LATIN AMERICA

by Antonio Guerrero

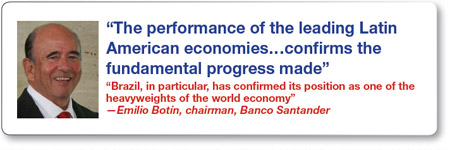

REGIONAL WINNER: Banco Santander

Brazil continues to shine as the jewel in Santander’s crown, helping the Spanish bank consolidate its position as Latin America’s premier financial group. Santander Brasil set a benchmark in 2009 when it raised $8 billion on the São Paulo and New York stock exchanges. The transaction marked the largest-ever equity deal for a Brazilian corporate and the world’s largest IPO of the year. In the wake of the merger between Santander Brasil and Banco Real, completed last year, Santander plans to open 613 new branches in Brazil through 2013. In 2009 the bank sold Banco de Venezuela to the Venezuelan government for $1.05 billion. Latin America contributed 36% of Santander’s 2009 profits, with Brazil accounting for 20% of the total. Attributable profit in Latin America rose 11%, to $5.33 billion. The bank’s efficiency ratio in the region improved 6.6 points, to 37.3%. “The performance of the leading Latin American economies during this period of global recession confirms the fundamental progress made by the region in recent years, the result of judicious policy choices,” says Santander chairman Emilio Botín. “Brazil, in particular, has confirmed its position as one of the heavyweights of the world economy, and it will continue to be one of our major assets in the coming years.”

Brazil continues to shine as the jewel in Santander’s crown, helping the Spanish bank consolidate its position as Latin America’s premier financial group. Santander Brasil set a benchmark in 2009 when it raised $8 billion on the São Paulo and New York stock exchanges. The transaction marked the largest-ever equity deal for a Brazilian corporate and the world’s largest IPO of the year. In the wake of the merger between Santander Brasil and Banco Real, completed last year, Santander plans to open 613 new branches in Brazil through 2013. In 2009 the bank sold Banco de Venezuela to the Venezuelan government for $1.05 billion. Latin America contributed 36% of Santander’s 2009 profits, with Brazil accounting for 20% of the total. Attributable profit in Latin America rose 11%, to $5.33 billion. The bank’s efficiency ratio in the region improved 6.6 points, to 37.3%. “The performance of the leading Latin American economies during this period of global recession confirms the fundamental progress made by the region in recent years, the result of judicious policy choices,” says Santander chairman Emilio Botín. “Brazil, in particular, has confirmed its position as one of the heavyweights of the world economy, and it will continue to be one of our major assets in the coming years.”

Emilio Botín, chairman

www.santander.com

Argentina

Banco Macro

Jorge Brito, president |

Banco Macro continues to focus its growth on areas outside Buenos Aires, with 90% of customers located beyond the capital city’s metropolitan area. The bank continues to service mainly low- and middle-income individuals and small and medium-size businesses often overlooked by larger players. The strategy has paid off well, as private sector loans grew 4% and deposits 5% in 2009, an otherwise challenging year for the Argentine economy. Sound risk management gave Macro liquid assets of 59.7% of total deposits in 2009, with a non-performing loan (NPL) ratio of 3.2%. Net income through September 2009 was $230 million, for an annualized return on equity (ROE) of 23% and return on assets (ROA) of 2.8%. ROA was significant considering Macro’s balance-sheet leveraging (8.4 assets-to-equity ratio). In 2009 Macro completed the merger with Nuevo Banco Bisel, acquired in 2006. Its strong numbers make it Argentina’s most liquid banking stock and the sector’s most frequent debt issuer. |

Barbados

FirstCaribbean International

With more than $10.5 billion in assets and $2 billion in market capitalization in 2009, FirstCaribbean holds its standing as the largest regionally listed financial services institution in both the English- and Dutch-speaking Caribbean. The bank operates 100 branches in 17 Caribbean countries and territories, including Jamaica, Trinidad and Tobago, the Cayman Islands and Curacao, among other important financial and industrial centers. In 2009 the bank reported net income attributable to equity holders of the parent of $171 million, slightly lower than 2008’s $175 million. Total revenue rose from $551 million in 2008 to $568 million in 2009, ROE was 12.3%, and the efficiency ratio was 56.3%. In 2009 FirstCaribbean turned its strategic focus to becoming a relationship bank, offering a wider range of services. It also enhanced its Internet banking platform to make it more user friendly. For its affluent customers, the bank launched a co-branded Platinum Visa card with British Airways.

