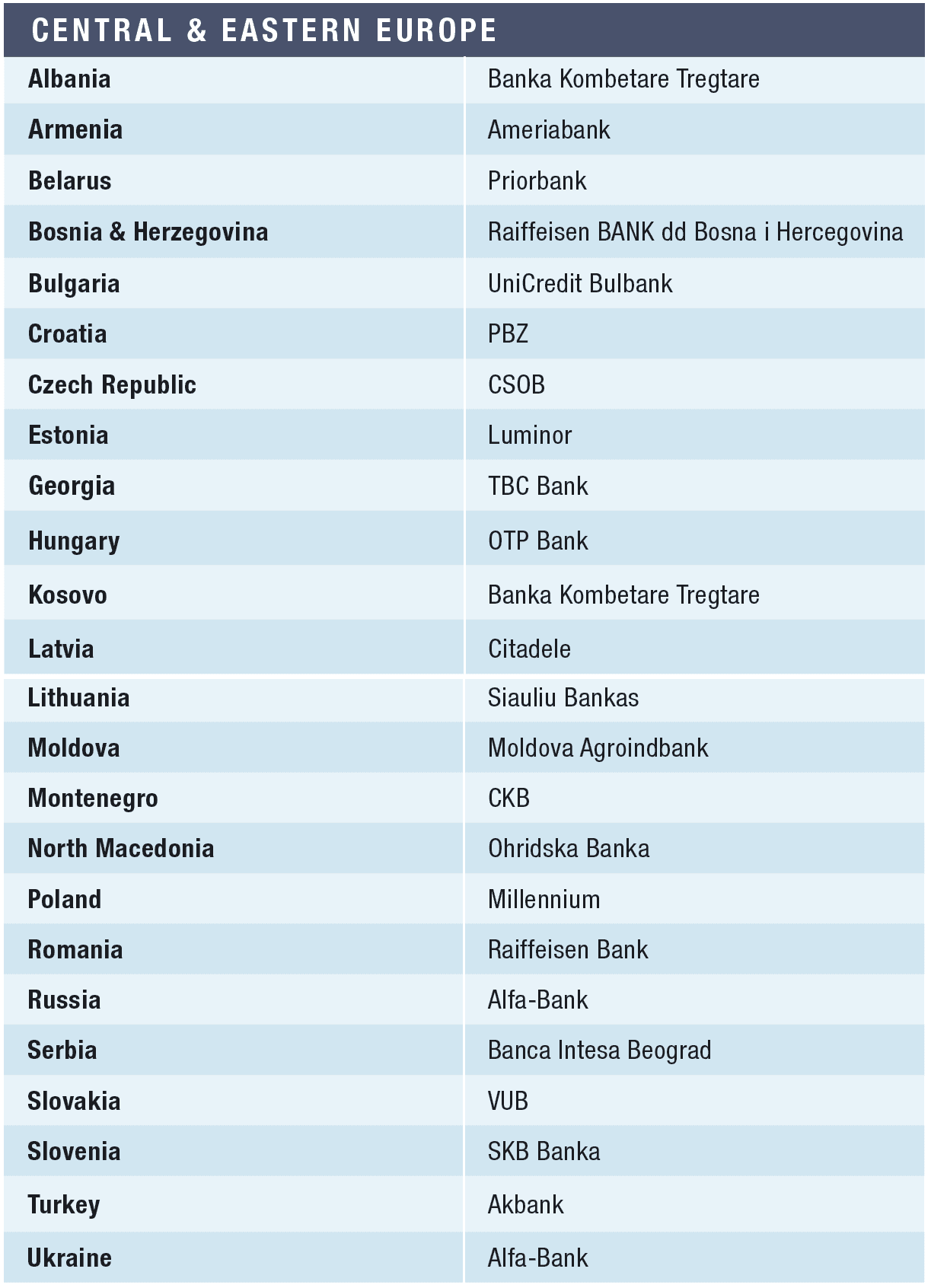

This year’s best banks in the Central & Eastern European region responded to the pandemic crisis with agility.

