A crisis-filled year reminded private banking customers of the value of the personal touch. This year’s winners found ways to accommodate them.

For most of the past decade, private banks struggled to keep up with an unprecedentedly mobile and global clientele. Board rooms loaded up on whiz-bang technology to transform the oak-paneled personal touch into anywhere-anytime, iPhone-sized financial management. Hands-on family counseling gave way to pop-up networking events in world capitals, one more calendar date for a jet-setting high net worth class.

In 2020, something funny happened. The jet setters had to stay home and began to crave—what else? The personal touch of trusted family counselors. Private bankers had to dust off old skills.

“We always had a close relationship with clients,” says David Bailin, CIO of Citi Private Bank. “This year I would describe it as truly intimate.”

Clients had plenty of appetite for trusted advice. Prevailing moods on the coronavirus pandemic swung from complacent to panicked and back more than once. Financial markets crashed, soared, then gyrated, more or less in tandem with that mood. Geopolitics did not take a rest either, with bitterly contested US elections, an assertive China and a still unsettled Brexit hanging over markets and personal destinies. Guidance on how to interpret this whirlwind of events grew more cacophonous as key world leaders scoffed at scientific consensus and media divided into partisan silos.

Against this background, private banks began to adopt an additional role as information source. Citi, Global Finance’s Best Private Bank for Net Worth of $25 Million or More, bombarded customers with online seminars featuring structured investment experts one day and epidemiologists the next.

“Clients absolutely loved our programming,” Bailin says.

“We had up to 1,800 people a week joining.” Competitors across the world followed suit. Brazil-based Banco Itaú Unibanco, our Best Private Bank for Digital Client Solutions, held some 200 webinars and virtual meetings with everyone from the bank’s own top executives to national politicians.

That doesn’t mean private bankers stopped leaning into technology as the Covid pandemic forced them to turn their business more fully virtual. Behind the scenes, evolving fintech and artificial intelligence systems kept speeding up and slimming down clunky back-office and compliance operations, handing a competitive advantage to the most adroit adopters. One example: Singapore’s DBS Bank, a perennial vanguard institution that takes this year’s award for Best Use of Technology, debuted an all-digital account opening system, short-circuiting reams of paperwork and giving it an inside track on new clients.

But private banking’s relationship with tech is maturing, says Anna Omarini, professor at Italy’s Bocconi School of Management, who studies fintechs; automated systems will neither disrupt high net worth advisers out of existence nor yield the killer app that enables them to overwhelm their competitors. Technology is back to being the cart, she argues, which every bank adapts to the horse of its clientele and brand.

“Tech is a force changing the industry, but not the only one,” says Omarini. “Banks should have a holistic approach to developing value for their customers.”

Battling Back

Rising competition at all levels is another force changing the industry: last year, this year and the next. At the upper end of the wealth scale, the ultrarich continue to migrate from private banks to family offices as their primary wealth management vehicle.

“Family offices are exploding now more than ever,” says Lauren Cohen, a professor at Harvard Business School who follows them. “Families don’t want to be one of 20 clients.”

At the lower end, mass-affluent brokerages keep shifting their goalposts and enriching their offerings to retain clients who cross the traditional $1 million private-banking threshold.

The best private banks are battling back. For ultrahigh ne worth individuals, that means symbiosis with family offices, doing what they can’t do for themselves: which is a lot.

“Family offices are trying to replace an organization of 1,000 people with a staff of maybe three,” Cohen says. “Many of the services private banks can provide are still incredibly valuable to them.” Northern Trust, our winner as Best Private Bank for Intergenerational and Family Office Services, understood this niche long ago. It extended its dominance this year by founding an internal think tank, the Northern Trust Institute, and expanding management options for philanthropies.

But the most decisive industry shift of 2020 was moving down market, blurring or obliterating lines between mass affluent and private banking to capture the soon-to-be-rich. Morgan Stanley, our Best Private Bank for Net Worth Under $1 Million, was already a leading mass-affluent “wirehouse” in the US. It stole a march on the competition this year with two major acquisitions: pioneering online brokerage E*TRADE and Eaton Vance, a midsized asset manager that combines institutional and high net worth accounts.