John D. Orr, chief executive officer

www.firstcaribbeanbank.com

Belize

Belize Bank

Belize Bank is a big fish in a small, albeit very beautiful, pond. As the largest and oldest full-service bank in a market comprising only five financial sector players, Belize Bank has invested in the technology, customer service and geographic footprint that have given it a more than 41% market share of loans and 37% share of deposits in the Central American nation of just 300,000 inhabitants. Founded in 1902, Belize Bank today operates 12 branches nationwide and is favored by international investors doing business in the country. As part of a plan to build a pan-Caribbean financial services group, parent company BCB Holdings, already listed on the London Stock Exchange, completed a cross-listing on the Trinidad and Tobago Stock Exchange in 2009. The group also operates a bank in the Turks and Caicos Islands. Belize Bank reported $419 million in assets and $22.4 million in reserves in 2009.

Lyndon Guiseppi, chairman and CEO

www.belizebank.com

Bolivia

Banco de Crédito de Bolivia

Diego Cavero Belaunde, chief executive officer |

Despite a challenging year, Banco de Crédito de Bolivia (BCB) maintained the market’s lowest non-performing loan ratio for the third consecutive year in 2009, at 1.81%. The bank implemented strict credit policies on its $466 million loan portfolio and set provisions over NPLs at 257.9%, 54% higher than the system’s average. BCB still managed to grow its assets by 14.5% year on year to $1.1 billion in 2009, when ROE was 30.9% and ROA was 2.8%. In 2009 the bank increased its focus on small and medium-size enterprises (SMEs) and invested $3.5 million in new technology, including the introduction of biometric readers at all teller stations and the replacement of 20% of its ATMs. Internet transactions rose 10% last year. The bank services clients through the country’s largest distribution network, with 65 branches and 172 ATMs. In 2009, BCB expanded its corporate social responsibility (CSR) offerings by launching a web page to help students sharpen their mathematical skills. |

Brazil

Itaú Unibanco

Itaú Unibanco is a juggernaut that cannot be stopped. The result of the 2008 merger of two giants, Banco Itaú and Unibanco, the bank is already Latin America’s largest financial institution but continues to seek growth opportunities both at home and abroad. With operations abroad reporting $29.7 billion in assets in 2009, the bank was rumored to be pursuing a UK acquisition last year. Its 2009 total assets were an estimated $300 billion, with net income of some $5 billion. ROE was 21.4%, and ROA was 1.7%. Itaú Unibanco operates 3,948 branches throughout Brazil, up from 3,906 in 2008, as well as another 948 customer site branches and 30,276 ATMs. In 2009, Itaú Unibanco formed an alliance with local insurer Porto Seguro to combine their automobile and residential insurance businesses in Brazil and Uruguay. The bank was included on the Dow Jones Sustainability World Index for the 10th consecutive year.

Roberto Setubal, chief executive officer

www.itau.com.br

Chile

Banco Santander-Chile

Banco Santander-Chile continues to grow partly through alliances with corporate customers, allowing the bank to identify another 7 million potential clients beyond its current 3 million customers. Examples include the launch of a co-branded credit card with Movistar, Chile’s largest mobile phone operator. Besides having the country’s largest client base, the bank also has Chile’s largest distribution network, with 500 branches and 1,917 ATMs. The bank’s strategy has been to actively manage its balance sheet, grow selectively, increase cross-selling and control costs. Though total loans declined 5.9% year on year in 2009, institutional loans grew 20.5% and residential mortgages grew 4.5%. The bank still outperformed its competitors, posting the sector’s highest net interest margin (5.5%) and return on capital (34.9%). Santander responded to a rise in non-performing loans from 2.72% in 2008 to 2.98% in 2009 by boosting its coverage from 70.9% to 85.4%.

Claudio Melandri, chief executive officer

www.santander.cl

Colombia

Bancolombia

Jorge Londoño, president and CEO |

Serving nearly 6 million customers, Bancolombia is already Colombia’s largest bank, but in 2009 the institution explored new growth channels. It introduced a program for SMEs, attracting 600,000 micro, small and medium-size companies; launched a private equity fund focused on real estate investments, with nearly $200 million in assets; and obtained a license to operate a leasing company in Peru. It launched a financial education program to train students aged nine to 19 on financial matters, also bringing the sessions to rural students through its “School on Wheels” buses. It is little surprise that, with 713 branches nationwide, Bancolombia remains “Top of Mind” for 36% of Colombians, 19 points above the second bank in the ranking. Its technology investments have led to 87% of total transactions being carried out electronically, including at 2,271 ATMs. Bancolombia has a 19.8% market share of assets, 21% of the sector’s gross loan portfolio and 18.5% of deposits. |