Most countries in Central and Eastern Europe were less affected than their western neighbors by the first wave of the pandemic. During 2020 their economies, which are typically based more on manufacturing and agrobusiness than consumer-facing services, proved resilient and in many cases registered positive growth.

The region’s leading banks responded to this by expanding their loan portfolios across the board while at the same time cutting costs and shoring up their capital base through retained earnings and increasing provisions against anticipated Covid-19 related loan losses.

While CEE banks were obliged to take the same precautionary measures as elsewhere in adapting their branches and increasing home working, they also invested in improving levels of service—especially by upgrading their digital offerings. As a result, the migration of CEE bank customers to online or mobile channels accelerated faster than elsewhere. While this surge in digital banking came off a relatively low baseline it shows every indication of becoming a long-term trend.

Our Best Bank in Central and Eastern Europe is Raiffeisen Bank International (RBI) which has the broadest footprint of any financial institution across the region, with subsidiaries serving 13 separate markets–three of which are country winners this year. While group operating income fell by 5% compared to 2019 this was largely offset by an equal reduction in administrative costs and, even after raising impairment charges to €630 million, RBI was able to report consolidated profits of €804 million.

“RBI entered the pandemic from a position of strength” says CEO Johann Strobl, “and therefore achieved a satisfactory result given the very difficult environment. We are well capitalized, which allows us to grow with our customers and at the same time let our shareholders participate in RBI’s success.”

RBI’s pandemic-related support for our customers ranged from extending maturities and adjusting loan terms to providing advice on coronavirus state aid packages. In different markets. “Like every crisis, this one has also shown that resulting opportunities may present themselves,” says Strobl, “the acceleration of the digitalization process, the shift towards new working methods and the emergence of new business models.”

RBI achieved a 9.2% return on equity while raising its NPE coverage ratio to 61.5%. The group’s CET 1 capital adequacy ratio stood at 15.4% at the year end.

Central Europe

The Czech Republic has been particularly hard hit by the pandemic and slower economic activity reduced earnings across the banking sector. Nevertheless, our repeat winner, SOB, grew its loan portfolio by 2% over the year. Deposits rose by 12% and as customers sought a new home for higher savings SOB recorded a 5% rise in total assets under management. The share of non-performing loans across the entire loan portfolio was low at 2.3% at the year end and SOB maintains strong capital buffers with a Tier 1 capital ratio of 23.7%.

Customer migration to online and other remote channels accelerated, the number of active clients increased by 66,000 year-on-year. “The pandemic era has confirmed that our ‘Digital with a Human Touch’ strategy is the right way,” says Jan Sadil, SOB board director responsible for retail banking.

A member of the Intesa Sanpaolo Group, VUB Banka is Slovakia’s second largest banking group and this year’s winner having strengthened its position in the key deposit and loans markets. The bank increased its shares of both retail and corporate deposits resulting in a 19.2% overall market share and maintained its position as the second largest lender in the country with a 21.1% market share.

VUB Banka had an especially successful year in the mortgage market, increasing volumes by 12% to improve its market share to 24%. The loan to deposit ratio stood at a prudent 92.8%, with deposits growing faster than loans. Capital buffers were strengthened during 2020 and VUB has one of the highest capital adequacy ratios in the Slovak market, standing at 18.3%.

Hungary’s largest bank, OTP Bank, is a repeat winner this year due to its dynamic lending combined with good risk controls. Performing loans grew by 19%, mostly driven by the subsidized baby loans, while customer deposits rose by 18% year-on-year. The bank’s core Hungarian operations benefited from increased volumes of lending to record a 4% improvement in operating profit, but the need to provision against future loan impairments resulted in higher risk costs overall and a 17% reduction in after-tax profit.

During 2020 OTP Bank expanded its balance sheet by 19%, much of this due to rapid growth in customer deposits as well as lending, while maintaining robust capital and liquidity buffers with a Tier 1 capital ratio of 22.5% at the year end. And having expanded its presence across South-Eastern Europe though a string of acquisitions, OTP’s CEO Sándor Csányi said at a recent press conference “we have very good acquisitions in the pipeline,” adding that of three acquisition projects under way, only one was in a market in which OTP was already present.