Other Wall Street giants followed the same trend. JP Morgan, which repeats in 2020 as the Best Private Bank in the World, redrew divisional lines to group clients from $250,000 to $25 million in net worth within one wealth management structure. Goldman Sachs, recognized this year as the best North American Bank for Entrepreneurs, reshuffled similarly to integrate private banking with its fast-growing Marcus online retail unit.

Staking Out the New Heartland

No less important than recognizing sub-$1 million clients was staking out a new private banking heartland in the (relative) middle tier of wealth, from about $5 million to $20 million, says Nalika Nanayakkara, who leads the wealth and asset management practice at Ernst & Young in New York. This is a challenging group to service because of its diversity: from athletes and entertainers to C-suite executives and law-firm partners. But it’s well insulated from raids by either wirehouses, which can’t offer sufficient services, or family offices, whose overhead is too heavy.

“Firms are finding out this neglected group is a gold mine,” Nanayakkara says. “All the big players are focusing efforts in this space.”

The pandemic seems to have accelerated another key concern of private banking clients: social impact. So-called environmental, social, and governance (ESG) funds kept growing even after the tumultuous start to 2020, according to Cerulli Associates.

Political events tilted in a socially conscious direction. The European Union and China both put ambitious climate-change targets at the heart of their post-Covid recovery strategies. Skeptics lost their global champion with Donald Trump’s reelection defeat in the US Markets also cooperated; stocks in “virtuous” industries like renewable energy and electric vehicles soared while oil and mining shares crashed.

More convincing for private bankers is the rising millennial generation’s faith in investing for good. UBS found that nearly three-quarters of high net worth 18-to-34-year-olds in the US mean to invest sustainably, compared to 6% of those over 65: a gap difficult to ignore as untold trillions pass steadily from the latter to the former.

UBS has been shifting toward ESG investment for a decade, and this year the Swiss industry giant formalized a “sustainability bias” as its “preferred solution” for long-term portfolio management. That earned UBS our nod as Best Private Bank for Millennials—now aged 24 to 39—despite no obvious hipster cred emanating from Zurich headquarters.

Some experiences of the pandemic year seem common to most people, rich or otherwise. Isolation made us treasure human contact as Zoom fatigue grew extreme. A fractured and shrill information environment, in the face of critical practical and financial decisions, made us treasure advice we could believe. Both these mass phenomena can work to private banks’ long-term benefit if they recommit to their core mission: one that has not changed that much, despite the upheavals.

“It really boils down to trusted relationships with your clients,” EY’s Nanayakkara concludes. “Everything else can be commoditized very quickly.”

Methodology: Behind the Rankings

Global Finance staff select winners for these awards based on entries submitted by banks, company documents and public filings. No proprietary information was sought or shared in the awards process. We consider local market knowledge, global footprint and investment breadth and sophistication. Because metrics are rarely public in this sensitive corner of finance, we incorporate perspective from analysts and consultants. Performance data are also drawn from industry sources including Scorpio Partnership’s annual Global Private Banking Benchmark and Asian Private Banker magazine’s regional league tables. Size and growth are a factor, but Global Finance also considered creativity, uniqueness of offering and dedication to private banking as a core business either globally or regionally.

