For Global Finance’s top TCM banks, navigating the Covid crisis means AI, innovation, better FX functionality and real-time for virtually everything.

The ongoing Covid-19 pandemic is testing the success of a decadelong effort by banks to transform their global transactions arms for a digital age. What was once a halting, piecemeal process at many institutions is now critical to serving their corporate clients attempting to navigate their way through the crisis.

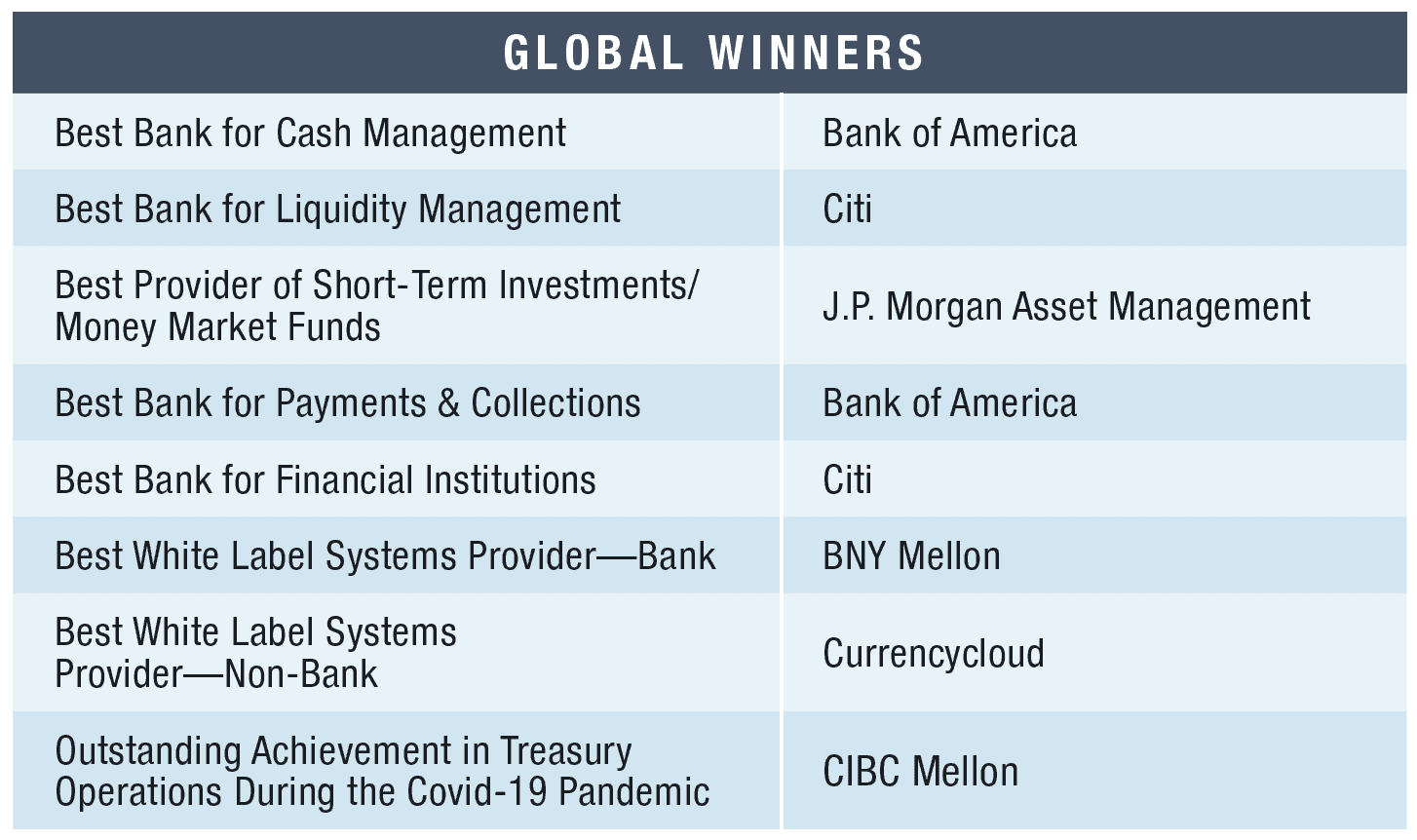

Prior to Covid-19, some corporates were embracing and driving digital transformation, while others focused their efforts only on certain business units, observes Paul Camp, CEO of Treasury Services at BNY Mellon, Global Finance’s Best White Label Systems Provider—Bank for the third year in a row. Many others were hesitant to change, often because they lacked the budget to overhaul legacy systems. “What we’re finding is that, thanks to Covid-19, the transition to digital has taken on much more momentum across much broader segments and much broader pieces of our client business than ever before,” says Camp, “and with a much greater sense of urgency.”

At Bank of America, 2021 global Best Bank for Cash Management and Best Bank for Payments and Collections for the second straight year, a global payments network was crucial to obtaining real-time information on how companies were navigating the virus—information that was particularly important during the early days of the pandemic.

“Our teams in China, Singapore and elsewhere were invaluable in passing along on-the-ground reports and what we needed to plan for business continuity,” says Faiz Ahmad, head of Global Transaction Services at BofA. “Our global trade finance footprint additionally helped us identify trends in economic activity throughout the pandemic. We’ve hosted multiple calls and Webex sessions for our clients to share this intelligence and for us to advise them on operational and tactical changes that would ensure uninterrupted treasury operations.”