Amongst the most successful of OTP’s earlier acquisitions is our Best Bank in Slovenia, SKB Banka, which was relaunched in 2020 through an extensive corporate marketing campaign. During 2020, the bank generated net income of €122.7 million, a 1.3 % drop compared to the previous standout year. This was achieved largely due to SKB’s above average margins on both lending and other banking services. CEO Anita Stojevska credited the bank’s values of team spirit, responsibility, innovation and commitment as “the foundation for an encouraging business environment and healthy long-term relationships with clients.” SKB strengthened its capital base during 2020, increasing its capital adequacy ratio from 12.3 % to 15.2 % at the end of the year.

Eastern Europe

Our Best Bank in Russia is the country’s largest privately-owned financial institution, Alfa-Bank, which increased its after-tax profit to $1.3 billion in 2020. This in part reflects the continued growth of its customer base with the number of active retail clients increasing to 7.3 million.

Alexei Tchoukhlov, deputy chairman and CFO, noted “we again managed to attract about one million new active customers in retail business and about 100,000 small business clients during the crisis year. We were also able to take advantage of the growing interest in investments of Russian people: the number of the Alfa-Direct platform clients increased by 3.5 times. We focused on controlling credit risks in the second quarter, however, as the situation improved, we resumed active lending and significantly increased our loan portfolio without decreasing its quality at the end of the year.”

Net fee and commission income grew by 18.9% to more than $1.2 billion (a 32.5% increase in ruble terms). Exchange rate volatility during 2020 had a significant impact on key balance sheet indicators, but the bank’s total assets grew by 4.0% in dollar terms over the year to nearly $62 billion. Alfa-Bank maintained robust capital buffers with a Tier 1 capital adequacy ratio of 16.4% at the year-end.

Bank Millennium is this year’s winner in Poland for its digital innovation and strong operating results. Sales of new mortgage loans increased by 57% which boosted market share to 12.2%. Core income rose marginally with a 6% increase in fee income. Merger synergies with Eurobank combined with improved efficiencies led to a 15% reduction in the branch network and lower costs. Debit cards issued passed 3 million for the first time, while the number of active digital and mobile customers rose by 12% and 18% respectively.

Bank Millennium was recently named one of the top ten most digitally advanced European banks by Bain & Company. The bank’s headline result was sharply down due to provisions against legal risks related to foreign currency mortgages and the costs of integrating Eurobank.

Šiauli Bankas is again our winner in Lithuania as it continues to attract new customers through its digital offering and award-winning service. More than 21,000 new private customers and over 2,000 new business customers started using the bank’s services in 2020. The number of logins to the e-channels increased by 26% during the year and in December for the first time exceeded one million logins.

The bank’s total assets grew by 21% to above €3 billion and its loan portfolio increased by 5% to €1.76 billion, with mortgage lending almost trebling over the year. While post-tax profits fell to €43.0 million, the bank’s operating result before impairment losses and tax was only 5% less than in 2019.

In neighboring Latvia this year’s Best Bank is Citadele, the country’s second largest bank by assets, which during 2020 grew the number of active customers by 4% to an all-time high of 326,000 clients, including a 9% increase in Mobile App users.

“During the year we have improved the resilience of the business model to better support our customers and leveraging our financial strength the UniCredit Leasing acquisition closed beginning of 2021,” said CEO Johan Åkerblom in February. Customer deposits grew by 18% over the year and the bank maintained strong capital and liquidity ratios, its CAR standing at 26.0%. Moody’s recently upgraded Citadele’s credit rating to investment grade with positive outlook.

Our Best Bank in Estonia, Luminor, was forged out of the discontinued Baltic banking operations of Nordea and DNB which sold a controlling shareholding to US investment group Blackstone. During 2020, Luminor completed the technology carve out from its former parent banks, with its Estonian customers ‘migrated’ to the new banking platform in November.