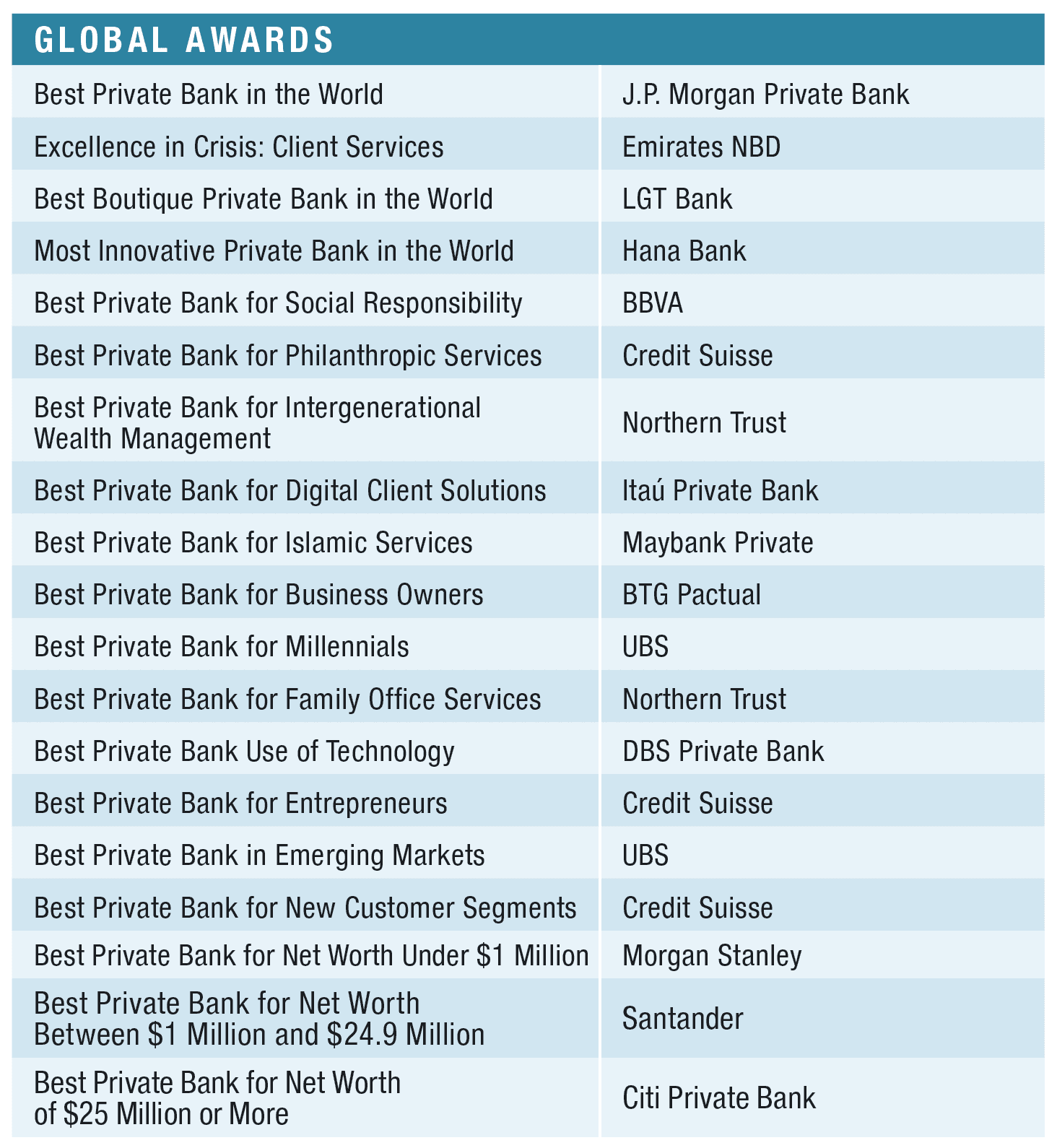

BEST PRIVATE BANK IN THE WORLD

J.P. MORGAN PRIVATE BANK

For years, changes in the high net worth marketplace have been pushing private banking out of its silo—or off its Swiss Alp—and toward integration with other elements of finance. High net worth individuals (HNWIs) have grown more entrepreneurial and want their wealth managers to act simultaneously as their investment bankers. Meanwhile, the path to getting rich has widened, elevating the importance of a feeder pool among mass-affluent clients.

J.P. Morgan, leaning on its powerful Chase retail arm, has been out ahead on both of these megatrends and keeps innovating to stay ahead. A restructuring late last year effectively merged Chase Private Client, an offer for branch customers with balances of $250,000 or more, with private banking (the $25 million-and-over crowd still have a division of their own). HNWIs keep getting more and deeper market options: for instance, an internal trading desk for shares in pre-IPO companies.

