaborating more in the Netherlands than in the UK or France.

Deals on future rent have become an essential tool for sales. In June, commercial real estate company Unibail-Rodamco-Westfield (URW) sold a 54.2% stake in five French shopping malls for €2 billion ($2.3 billion) to a joint venture set up with the insurance arm of Credit Agricole and asset manager La Francaise. URW covered €24.4 million of a €45 million rent guarantee up to 2024. Even if the reopening in Europe is showing better-than-expected retail sales, consumers appeared much more focused and less willing to linger in malls, Van Doorn says.

While retail suffers, industrial properties—from warehouses to kitchens for takeout food—are doing well around the world. Remote work requires data and wireless infrastructure. Online shopping was among the trends accelerated by consumers in lockdown. “E commerce has become a way of life in Asia,” says the ULI’s Brooke. “There’s a huge demand for logistics around groceries, food and beverages.”

Omar Eltorai, a market analyst at software and data firm Reonomy, notes Covid 19 has also accelerated emerging trends toward reshoring and a shift away from just-in-time inventory management. “Trade tensions with China even before the pandemic were making companies rethink their global supply chains,” he says. “[Pandemic-driven] demand for delivery and fulfillment centers added additional fuel.”

As demand for industrials grows, citizen resistance constrains supply. “Many [European] cities don’t want those sheds nearby,” says Van Doorn. “They don’t look pretty, and they don’t generate much employment.”

Office Space

The future of office buildings remains an open question. Silicon Valley denizens had long predicted the end of the office, yet employers remained firmly grounded in brick and mortar. Then Covid 19 hit.

Though a last-minute resort, remote work has worked surprisingly well for many companies. Property-management specialist Cushman & Wakefield (C&W) surveyed 50,000 employees of its clients about their Covid 19 remote-work experience. Three fourths felt that they were “collaborating effectively with colleagues” and that productivity remained high. Overall, 73% believe their company should embrace some work flexibility going forward. “Through the emergency of having to work remotely, most of the workforce has made a great effort to adapt, and some of these changes are here to stay,” says Diego Rodinò di Miglione, C&W managing director.

However, there were also some discomforts, notably in the area of mentoring and teambuilding. “It is ludicrous to think that companies will not return to offices,” Bruce Flatt, CEO of Brookfield Asset Management, which owns 450 million square meters of commercial real estate worldwide, told Reuters in June. “Anyone who says they’re not going to be in offices is naïve about how company culture is built.”

Cultural differences play out in architecture too. “In China, working from home is not feasible, because of how homes are organized with multigeneration families and relatively small spaces,” says the ULI’s Brooke.

C&W has helped nearly a million Chinese employees get back to work safely post-Covid, according to di Miglione, and is continuing to do the same in other countries as well. In the process, C&W has assessed and designed adaptations to achieve less density and more personal protection in workspaces.

The return of office workers will be welcome news to city microbusinesses such as bars and restaurants, pharmacies, florists and clothing stores. In mid-June, the mayor of Milan, Italy, one of the cities worst hit by the pandemic, said on his Facebook page, “The ‘cave effect’ … has its dangers,” as he called for office workers to return and revive the city’s economy.

In China, where the pandemic started, there is optimism and activity. “A lot of domestic institutions—insurance companies, and pension and sovereign funds—are taking advantage of the absence of international funds,” says Brooke. “As international buyers cannot travel and cannot do their due diligence, domestic buyers are mopping up what is available.”

He cites some recent deals: Alibaba took a 50% stake of the $1.2 billion AXA Tower in Singapore; Gaw Capital snapped up a 46-story office building in Hangzhou partly let to Alibaba; and Ping An Insurance bought a 30% stake in Sun Hung Kai’s office development above the high speed rail station in West Kowloon, Hong Kong, for $1.45 billion.

Alan Todd, head of CMBS Strategy at Merrill Lynch in New York, says that also a significant amount of dry powder—emergency funds collected to be invested in distressed assets—will remain unused for a while. “This is not going to wrap itself up cleanly and nicely in six months. It is going to take up to several years for all the distressed [assets] to work their way through the system.”

In the Middle East, meanwhile, real estate may be losing some of its luster. “In the GCC, there was a predilection towards real estate as the core investment concentration; yet prices across the region and globally have gone down,” says Joseph Abraham, group CEO of Commercial Bank of Qatar. He predicts a new interest in alternatives that will create growth opportunities in wealth advisory services.

After Covid

UBS’ Woloshin doesn’t see remote working taking over, but he believes this may be the start of a shift out of large cities. “The trend we have seen in the last 25 years of densification, with more people in less space, is going to have to reverse,” he says. Offices being designed now for working through Covid 19 have lower employee density, and the open-office trend is giving way to personalized spaces that still permit air flow.

“People populating the offices in coming years will be people who really want to be present to grow professionally, to interact socially, to lead by example, to learn and to enrich themselves and their companies through unfiltered interactions,” says C&W’s di Miglione.

Offices with communal spaces, such as those of WeWork, are also likely to be put into the limelight. “Co-working has to change a few things,” says Woloshin. “But there’s still going to be demand for office space from small companies that cannot afford or do not want to negotiate their own lease.”

Indeed, the requirements of adaptation may also enhance the business of running offices. Companies are already inquiring about part-time rentals and the equivalent of “pop-up” offices that would allow teams to come together for a time without the company committing to ownership. The manager is now responsible for keeping up with Covid 19 trends and implementing the necessary changes.

Elevators will have to be reorganized as well as common spaces. With all the retrofit needed to protect people from the contagion, the current health crisis will be remembered by the industry as a period when commercial real estate gained in flexibility, Brooke says.

“We are living through a health crisis that is fast-tracking cultural shifts,” says di Miglione. “And commercial real estate will be front and center of the way many corporations and institutions reorganize themselves.”