Deposits from customers increased by €713 million to €11.8 billion in the fourth quarter, leading to a loan to deposit ratio of 80%, while the portfolio of non-performing loans stood at 3.2%, the bank’s lowest ever ratio. Net profit in the fourth quarter was €18.6 million, an increase of €14.6 million compared to the same period last year.

During 2020, our Best Bank in Belarus, Priorbank, actively promoted digital channels by offering new electronic products and services, resulting in the number of active mobile bank users to increase over 40%. This fed through into enhanced sales, Priorbank’s market share of digitally initiated personal loans sales having increased from 13% to 17% over the year. CEO Sergey Kostyuchenko notes that “while we are trying to involve modern technologies and approaches in every working process and every customer touchpoint, trust and reliability remain our cornerstones.” While net interest income fell by 12% on the back of lower margins and stable loan volumes, Priorbank improved its operating result before impairment charges. Return on equity was slightly lower at 14.4%.

Our repeat winner in Moldova, state-owned Moldova Agroindbank, is the country’s largest lender with a 34.2% market share of loans and a 30% share of deposits. The bank grew its asset base by 8% in 2020, and despite a slight fall in headline profit it achieved return on equity of 13.6% over the year. Alongside its new mobile banking application, MAIBank, in 2020 Moldova Agroindbank also launched the country’s first currency exchange service at ATMs and implemented an online 3-module anti-money laundering system.

Alfa-Bank is our winner in the Ukraine, having continued to strengthen its market position through 2020 despite economic headwinds. With a market share of 12.6%, Alfa-Bank is the leader in loans to private individuals, while it stands second in terms of net assets (4.9 %) and overall loans to customers (7.1%).

In 2020, Alfa-Bank focused on its digital transformation with the launch in November of its new digital banking application, Sense SuperApp, which in two months became the most-downloaded app in the financial category of Google Play in Ukraine. In reaffirming Alfa-Bank’s credit rating, Fitch recently noted that over the last three quarters of 2020 the bank improved the quality of its loan portfolio, strengthened its capitalization, maintained a strong liquidity cushion and boosted pre-impairment profitability.

The Balkans

During 2020 our Best Bank in Serbia, Banca Intesa Beograd, consolidated its leading market position. Total assets increased by nearly 10%, loans grew by 9.3%, while deposits rose by 10.3%. Intesa Leasing (a financial leasing services company) also retained first place in the market measured by new placements, with market share of almost 20%.

The first Serbian bank to implement the government-endorsed Women in Business program in Serbia, in cooperation with the EBRD, Banca Intesa recently signed an €8 million credit line, placing a total of €19.5 million in lending at the disposal of women-led businesses. With the backing of the European Union, the bank has also launched a long-term lending product designed for agricultural producers–EaSi Farmer Invest Loans.

Another member of the Intesa Group, PBZ, is our winner in Croatia and the country’s second largest bank by assets. With market shares of up to or slightly above 20% in key operating segments, PBZ enjoys leadership in card transactions and has the most extensive branch network in the country. During 2020, PBZ built on its leadership in digital technology with the launch of Online Loans, the first product of its kind on the market, and now some 96% of transactions are carried out electronically.

The second largest bank in the country by all key financial categories (assets, loans, capital, deposits), our winner in Bosnia & Hercegovina is Raiffeisen Bank. Since the launch of its new mobile banking app RMB over a year ago, the bank has doubled the number of active users. It also launched RaiConnect, a new communication platform for Premium and SME clients. James Stewart, interim CEO, notes that “we accelerated our digital transformation, adapting to the changing habits of our customers not only by upgrading our current services but also by developing new digital ones.”

Our Best Bank in Albania, Banka Kombëtare Tregtare (BKT), consolidated its position as the country’s largest bank by total assets, the bank’s 27% market share is almost double that of its closest competitor. Its market share in key activities such as credit cards exceeds 50%. BKT remains the most profitable bank in the Albanian banking industry with an ROE of 18.9%, having increased net profits to $47 million on the back of a growing loan book, higher levels of deposits, and sound management of its non-performing loans. Looking ahead, BKT is looking to expand into neighboring regions and is studying new potential markets.