J.P. Morgan Private Bank thinks both locally and globally, with success. Aggressive marketing of the Chase brand has made it the hometown bank for HNWI clients in New York and elsewhere in the US Northeast. It was also the among the fastest-growing global banks in Asia during 2019, expanding assets under management (AUM) an impressive 28%. And it is lengthening its Latin American reach with a raft of new hires in Houston and Miami.

EXCELLENCE IN CRISIS: CLIENT SERVICES

EMIRATES NBD

Dubai’s biggest bank and the fourth largest lender in the Middle East, Emirates NBD distinguished itself with a swift and innovative response to the Covid-19 pandemic. Actually, the bank entered the crisis with a digital head start, having just last year overhauled its branding and product offering.

The bank’s commitment to digital transformation—embodied in its new award-winning motto, “Inspiring what’s next”—gave it an edge in delivering financial services through the crisis. Using mobile banking tools and cloud technology, it switched most of its operations to remote functioning within weeks of the first outbreaks of the coronavirus.

BEST BOUTIQUE PRIVATE BANK

LGT BANK

Liechtenstein-based LGT, which celebrated its 100th anniversary in 2020, has turned a profit every year of its existence. Yet the steady performer, controlled by the ruling family of the principality, is anything but cautious. It has nearly doubled its size over the past five years with a string of acquisitions that shifted its focus from numbered vaults in the Alps to the global growth nexus of Asia. Asian AUM grew by an eye-popping 28.5% annually from 2015 to 2019. At $231 billion in total AUM, LGT is small enough to remain close to its select clientele but big enough to offer a global perspective and capacity. LGT is looking to the future. It was an early entrant in sustainable investing, opening equity and bond funds with sustainable objectives in 2009. LGT Lightstone is the group’s impact investing platform, and last year it acquired an impact investment manager in India to pursue opportunities there.

MOST INNOVATIVE PRIVATE BANK

HANA BANK

South Korea’s Hana Bank understands that innovation is about more than gadgets. In Asia, most of the wealth that private banks manage is created from still-active family businesses. Bankers therefore serve essentially the same clients as corporate lenders, investment strategists and counselors on inheritance and other key life questions. Hana was an early digital adopter, launching its online Hana Private Banking System in 2011, and has also targeted the advanced technology required to pursue a strategy of holistic integration. The effort is paying off: Private banking funds managed for corporate customers are growing by a third each year. More recently, Hana Bank has focused on expanding the lifestyle component of its private banking offering, adding an online global network of real estate advisers for wealthy Koreans looking to educate their children abroad and an art-buying channel in collaboration with Seoul’s most prestigious auction house.

A decade of deepening virtual capability has also enabled Hana Bank to lean into the coronavirus pandemic, integrating its investment portal with its video conferencing system and adding new money management options like real estate investment trusts and currency swaps. The goal is to be a “total life solution provider,” the bank says, and it is continually devising innovative ways to get there.

BEST PRIVATE BANK FOR SOCIAL RESPONSIBILITY

BBVA

Europe has embraced a green future more enthusiastically than any other region; and BBVA is a leader in financing the transition, according to a World Resources Institute 2019 report. The Spanish financial services group, whose reach extends to 10 countries across North and South America, is working hard to persuade its 600,000-plus private banking customers to focus on socially responsible and sustainable investments. It has built a portfolio module aggregating funds across the world that accentuate positive megatrends from health and wellbeing to demographics and longevity, and it scores every fund it markets to HNWI clients on sustainability metrics.

That’s just the start, as BBVA pushes toward its goal of mobilizing €100 billion (about $119 billion) in sustainable finance by 2025. Private banking clients do not have to come along for the ride, but BBVA is trying to make the choice as attractive as possible.