Costa Rica

Scotiabank Costa Rica

While Scotiabank’s Costa Rican subsidiary is not the nation’s largest bank, it is one of its most dynamic. With $1.74 billion in assets, Scotiabank Costa Rica is the Central American country’s fifth-largest bank by assets, holding a 10.5% market share of loans ($1.33 billion) and 9.1% of deposits ($1.34 billion) in 2009. The bank created a new subsidiary, Scotia Insurance Agency, to market and service insurance products as part of a broader diversification strategy. The new unit is primarily focused on insuring mortgages, auto loans and leasing contracts. It also consolidated its trust area, which has grown steadily to nearly 20% of the bank’s annual portfolio. In 2009, Scotiabank Costa Rica concluded the first phase of its “IT Environmental Friendliness Meter” project, which allows the bank to measure its IT systems’ environmental impact, including everything from its use of energy to paper and ink, in one of the most environmentally conscious countries on Earth.

Carlos Lomelí Alonzo, president

www.scotiabankcr.com

Dominican Republic

Banco Popular Dominicano

The Dominican Republic’s booming tourism sector and other local industries owe much of their growth to financial support from Banco Popular Dominicano (BPD). Founded in 1963 as the country’s first privately owned bank, and intended to support small industries and farmers, BPD has since become an engine for corporate growth nationwide. Its more than 1.7 million customers are serviced by 4,500 employees at 187 branches, or through its more than 500 ATMs, together comprising the nation’s largest financial services distribution network. One would be hard pressed to travel around the Dominican Republic without encountering the Banco Popular Dominicano logo. In 2009 its total assets grew by 6% year on year to some $5 billion. Its net loan portfolio also grew by 10%, with the expansion driven mainly by commercial loans. Total deposits jumped 7%. The bank’s sound management policies have been rewarded with an AA- rating from Fitch and an A+ rating from Feller Rate.

Manuel A. Grullon, chief executive officer

www.bpd.com.do

Ecuador

Banco Pichincha

Since its founding in 1906, Banco Pichincha has grown to become Ecuador’s largest bank. It operates 279 branches, 657 ATMs and more than 66 kiosks in 22 provinces. It also services 1.8 million customers and holds a 31% and 28% market share of loans and deposits, respectively. Pichincha reported $4.5 billion in assets and $4 billion in deposits in 2009. The bank is a strong corporate citizen, whose CSR activities are focused on promoting business ethics, community development, responsible marketing, improving quality of life for workers and environmental protection. The Crisfe Foundation joins the Banco Pichincha financial group’s CSR efforts for all its divisions under a single umbrella, granting scholarships, teaching SMEs about the importance of corporate responsibility and providing access to technology, among other initiatives. The bank has been rated AA+ by Bank Watch Ratings since 2006, the highest international risk rating of any Ecuadorian bank. It is also rated AAA- by Pacific Credit Rating.

Aurelio Fernando Pozo, general manager

www.pichincha.com

El Salvador

Banco Agrícola

Over the past five years, Banco Agrícola has implemented a conservative strategy that has paid off by allowing the bank to maintain its market share of loans (30.7%) and deposits (30.4%) in a difficult economic environment. The bank holds the market’s lowest past-due loan ratio and its best efficiency ratio. A leader in the corporate banking segment, Banco Agrícola launched a series of customer service improvements to retain a competitive advantage. In 2009 the bank introduced a new credit card linked to automatic payroll deductions and launched personal finance classes for clients in a bid to boost financial awareness and strengthen customer loyalty. Technology investments have led to an estimated 76% of transactions being conducted electronically via Internet banking and ATMs. It operates El Salvador’s largest distribution network, with 653 service points, including full-service branches, mini branches, ATMs and kiosks. Total assets were nearly $4 billion in 2009, when ROE was 9.73%.

Roberto Orellana Milla, executive president

www.bancoagricola.com

Guatemala

Banco Agromercantil

Since its founding in 2000, the result of a merger between Banco del Agro and Banco Agrícola Mercantil, Banco Agromercantil has effectively retained its market leadership. After introducing mobile phone banking and launching new insurance products in 2008, the bank launched a restructuring drive in 2009 to better face local and global economic challenges. The effort led to the creation of specialized business banking areas to attract corporate clients, among other tactics. The result was the market’s highest growth rate in deposits, loans and total assets. The number of clients grew by 17.2% in 2009, to 1.25 million, after 2008’s astounding 74.7% growth. Total assets rose 5.5% year on year in 2009, to $1.26 billion. The bank grew its net loan portfolio by 16.43%, compared with an average of just 1.6% for the sector. Agromercantil continued to build reserves and invest in technology. ROA in 2009 was 1.1%, and ROE was 14.7%.