A member of Austria’s Steiermärkische Sparkasse Group since 2019 and our Best Bank in North Macedonia again this year, Ohridska Banka grew its asset base by 7% during a difficult year. Customer loans grew by 5% while net interest income was flat. The merger with Sparkasse Banka Makedonija is still ongoing and increases the combined group’s market share to 14%. The bank’s technology focus is on full integration which should be completed by the end of this year.

The integration of our winner in Montenegro, CKB, with Podgorika banka (formerly Société Générale Montenegro) was completed in December 2020, giving CKB the highest number of retail clients in the country and more than 30% household market share. A member of the OTP Group, CKB’s President Miklos Nemeth stated “the integrated bank has further improved its leading market position in terms of deposits and loan portfolios. The customers will have access to the largest network of branches and ATMs, as well as a wide range of modern banking services.”

Albanian-owned Banka Kombëtare Tregtare Kosovë (BKT) is our Best Bank in Kosovo, having grown its assets base by a quarter on the back of a 20% increase in customer deposits, while loans to customers rose by 15%. The bank also improved its efficiency which resulted in a lower cost-to-income ratio of 42.4% and succeeded in decreasing NPL ratio from 2.04% in 2019 to just below 2% despite the pandemic.

Bulgaria’s largest bank by assets, UniCredit Bulbank, wins again, having outperformed its competitors in both efficiency and profitability. Despite the pandemic and ultra-low interest rates, the bank achieved above-average profit margins resulting in a 6.2% ROE—in large part due to its lower risk costs and internal efficiencies which produced a cost/income ratio of 40.4%. The bank maintained its market leadership in corporate and investment banking and, with more than 1.2 million customers, remains a key player in all segments of retail banking.

Customer deposits at our winner in Romania, Raiffeisen Bank, grew by 21% last year and total assets were up by 20%. Although net profits were down 17%, this reflected not just the strains on the Romanian economy in this pandemic year, but also the bank’s conservative provisioning policy. Non-performing loans were lower, the ratio to total loans standing at 3.8%.

Steven van Groningen, President & CEO Raiffeisen Bank Romania, notes that “in these unusual circumstances, we managed to increase the loan portfolio by 5% and achieved a return on equity of 14%. What we know for sure today is that we will continue to sustainably finance the Romanian economy because banks are part of the solution and there is an economic growth potential.”

The Near East

A repeat winner in Turkey, Akbank, concentrated on strategy and technology investments, implementing its Digital First program and becoming the first bank in the country to offer numberless credit cards. CEO Hakan Binbagil points out that “in 2020, the loan support we provided to the economy increased to a total of TL331 billion, with TL279 billion in cash loans. Our deposits increased by 19.5% while our assets increased by 23.5%. We have one of the strongest capital structures in the sector with a robust capital adequacy ratio of 20.7%.”

In February 2021, Akbank announced a new working model for the post-pandemic era, featuring three different working practices: remote work, hybrid work and office work, with 52% of head office staff expected to work remotely in the future.

TBC is our Best Bank in Georgia, having increased its asset base by 23.0% on strong growth in both lending and deposits–key segments where it is clear leader with nearly 40% market share–while reinforcing its dominance in commercial banking, leasing, brokerage and investment banking. The number of affluent clients increased 15% over the year and TBC’s fully digital bank space and its suite of user-friendly apps resulted in 96% of all transactions being conducted through digital channels. The bank’s ROE stood at 11.7% after conservative provisioning against credit impairments; without the additional reserves it would have been 24.7%, only marginally lower than the previous year at 24.7%.

Armenia’s Ameriabank ranks first in the country’s banking system in key metrics from total assets and deposits to equity and loans. The bank demonstrated leadership across corporate and retail business lines, a commitment to product innovation and cutting-edge financial technology. Ameriabank ticked the ESG box last year with the issuance of a €42 million Green bond— alongside the Netherland’s FMO—which represented Armenia’s first Green project funding.