BEST PRIVATE BANK FOR PHILANTHROPIC SERVICES

BEST PRIVATE BANK ENTREPRENEURS

BEST PRIVATE BANK FOR NEW CUSTOMER SEGMENTS

CREDIT SUISSE

Credit Suisse got off to a rocky start this year as CEO Tidjane Thiam stepped down in February after an escalating corporate espionage scandal. But successor Thomas Gottstein moved smartly to shore up and accelerate Thiam’s core strategy: putting the bank’s global markets and investment banking reach at the service of HNW entrepreneurs in the hope of swelling “collaboration revenues.”

To this end, Gottstein brought in Christian Meissner, former chief of investment banking at Bank of America, to head a new Zurich-based advisory unit “that will do mergers and capital markets deals with customers of the international wealth business.” Gottstein also told a financial conference that he’s open “to look at acquisition opportunities, especially in private banking,” even as rumors swirled that Credit Suisse could itself be absorbed by its giant neighbor UBS.

Fortune favored Credit Suisse this year, as the Covid-19 pandemic shifted economic gravity further toward Asia, the focus of its expansion over the past half decade. With China alone producing more than one IPO a day, Asian entrepreneurs seem poised to keep driving wealth management globally; and Credit Suisse is intent on getting its share of their business.

Writing a check to Unicef or the local hospital fails to satisfy the philanthropic urges of an increasing number of private banking clients. They want a charity program as individualized and goal-oriented as their investments. But most are too busy with their own businesses to study the complex global giving market.

Credit Suisse is ahead of the curve on stepping into this gap. One vehicle is its “umbrella foundations,” three headquartered at home base in Switzerland and a fourth in Singapore. They provide a ready-made structure, staff and expertise for “subfoundations” set up by individual clients and families. Jointly they have funneled some $235 million to nonprofits over the past decade.

The bank sets an example by focusing its own philanthropy on combatting illiteracy and supporting girls’ education in developing nations. African-born Thiam became a global ambassador and fund-raiser for Room to Read, an NGO pushing these efforts in 16 countries. The bank’s 14-year partnership with Room to Read is one practice his successors will want to continue while helping clients boost the causes closest to their hearts.

BEST PRIVATE BANK FOR INTERGENERATIONAL WEALTH MANAGEMENT

BEST PRIVATE BANK FOR FAMILY OFFICE SERVICES

NORTHERN TRUST

In the US heartland, home of the short-term investor, Northern Trust has been playing the long game for 130 years. A traditional manager and custodian for large institutional assets, the Chicago-based bank was among the first to realize that many rich families command institution-scale wealth that requires a special structure: the family office.

Northern Trust has built steadily on its pioneering role in multigenerational wealth management and did not take time off in 2020. In June, it launched the Northern Trust Institute, a research entity with a semiacademic structure. It has steadily expanded a division that manages money for foundations and nonprofits, keeping a step ahead of family offices rivals’ growing philanthropic efforts. While focused on its home market in North America, the bank also made new hires targeting Latin America and the UK. The efforts are paying off, as Northern Trust’s wealth management earnings have continued to rise in 2020 through a tough year of pandemic and shrinking interest income.

BEST PRIVATE BANK FOR DIGITAL CLIENT SOLUTIONS

ITAÚ PRIVATE BANK

Private banks around the world took on the roles of news provider and social network during this pandemic year, as clients sought trustworthy information and the advice of peers. Latin American private banking giant Itaú Unibanco jumped into the void, providing more than 200 online conversations with public figures and its own executives and analysts. Despite tumultuous financial markets, it hired 20 new private banking managers in the first half of 2020, expanding its franchise as others retrenched. The market responded, lifting private banking income by 11% in the first half.

Recently, data analysis has become the institution’s key to customer insight and therefore service. “Our huge investment in technological platforms facilitated our clients’ engagement with the digital services we offer,” says Luiz Severiano Ribeiro, the global head of private banking. “Our clients’ satisfaction kept the same level as in 2019. Our customers are delighted to get through this crisis so well.”