José Luis Valdés, president

www.agromercantil.com.gt

Honduras

Banco Atlántida

Last year’s political upheaval in Honduras, with president Manuel Zelaya ousted by the nation’s military and replaced by an interim administration as factions negotiated an end to the turmoil, led to the country’s virtual isolation from the international arena. The situation did not bode well for the nation’s banks or its few large corporate players. However, Banco Atlántida not only weathered the storm but also helped keep the nation’s battered economy on track. After all, since its founding in 1913, the bank has survived many other political and economic crises. In 2009 it continued to attract clients by launching a series of high-profile contests, with prizes including houses and new automobiles. It also partnered with a local university to launch Telescuela Atlántida, a televised mathematics and language arts tutorial program for students in first through fourth grades. The program is considered one of the Honduran private sector’s largest educational endeavors.

Guillermo Bueso, acting CEO

www.bancatlan.hn

Jamaica

Scotiabank Jamaica

Scotiabank Jamaica proved that it has the flexibility to adapt its business strategy quickly to face an ever-changing economic environment. When the island’s economic downturn boosted unemployment and reduced spending power, the bank responded by partnering with used-car dealers to offer auto loans for customers no longer able, or willing, to invest in new cars. To stave off potential defaults, the bank also proactively invited all loan customers in good standing to renegotiate their loans. It even extended a $100 million loan to the Jamaican government in 2009 to support the national budget and help the country meet its eurobond repayment schedule. Net income for the year ended October 2009 rose to $9.65 million, compared to the previous year’s still healthy $8.62 million. ROA was 3.9%, and ROE was 27.21%. The bank’s productivity ratio was 58.4% in 2009. Scotiabank Jamaica operates 39 branches and has just over 2,200 employees.

Bruce Bowen, president and CEO

www.jamaica.scotiabank.com

Mexico

Banamex

As Banamex celebrated its 125th anniversary in 2009, Citi found itself in the awkward position of defending its right to maintain its Mexican banking unit. With Washington’s bailout of the US banking giant putting 27% of Citi’s common stock under government control, Mexican regulators unsuccessfully invoked a law that prohibits foreign governments from owning banks in Mexico. Having faced the possibility of having to sell the operation, Citi chose to fight the battle and retain control of one of its most profitable ventures. Banamex was acquired by Citigroup for $12.5 billion in 2001, marking the largest-ever US-Mexican corporate merger. The bank has expanded its distribution network to 1,700 branches (it opened 50 last year) and 6,000 ATMs in 1,300 communities. Its more than 17 million clients represent four in 10 economically active Mexicans. In 2009, Banamex partnered with mobile phone operator Telcel to become the first bank in Mexico to introduce mobile banking.

Roberto Hernández Ramirez, president

www.banamex.com.mx

Panama

Banco General

As a leading lender to low- and middle-income borrowers, Banco General has capitalized on Panama’s ongoing real estate boom. It is also benefiting from the $5.25 billion expansion of the Panama Canal, which is contributing to the country’s economic growth and helping position Panama for a much awaited investment-grade rating. Founded in 1955, Banco General is a subsidiary of Empresa General de Inversiones, one of the country’s largest investment groups. The bank, which operates 63 offices nationwide, offers a broad portfolio of products, including personal and commercial banking, pension funds, leasing, insurance, credit cards, factoring, securities and bond issuance, foreign exchange and mortgages. In 2009 the Inter-American Development Bank approved a $20 million non-sovereign guaranteed loan for Banco General to help develop a portfolio of green projects in Panama. Funds will be used to finance SME projects involving energy efficiency, renewable energy, water and wastewater treatment, waste management and other carbon-mitigating ventures.

Federico Humbert, president

www.bgeneral.com

Paraguay

Interbanco

Established in 1978, Interbanco is Paraguay’s largest private bank by assets and is regarded as a market pioneer in a variety of areas. Interbanco was the first local bank to offer Internet banking and phone banking, is the country’s sole issuer of American Express cards and is the first to issue platinum-level credit cards. While the bank offers retail banking through 22 branches, its focus remains on the commercial banking sector, with particular emphasis on trade finance. With commodities an important source of export revenues in Paraguay, Interbanco has taken on increasing relevance for the country’s economic growth. Interbanco’s CSR efforts are focused on health, culture and environmental preservation. For the past three years, the bank, along with other companies, has sponsored a program to prepare outstanding school students to enter the workforce. It is also the official bank for the country’s annual telethon to help physically challenged children, assisting in processing donations.