In this environment, innovation is building on itself, says Camp. “Digital treasury innovation is not only delivering the next chapter of where the business is going,” he says, “but it’s leveraging scalable, underpinning technology.”

Artificial Intelligence (AI) is becoming a key technology for treasury. “AI is a core component of corporate treasury digital transformation, and it relies heavily on data,” says Tapodyuti Bose, global head of digital channels and data for Treasury and Trade Solutions at Citi, 2021 global Best Bank for Liquidity Management for the second year in a row and Best Bank for Financial Institutions. “It can augment or replace human functions with smart technology systems that can perform tasks on their own, and it can help predict and drive actions proactively.” As a tool for treasury and cash management, he says, AI can optimize liquidity and cash forecasting for working capital management, manage returns on short-term investments, detect suspicious or outlier activity to minimize fraud and operational errors, measure and mitigate foreign exchange and interest rate risk exposure, and drive smart automation through bots that eliminate manual touchpoints and bespoke processes like reconciliation.

Lately, digital solutions for foreign exchange (FX) transactions have been a particular focus for corporates and their banks. At the request of clients, Bank of America introduced a new application programming interface (API) in the fourth quarter for FX settlement.

“Now, clients can directly manage cross-border payments, either initiating a single cross-currency FX payment or bundling payments into one foreign exchange settlement using our API,” Ahmad says.

The desire for greater efficiency and better functionality is changing the FX business landscape. Ten years ago, corporate treasurers regularly received calls from FX brokers offering them better rates than their competitors. “Essentially, the focus was on paying out international invoices cheaply and quickly,” says Harry Geller, global head of FX brokerage at Currencycloud, 2021 global Best White Label Systems Provider—Non-Bank.

More recently, banks have worked to differentiate themselves by providing tech functionality to deliver a customer experience that would traditionally have been available only to the very largest multinationals.

That poses a challenge to FX brokers whose “expertise does not lie in tech development. That’s a cost and time investment that is out of reach for many,” Geller says. “That’s where white labels add real value. Companies like ours invest in research and development and build regulated, compliant treasury systems that FX brokers can use—bringing best-in-class quality to the treasury teams of SMEs [small and midsize enterprises]—while the FX brokers focus on what they can bring to the table: superior rates and service.”

White-label providers that deliver multicurrency treasury hubs have two key areas of focus, Geller says: functionality and visibility. By eliminating the currency problem for SMEs, these hubs make it easier to do business internationally. “Increased currency visibility and reporting deliver the ability to create risk-mitigating forward hedges that allow SMEs to protect profit margins.”

This year, Geller predicts, banking providers and fintechs will collaborate more closely on solutions that provide higher levels of treasury functionality by combining multi-user interface (MUI) feeds, still under a single sign-on platform.

“We’ll see improved reporting tools that provide businesses with better insights and better ability to manage their internal treasury, ultimately decreasing risk and costs by allowing SMEs to net currency balances and book forward contracts with more accuracy. While this may already be bread and butter for a FTSE 100 company, it is a game changer for SMEs and goes a long way to leveling the competitive landscape for them.”

Collaborating with fintechs brings both agility and cost savings to the innovation process—an important consideration for transaction banks, which have seen their cash management profits decline in line with interest rate cuts.

“In the past, interest rates and liquidity cross-subsidized the big investments, such as payments and digitalization; so, it was hugely important income in global transaction banking,” says Luca Corsini, co-head of Global Transaction Banking at UniCredit. “Now, not only is this disappearing, but it is becoming a cost. When the industry needs to invest an amount of money in a specific project—such as the ISO 20022 messaging standard migration, for example—the principal way for banks to justify the expenditure is to charge corporate clients for liquidity. We are already seeing it in the German market, and now it’s happening in Italy. In essence, it’s about charging fees in order to avoid costs, as opposed to making revenue.”

As the global economy slowly recovers from the Covid-19 crisis, banks will need to balance their books to accommodate negative or close-to-zero interest rates without letting their digital transformation efforts slip.

Methodology

Global Finance editors select the winners for the Best Treasury & Cash Management Awards with input from industry analysts, corporate executives and technology experts. The editors also use entries submitted by financial services providers, as well as independent research, to evaluate a series of objective and subjective factors. It is not necessary to enter in order to win, but experience shows that the additional information supplied in an entry can increase the chances of success. In many cases, entrants are able to present details and insights that may not be readily available to the editors of Global Finance. This year’s ratings are based on the period from January 1, 2020, to December 31, 2020. [Companies with different fiscal year reporting have the option to submit data from the fourth quarter of 2019 through the third quarter of 2020.] Global Finance uses a proprietary algorithm with criteria—such as knowledge of local conditions and corporate customer needs, quality of product and service offerings, financial strength and safety, market standing, compliance and excellent customer service—weighted for relative importance. The algorithm incorporates various ratings into a single numerical score, with 100 equivalent to perfection. In cases where more than one institution earns the same score, we favor local providers over global institutions, and privately owned banks over government-owned ones.

The winners are those financial services providers that best meet the specialized needs of corporations engaged in global business. These top-notch finance institutions are not always the biggest, but rather the best—those with qualities that companies should look for when choosing a provider.