BEST PRIVATE BANK FOR ISLAMIC SERVICES

MAYBANK PRIVATE

You might not know it from the news, but just over 20% of the world’s Muslims live in Arab countries; most reside in South and Southeast Asia. That puts Maybank, headquartered in Malaysia with offices in 20 mostly surrounding countries, in a perfect position to service them. Maybank embeds Shariah-compliant channels in a broader world-class private banking operation. “H.O.T. Broking” (Honest views, Opening channels, Transparent information), described as “end-to-end Shariah-inspired equities trading,” is fully integrated with the rest of Maybank’s online platform. The results have been positive. Private banking client numbers jumped by 19% in the most recent fiscal year and revenue grew 17%, suggesting that for a large provider with a presence throughout the region’s Islamic community, Shariah has staying power.

BEST PRIVATE BANK FOR BUSINESS OWNERS

BTG PACTUAL

Numerous global players are committed to blending private and investment banking, as most new wealth today is generated by entrepreneurs who are still raising cash and making deals for their core business. None dominates its market like BTG Pactual. From its home base in Brazil, BTG has expanded to become the go-to financier for growing businesses across Latin America. In 2020, the ravages of the coronavirus did nothing to slow down the trend. Brazil had its biggest year for IPOs since 2007 as record-low interest rates pushed local savers into stocks, and domestic banks like BTG took most of the mandates.

While BTG remains as a distant runner-up to its compatriot Itaú in private banking overall, it aims to triple its current $41 billion in AUM within five years. Providing a one-stop shop for Latin American business is the path it expects will take it there.

For these special clients and their families, the institution has built a tailor-made program for succession planning, offering a series of meetings with experts. In 2019, BTG also reviewed its strategic guidelines for investments to prioritize two topics: education and the environment. Beyond its support to 30 Brazilian institutions acting in these areas, the bank encourages business owners to engage their companies in socially and environmentally responsible procedures.

BEST PRIVATE BANK FOR MILLENNIALS

BEST PRIVATE BANK IN EMERGING MARKETS

UBS

UBS, the most venerable pillar of the private banking establishment, might seem a strange choice for HNW millennials. But the Swiss behemoth leads the industry in what the youngest clients may care most about: sustainable investing. According to UBS’ own data, 72% of HNWIs 18 to 34 years old in the US intend to commit to a sustainable strategy, compared to 6% of those 65 and up. UBS has been preparing for this shift for decades: 20 dedicated professionals help manage $488 billion in “core sustainable assets.” The bank doubled down in 2020, betting the pandemic would intensify wealthy clients’ consideration of their investments’ environmental and social impact. UBS officially declared a sustainability bias “the preferred solution” for long-term portfolio management, with a range of strategies on offer from water to health care.

Of the many remarkable private banking stories in emerging markets, the most striking may be UBS’ persistent dominance. The Swiss-based industry giant still boasts nearly twice the AUM in Asia as its nearest rival, Credit Suisse, and a five-year average growth rate of 13.2%—among the best in the business. Sergio Ermotti closed out a highly successful nine-year run as UBS’ CEO—the banker who made “boring” great again—in 2020, just over a year after the colossus of Zurich imported a bundle of dynamism in the person of wealth management co-head Iqbal Khan, poached from Credit Suisse. Khan looks to be shifting focus toward new emerging markets—creating new divisions to service Eastern Europe and Middle East/Africa while eliminating stand-alone private banking in the US, where its bankers will shift into the larger wealth management practice. Ermotti went out on a high note as UBS’ third-quarter earnings nearly doubled and wealth management nudged up in tough circumstances. With Khan continuing in his new role, the focus on private banking appears to be set for some time.

BEST PRIVATE BANK USE OF TECHNOLOGY

DBS PRIVATE BANK

How can a homegrown Singapore bank compete with the giants of global private banking as they refocus on a growing Asian market? DBS CEO Piyush Gupta gave a three-word answer back in 2013: “Innovate or die.” DBS has been innovating ever since, driving the shift to 24/7 digital client access. Its “Hack2Hire” program ensures a steady stream of talented new nerds coming on board to design the next tweak and offering.