Claudio Yamaguti, president

www.interbanco.com.py

Peru

BBVA Banco Continental

BBVA Banco Continental, part of Spain’s BBVA financial group, is a market innovator in Peru, constantly developing new products and services. In 2009 the bank unleashed an intense branding campaign, after which 77% of customers polled felt the bank had improved its overall image. BBVA Banco Continental is one of only two Peruvian banks with a coveted investment-grade rating. The bank saw a decline in past-due loans to 1.04% in 2009, from 1.17%, compared with a market average of 1.56%. The NPL ratio, nevertheless, rose to 2.38% on account of an increase in refinanced loans, though it still remained lower than the overall sector average of 2.71%. The bank’s coverage ratio was the Peruvian banking system’s highest, at 401.1%. Net profits rose 28.1% year on year. BBVA Banco Continental operates 229 branches and more than 1,900 ATMs.

Eduardo Torres-Llosa, general manager

www.bbvabancocontinental.com

Puerto Rico

Banco Santander Puerto Rico

Juan Moreno Blanco, chief executive officer |

With Puerto Rico’s economy in its fourth year of recession, the island presents a significant challenge for banks seeking to remain profitable or, at the very least, remain afloat. The situation has eroded personal and corporate finances, boosted unemployment and heightened inflationary pressures. Total bankruptcies soared 26% year on year between January and November 2009. Banco Santander Puerto Rico remains the battered market’s star player by maximizing organic growth through cross-selling to diversify revenue, strengthening its credit risk management framework to maintain asset quality, and controlling operating expenses to improve efficiency. The game plan led to a 5.38% net interest margin (tax equivalent basis) through September 2009, from 4.4% the previous year. Its cost-cutting led to a $48.8 million decline in operating expenses, to $200.5 million. Santander BanCorp, the local holding company, reported a rise in 2009 net income to $22.5 million, from 2008’s $16.1 million. |

Trinidad & Tobago

Scotiabank Trinidad and Tobago

Operating in Trinidad and Tobago since 1954, Scotiabank’s unit is a pioneer in the island nation’s financial sector. It is the only bank in Trinidad with an e-business solution, through its Internet merchant account or e-Scotia, as well as the only one offering an interactive teller platform that allows for paperless transactions. In 2009 the bank refocused its approach to corporate and commercial banking by introducing further market segmentation. It also rolled out a home financing unit with mobile sales offices and launched the “20 in 20” mortgage program, which gives retail customers 20% of their principal back at the end of the 20-year mortgage period. Scotiabank Trinidad and Tobago has increased its profitability and maintained consistent dividend growth for 17 consecutive years. Assets grew 11.7% in 2009, when net profit also rose 5.4%. ROE was 22.86%. The bank operates 24 branches, four sales centers and more than 81 ATMs.

Richard P. Young, managing director

www.scotiabank.com

Uruguay

Banco Santander Uruguay

Jorge Jourdan, chief executive officer |

Arriving in Uruguay in 1980, Spain’s Banco Santander consolidated its presence with the 2008 acquisition of ABN AMRO’s local operations. The deal made it the country’s largest private sector bank, with a 31% market share. With the merger completed in 2009, Santander ranks number one among private banks in terms of assets, liabilities, loans, net worth, net profit and ROE. Its 40 branches nationwide give it the country’s most solid financial network. More than 700 employees service some 200,000 individual and corporate clients. By acquiring ABN AMRO Uruguay, long considered the country’s strongest financial institution, Santander also added the Dutch bank’s Van Gogh Preferred Banking investment centers for affluent clients, with some $2 billion in assets under management. Through a partnership with insurer Mapfre, the bank launched its insurance business in 2009. Total assets rose 17.8% in 2009, to $3.79 billion, with net profits rising 64%, to $59 million. ROE was 19%. |

Venezuela

BBVA Banco Provincial

Pedro Rodríguez Serrano, chief executive officer |

A weakened economy and the government’s mounting stance against foreign companies make operating under Venezuela’s socialist regime a challenge for international banks. Yet in 2009 BBVA Banco Provincial surpassed competitors in terms of profitability and other key indicators. The bank’s long-term strategy is focused on maintaining profitable growth, cost efficiency and providing quality customer service. To help meet its objectives last year, BBVA Banco Provincial not only increased liquidity reserves but also diversified them by investing more heavily in higher-yielding government-guaranteed bonds. Liquidity reserves were $6.9 billion, of which 53% were non-mandatory. Despite increased reserves, the financial intermediation rate remained unchanged from 2008, at 67%. Total assets rose 22.6% in 2009, to $16.2 billion. Net income was the sector’s highest, at $653.6 million. Due to strict risk policies, the bank had a loan delinquency rate of just 0.92%, compared with a sector average of 2.52%. ROE was 45.13%, and ROA was 4.54%. |