Gupta’s troops were not idle in 2020, even while Singapore authorities kept them out of the home office for much of the year. DBS launched a major upgrade of its core iWealth app, offering an easier, more intuitive user experience. It unveiled all-virtual account opening for private banking clients in Hong Kong, shredding the paperwork that weighs down customer acquisition across much of the industry. It enhanced its Intelligent Banking artificial intelligence system, adding features like foreign exchange alerts when shifting currency values open trading opportunities for global portfolios. Keeping with the worldwide trend to look down-market, DBS teamed with outside fintechs to offer segmented products for different wealth points: digiPortfolio, a hybrid of robot and personalized asset management; and its new NAV Planner for retail investors. Other banks are investing heavily in all these directions. But DBS is staying a step ahead by making the best technology its core mission. Its motto: “Live more. Bank less.”

BEST PRIVATE BANK FOR NET WORTH UNDER $1 MILLION

MORGAN STANLEY

Long a global leader in managing millionaires’ money, Morgan Stanley announced two giant steps down-market in 2020: the acquisitions of mass-affluent brokerage Eaton Vance and of E*Trade, a pioneer in online retail services. The deals should put the bank ahead of one of the industry’s hotter trends: leveraging technology to integrate traditional, white-glove private banking with broader wealth management in order to capture the next generation of the rich as they climb the ladder.

Morgan Stanley already had a solid platform in the under-$1 million space, rooted in its opportunistic grabs of US franchises Dean Witter and Smith Barney during earlier financial crises. It dominates the standard wealth adviser rankings compiled by Forbes and Barron’s. And management has been remarkably steady in an industry addicted to churn as private bank CEO Shelley O’Connor completes her 10th year since she first became CEO.

Morgan Stanley has not neglected foreign markets either. It ranks fourth by AUM in Asia, and it has been hiring aggressively in Miami to grab Latin American clients.

BEST PRIVATE BANK FOR NET WORTH BETWEEN $1 MILLION AND $24.9 MILLION

SANTANDER

For much of the past decade, the fashion in private banking focused on ultrahigh net worth (UHNW) clients with $25 million or more to invest. This year, the pendulum is swinging the opposite way, toward mass-affluent customers possibly on their way to millionaire status. The “merely rich” in the middle tend to be neglected, but not at Santander. Santander, whose biggest markets are Brazil and the UK, is happy to count 95% of its private banking customers in the below €10 million category. Its threshold is €500,000, and it concentrates, in its own words, “only on clients to whom private banking brings added value.” In its Portuguese operation, for example, that meant 17% fewer customers for the year ending in June but 5% more in AUM and an 11% increase in net profit.

Santander looks to spoil its midmarket clients with old-school private banking based on the relationship manager while leaning on its commercial banking reach to nurture the core businesses. This approach has made it a leader in Portugal, but the private banking franchise has plenty of room to expand elsewhere. Santander has 15 times as many retail/corporate customers in Brazil as in Portugal and eight times as many in the UK. Add a considerable footprint in the US and Mexico, and a global player may be on the rise.

BEST PRIVATE BANK FOR NET WORTH OF $25 MILLION OR MORE

CITI PRIVATE BANK

Citi is bucking the industry trend as it sticks with the strategy it launched a decade ago: restricting its private bank to customers with $25 million liquid and up. The bank lavishes these “global citizens” with a wealth of 360-degree, anytime-anywhere services, from M&A investment banking services to art advisory and sports finance. Its exclusive focus on UHNWIs has enabled Citi to cement microfranchises among subgroups like the Indian diaspora and US law firm partners.

As its super-rich clientele migrate to autonomous family offices, Citi has become a service provider to more than 1,400 such operations in more than 80 countries. Its annual summit, the “Davos for family offices,” drew over 4,000 participants this year: virtually, of course. Next-generation programs are another area where Citi Private Bank leads, although youth gatherings of 2019 in San Francisco, New York, and Cambridge in the UK went on hiatus this year. While super-rich global citizens have had to lie low physically in 2020, surprisingly buoyant markets and plentiful deal-making have kept their money as active as ever, making Citi’s private banking strategy a success.